Uncategorized

A premature pessimism

admin | January 3, 2019

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors.

The financial markets are currently reflecting a deep pessimism that the US economy is on the brink of recession, and are pricing in a significant chance that the FOMC will be forced to begin cutting rates in 2019. Furthermore, market expectations are that the Fed’s ammunition is so depleted that any actions taken to defend their price stability mandate will be ineffective, and inflation will remain below the 2% target for a decade or more. Such pessimism seems premature, but has created attractive investment opportunities to be short the belly of the curve and long inflation breakevens.

Pricing in an imminent recession

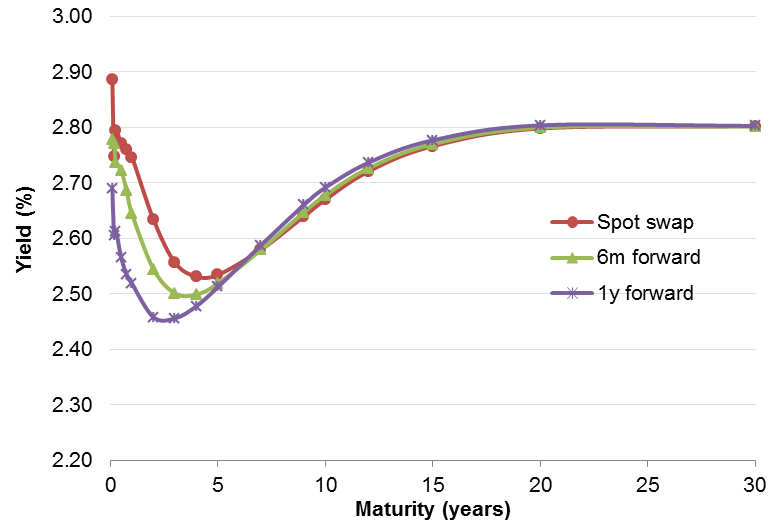

The financial markets, by nature and by design, anticipate future economic and political events. The prices of goods, securities, financial contracts and derivatives of all kinds reflect these expectations of future states of the world. But front-running a recession that isn’t likely to occur for 12 to 18 months seems too aggressive. The Treasury and swap curves are inverted in the front end, mechanically pushing forward rates lower. The spot swap curve is shown in Exhibit 1, along with the 6-month and 1-year implied forward curves. The 6-month and 1-year forward rates out to five years are lower than current spot rates, implying that the market expects short term rates to decline. The 1-year spot rate on the swap curve is 2.75%, with 1-year forward 1-year rate 23 bp lower at 2.25%. This is roughly consistent with what is priced into fed funds futures contracts, with spot fed funds rates of 2.40% for the January – March 2019 contracts, while the January 2020 contract rate is lower at 2.31%.

Exhibit 1: Spot and forward swap curves are pricing in lower rates

Source: Bloomberg, Amherst Pierpont Securities

Both of these markets are pricing in a significant probability that the Fed will cut rates before the end of 2019. The forwards were even lower prior to the impressively strong employment report, but the near-term pessimism has still not fully faded. The 5-year spot swap rate is 2.53% with the 6-month and 12-month projected forwards barely lower at 2.51%, while the 7-year point on the curve is virtually flat at 2.58% across the spot and forward horizons.

Expectations of an ineffective FOMC

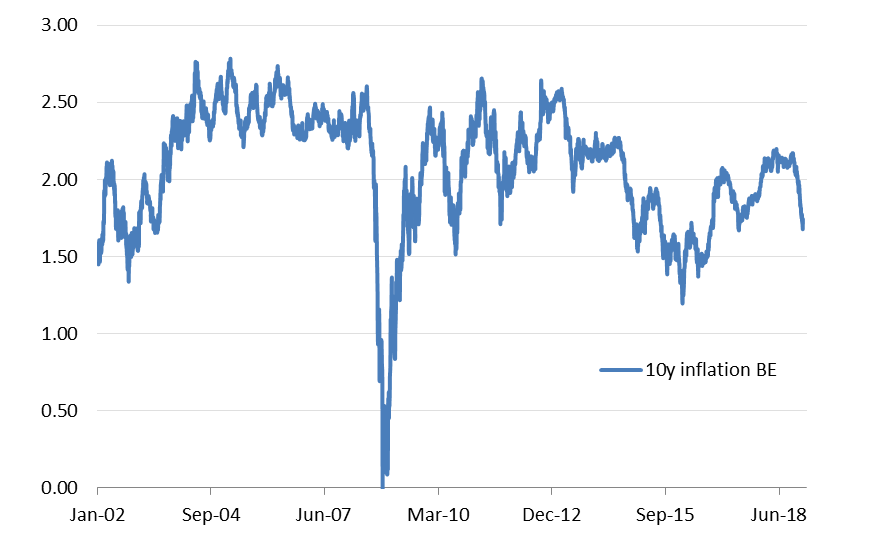

Equally pessimistic is the markets opinion of the potential effectiveness of FOMC policy actions to achieve their dual mandate of full employment and price stability. The FOMC has a 2.0% inflation target as part of its price stability mandate. During the risk-off movement of the past few weeks, inflation breakevens in the TIPS market have dropped sharply, as shown in Exhibit 2. Ten-year breakevens are now hovering at 1.7%, below the level of inflation reflected in core PCE which has been running at 1.9% year-over-year.

Exhibit 2: Ten-year inflation breakevens have dropped sharply

Source: Bloomberg, Amherst Pierpont Securities

The sharp drop in inflation expectations when the unemployment rate is at historic lows and wages are rising faster than 3.0% per year is effectively the market registering a no confidence vote in the Fed’s ability to achieve its inflation target over the next decade. There are arguably technical factors impacting the TIPS market, as volatility in credit and equities could be widening TIPS as well, pushing breakevens mechanically lower. Still the entire breakeven curve is well below the Fed’s 2% inflation target, with 30-year breakevens the “high point” at 1.82%.

Fade the pessimism

Short of the economy falling imminently into recession, it seems very unlikely that the FOMC will cut rates in 2019. On that basis the pessimism of the market is overdone, and the belly through the long-end of the Treasury and swaps curve should re-price, pushing yields a bit higher. The upside is that with the front end inverted, being short 5-year Treasuries or paying fixed in 5-year swaps over the next six months is flat to modestly positive carry. Get long 5-year or 10-year inflation breakevens.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2024 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.