Uncategorized

Ratings transitions in Freddie K deals

admin | August 9, 2019

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors.

Strong price appreciation in multifamily properties coupled with increased incentives to refinance at lower rates has pushed defeasance levels in Freddie K deals to all-time highs. Ratings on seasoned B and C classes have climbed as a greater percentage of the underlying commercial mortgage loans are replaced with Treasury securities, enhancing credit support. Defeasance levels are expected to continue to trend higher in the near term. The prepay protection and potential for upward ratings migration has made Freddie B and C classes an attractive alternative to residential MBS and BBB-rated corporate debt.

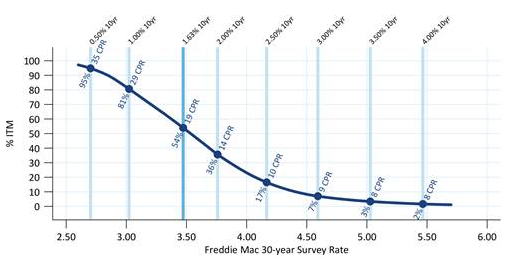

The building refinance tsunami

Prepay speeds on 30-year mortgages picked up more than 30% in July when the 10-year Treasury yield was still above 2.00% and 36% of outstanding conventional 30-year mortgages were in-the-money to be refinanced. The latest rally in Treasury rates has pushed approximately 50% of these mortgages into the refinance window (Exhibit 1), and speeds are expected to surge higher. A complete discussion is in the APS prepayment report, here.

Exhibit 1: % of MBS that are in-the-money for various 10-year Treasury rates

Note: A mortgage loan is considered to be in-the-money when its coupon is 75 bp above the current Freddie Mac Primary Mortgage Market Survey rate. Source: Fannie Mae, Freddie Mac, eMBS, Amherst Pierpont Securities

Banks and insurers appear to be avoiding some of the negative convexity risk by migrating towards agency CMBS, using Freddie K deal A and AM pieces as a replacement for agency MBS, and as an alternative to corporate AAA to AA-rated paper, which tends to be substantially less liquid. For a complete discussion, see the APS piece, Banks become negative on negative convexity.

Investors willing to go down in credit and forgo the agency guarantee can consider the B and C classes of Freddie Mac K deals. Commercial mortgage loans in Freddie K deals are locked out from prepaying until they have only 6 months remaining to maturity. Borrowers who wish to prepay their loans in order to refinance or sell the property must defease the loan with Treasury securities. These B and C classes have a variety of ratings from BB to AAA, and tend to migrate upwards in the ratings as they season, because a greater proportion of the loans are defeased with Treasury’s over time. This can be seen in the ratings transition matrix which covers most of the universe of Freddie K B and C classes.

Defeasance rises on multifamily strength

Strong performance across the multifamily housing sector has resulted in all-time high levels of defeasance in Freddie K-deals, and a new trough in the amount of supplemental financing, according to a report by Kroll Bond Rating Agency (KBRA). Multifamily price growth was 2.1% in 1Q 19 and 8.5% for the trailing twelve month period. That’s after an 11.3% increase for the trailing twelve month period in March 2018, according to data from CoStar Group. The unpaid principal balance that has been defeased in Freddie K-deals rose 86% year-over-year to $3.86 billion, an all-time high. The defeasances contributed to eight upgrades on Freddie K-deals rated by KBRA. The amount of supplemental debt taken out by borrowers fell 36% to $254 million. It’s unclear whether the drop in supplemental debt is due to caution on the part of borrowers or Freddie Mac. Defeasances are expected to keep rising over the near term based on continued price appreciation of multifamily properties and strong incentives to refinance, meaning ratings upgrades of Freddie B and C classes are likely to continue.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2024 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.