Uncategorized

Callable bank structures present alternative to corporate bullets

admin | August 23, 2019

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors.

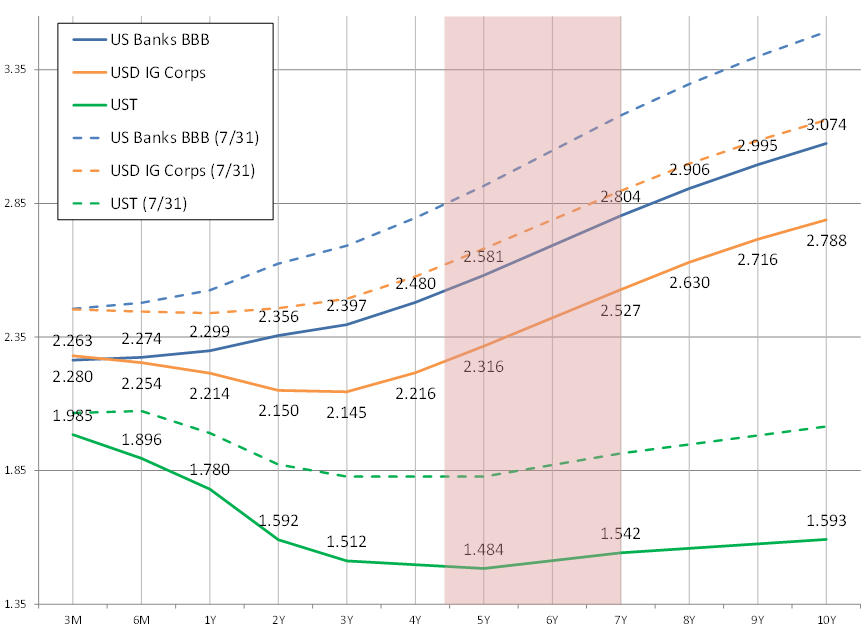

Rapid compression in the yield curve since month-end has limited opportunities for yield hungry investors in USD fixed income product. Despite the relative attractiveness of US corporate bond yields versus the global landscape, investors have been reluctant to bid intermediate bullets, seeing valuation as too flat, and seeking better opportunities elsewhere (Exhibit 1).

Exhibit 1: Current yield curves vs. month-end (7/31/19)

Source: Bloomberg, Amherst Pierpont Securities

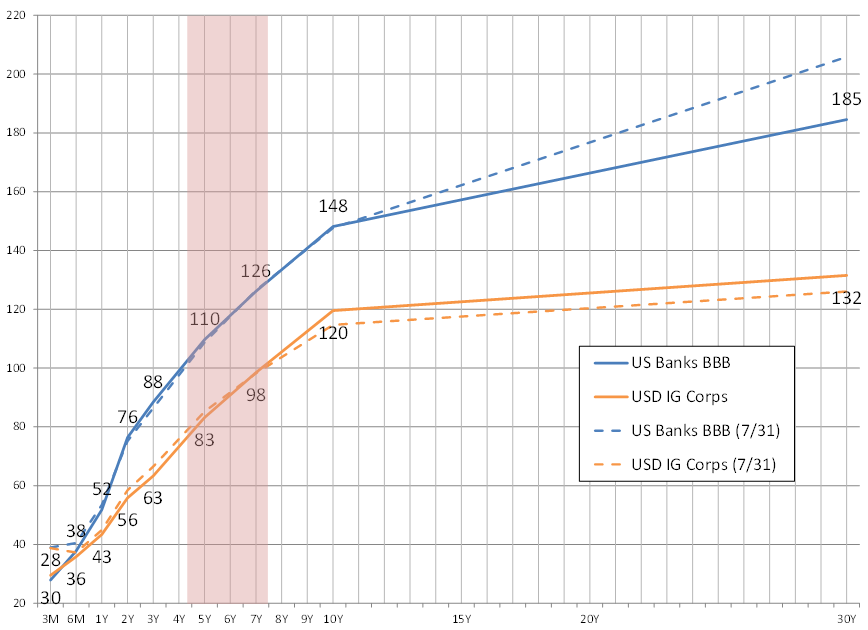

Likewise, spreads have remained little changed in aggregate from the start of the rate rally, but with much flatter curves that are making it difficult to identify better values or attractive entry points for corporate buyers (Exhibit 2).

