Uncategorized

A recipe for steady volatility

admin | May 31, 2019

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors.

Fixed income markets continue to reprice for trade war with an increasingly uncertain set of outcomes. The US-China conflict has pitted two of the world’s largest and strongest economies in a likely long test of each other’s economic and political will to continue. US-Mexico, if it goes beyond initial threats, would open a second front. Markets globally since the May 9 announcement of new US tariffs on China have marked down implied growth and inflation. Credit spreads have widened. Correlations have shifted. It’s a recipe for steady volatility. But investment performance since May 9 is a good roadmap to safe harbor.

Prospects for an extended US-China conflict

The US and China meet next at the June 28-29 G20 summit, but rhetoric and action on both sides look far from promising. Press reports suggest that both US and Chinese officials have framed the conflict in aggressive terms. The US has blacklisted China’s Huawei from buying US software and components. And the US has also announced $16 billion in subsidies for farmers affected by tariffs. China has warned Canada against backing the US in the fight with Beijing.

Neither side looks likely to have reason to concede by the time the G20 arrives. Each side has plenty of resources and a clear idea of potential costs. Less clear is the economic and political willingness to bear the costs. The measurable impact of trade war on US and Chinese economies will almost certainly take months or years to show up, reducing pressure on both the US and China to concede by the end of June. That raises the prospects for a long fight that should keep driving market volatility.

Complexities of a US-Mexico conflict

The latest surprise of a US-Mexico trade conflict brings the added complexity that it is as much about politics as economics. The US apparently wants to use tariffs to fix problems with immigration from Mexico. It is unclear what might constitute a sufficient response from Mexico and how the US might measure whether the problems have been solved. That could make it difficult for each side to resolve the conflict, and difficult for the markets to anticipate outcomes. With the announcement of a potential US-Mexico conflict, the market appropriately marked up its expectations for volatility.

Dropping expectations for growth and inflation

Since May 9, rates on 10-year US TIPS have dropped from 0.59% to 0.39%, implying an expected drop in economic growth. And breakeven inflation has dropped from 1.86% to 1.74%. In Germany, where real growth has been running at less than half a percent, rates on government inflation-index debt has barely moved from -1.32% to -1.31%. But German breakeven inflation has dropped from 1.26% to 1.11%.

Generally wider spreads

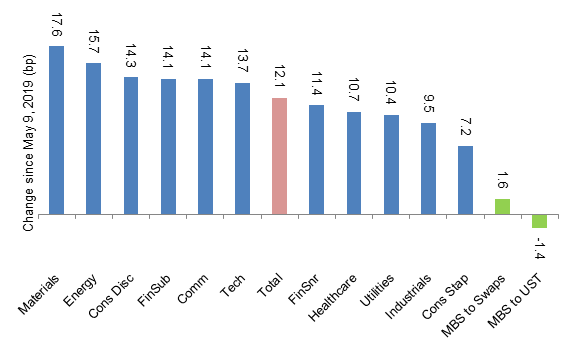

Credit spreads have widened since May 9 broadly reflecting the parts of the US economy most exposed to global trade (Exhibit 1). Investment grade materials, energy and consumer discretionary issuers—the later including aerospace and auto issuers–have widened the most. Consumer staples, industrials and utilities have widened the least.

Exhibit 1: Wider spreads on corporate debt since May 9, limited change in MBS

Note: data show OAS on corporate debt. Source: Bloomberg, Amherst Pierpont Securities

The nominal spread of MBS to the swap curve has widened by less than 2 bp since May 9, and the spread to the Treasury curve has actually tightened slightly. The limited move in MBS spreads suggests flow from corporates or other assets into MBS.

Correlations shift

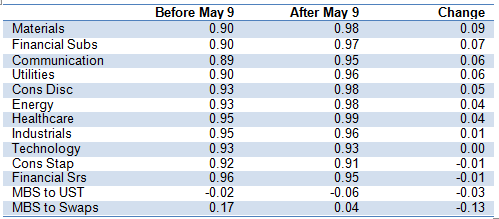

Correlations between parts of fixed income have started to subtly shift, too. The correlation between aggregate investment grade credit spreads and subsectors of the investment grade market, for instance, have moved slightly higher from already high levels (Exhibit 2). MBS again stands apart as already low correlations have become slightly lower. The falling correlation between credit and MBS also suggests some flows from credit into MBS.

Exhibit 2: Correlations within credit rise, between credit and MBS fall

Note: Before May 9 covers 60 sessions, after May 9 covers 21 sessions. Correlations are between daily spread changes in each sector and daily changes in the Bloomberg All Cash Bonds OAS. Source: Bloomberg, Amherst Pierpont Securities

Investment implications

The last few weeks arguably show the relative sensitivity of different market sectors to rising trade tensions. For most investors, it is extremely difficult to know the timing and direction of the next rounds of developments. For those investors, it is better to deleverage exposure to a likely persistent and growing risk. Investment performance since May 9 is a good guide to safe harbor.

* * *

The view in rates

Trade friction has now driven the US 10-year yield to 2.12%, and Fed Vice Chair Clarida has noted that trade friction could lead the Fed to ease . The market in the last week has raised the odds of a Fed cut this year from 80% to 95%. Threats to growth compound concerns about low inflation as reflected in recent remarks by Fed Governor Lael Brainard. Persistent volatility from trade conflict stands to keep yields low or drive them lower for now.

The view in spreads

Spreads in credit should continue to widen as trade frictions pick up. It’s an appropriate repricing as prospective global growth comes under pressure. Agency MBS could see a softening of bank demand, but it should still outperform credit. Since the US announced new tariffs on China on May 9, MBS has performed much better than credit, and correlations suggest flows from credit into MBS. That should continue.

The view in credit

Corporate credit on the margin looks like it is improving from its state last year. Various measures of leverage paint a mixed picture, but many are improving. Companies have started to divert cash flow toward paying down debt, have started to sell non-core assets and have curtailed stock buybacks. Management has heard the concerns of debt investors. Households continue to look strong with low unemployment, rising home prices, and generally good performance in investment portfolios.