Exhibit 2: Current spread curves vs. month-end (7/31/19)

Source: Bloomberg, Amherst Pierpont Securities

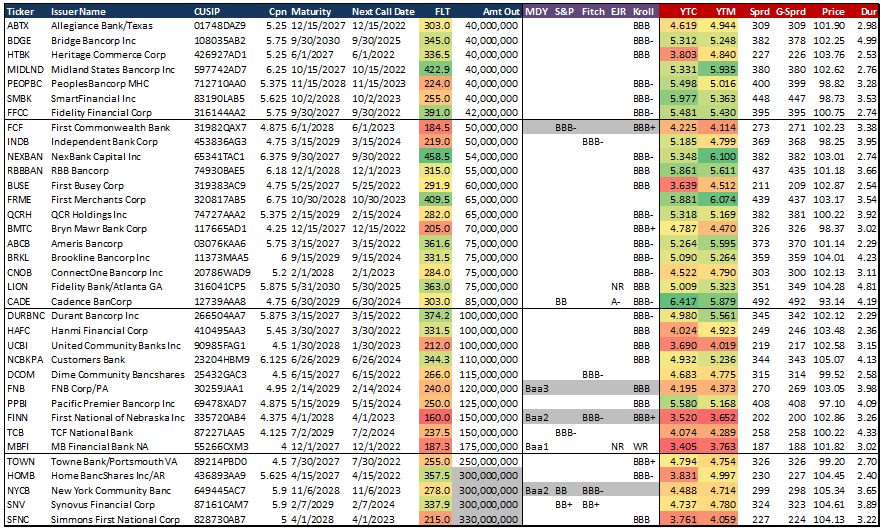

An area of the market highlighted previously, in Mining liquidity in private bank placements, as a source of value for corporate bond investors is in the US large community and smaller regional bank space. The sector not only contains a broad cross section of high quality, under-covered credits, but also is heavily populated by callable structures that are particularly attractive in this rate environment. Many of the deals in this cohort that were issued over the last 3-4 years were structured as fix-to-float 10-year final maturities with a 5-year par call (10NC5), and mostly with attractive back-end floating spreads (Exhibit 3). Many of these deals have now aged into 8NC3 and 7NC2 instruments as well, which is an attractive alternative for investors that are currently unimpressed with total yields in intermediate bullets in the financial sector.

Exhibit 3: Examples of community bank bonds with 3- to 4-year call structures

Note: Bonds listed mostly trade by appointment. Source: Bloomberg/TRACE – indications only, Amherst Pierpont Securities

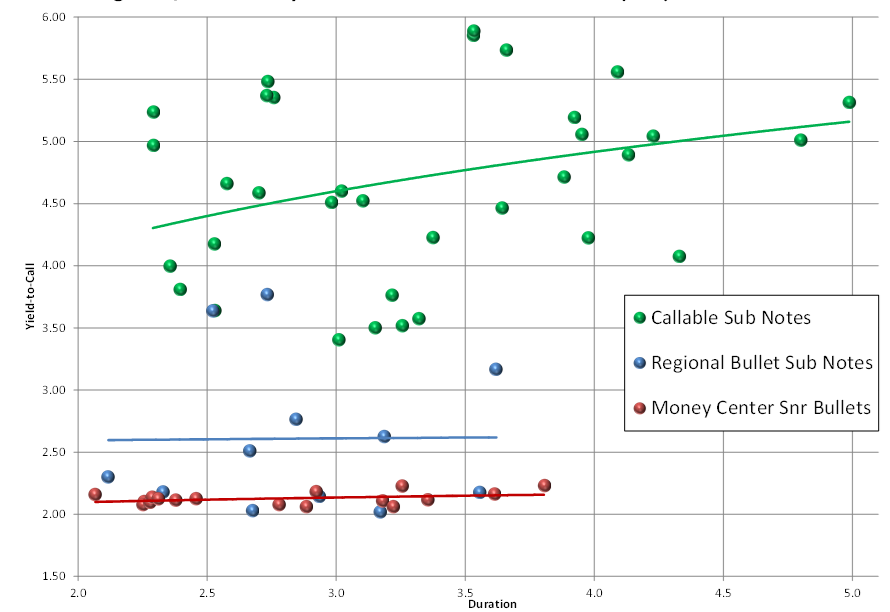

There are good value bonds in this segment on both a yield-to-call (YTC) and yield-to-maturity (YTM) basis. On a pure economic basis is does appear many of the issuers would or should be compelled to call if rates remain under pressure. Nevertheless, these are infrequent (and even first-time) issuers in the public debt markets, which could impact their willingness or motivation to re-issue. In which case, investors are protected with the generous spreads offered in the back-end.

Exhibit 4 illustrates how these bonds are currently pricing on a YTC basis versus:

- a sample of bullet maturities in investment grade regional bank sub notes, and

- senior unsecured bullets of the IG money center banks (BAC, C, JPM, WFC).

This provides additional context of the alternative yield opportunities available to IG investors with the same duration profile (or lack thereof). As indicated in Exhibit 3, there are even opportunities for investors to stay in index eligible deal size as well as achieve one or more investment grade ratings.

Exhibit 4: Attractive YTC opportunities – community bank sub callables vs. regional sub and money center senior bullets

Note: Bonds listed mostly trade by appointment. Source: Bloomberg/TRACE – indications only, Amherst Pierpont Securities

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2024 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.