Uncategorized

Assessing risk from use of eminent domain

admin | October 10, 2019

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors.

The loss of affordable housing stock, particularly in high-cost, densely populated markets, has led the King County Housing Authority (KCHA) in Washington State to implement a novel solution: buy up existing multifamily properties through eminent domain and preserve the units as low- to middle-income housing. The KCHA began identifying apartment complexes and authorizing acquisition in October 2018. A $60 million loan to the program from Microsoft – part of a $500 million pledge to fight the region’s housing affordability crisis – has added momentum and triggered prepayments in loans backing agency CMBS. And the idea could spread to the San Francisco area next.

Three loans for apartment complexes in the Seattle area subject to the KCHA program have so far prepaid, though with different impact on investors. The first loan, which was in a Freddie K-deal, was defeased in March 2019. The next two loans, which happened to be in Fannie DUS pools, prepaid at par without yield maintenance following through to investors. It seems likely that the disparate resolution was due to a voluntary defeasement by the Freddie Mac borrower, though its remotely possible it could be the result of a bespoke clause in the particular contract. Assessing this investment risk attached to the use of eminent domain has taken on renewed importance, as the strategy could become more widespread. Google recently pledged $1 billion in capital to fund affordable housing in Silicon Valley.

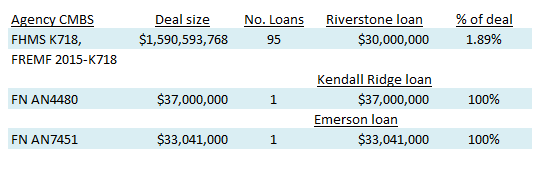

The bonds impacted by the initiative in King County

King County passed resolutions over the past year to purchase five existing moderate- to low-income multifamily apartment buildings (Exhibit 1). The county took two of the properties – Riverstone and Kendall Ridge apartments – by eminent domain and bought the other three properties, which do not appear to have had any outstanding loans in securitized deals, through private transactions.

Exhibit 1: Apartment buildings acquired by King County Housing Authority

Source: King County Housing Authority, Bloomberg, Amherst Pierpont Securities

A disparate impact for investors

Borrowers are typically required to promptly notify lenders of any action or proceeding related to a proposed or actual taking by eminent domain or conveyance in lieu of a taking.

Fannie Mae recently posted an announcement on their website of multifamily properties purchased through eminent domain and a FAQ regarding the KCHA actions. Fannie Mae states in the announcement that:

“Our mortgage loan documents do not require a borrower to pay a prepayment premium in the event of a condemnation (which is the process through which the eminent domain power is exercised) resulting in the early receipt of all or a portion of the principal of a loan. Our MBS prospectus discloses that a prepayment premium is not required to be paid by the borrower in the event of an involuntary prepayment resulting from the receipt of amounts received in connection with a condemnation action affecting a property.”

What’s unclear is why the loans for the three properties taken by eminent domain had disparate resolutions, which resulted in different impacts on the investors (Exhibit 2). The Riverstone loan in the Freddie Mac K-deal was defeased – which has a positive impact on the deal as it removes credit risk and maintains the required interest and principal payments throughout the original term of the loan.

Exhibit 2: Agency CMBS deals containing the affected loans

Source: Bloomberg, Amherst Pierpont Securities

The Kendall Ridge and Emerson loans in the Fannie Mae DUS pools were prepaid without prepayment penalties attached, so that pools which had been trading at a premium were suddenly paid back at par without additional compensation to the investors.

The KCHA initiative to increase affordable housing is currently slated to continue through 2021. Fannie Mae DUS pools contain $5.1 billion of loan exposure throughout the county and Freddie Mac K-series contain $3.8 billion, but only a fraction of that would likely satisfy the KCHA requirements for location and affordability for moderate- to low-income renters if they do expand their purchase program of multifamily properties.

An involuntary prepayment may not require prepayment premiums

The taking of a property by eminent domain or a sale in lieu of a taking are legally acts of condemnation on the property. The condemnation action does not reference the condition of the property – it refers only to the action of the government taking physical possession and legal title to the property.

Prepayments as a result of, or in lieu of, a condemnation action are both considered involuntary. The rights of the property owner and the mortgage lender as potential condemnees vary significantly by state and local jurisdiction. The attachment of prepayment penalties in the event of condemnation is governed by several sections of the overall mortgage loan documents, including the condemnation clause, which can vary by state and jurisdiction depending on applicable law.

See the Appendix: That’s the law for more background on eminent domain and condemnation.

The risk that involuntary prepayments may not require prepayment premiums are reflected in the multifamily prospectus of both Fannie Mae and Freddie Mac.

Excerpted from Fannie Mae’s Multifamily MBS Prospectus Supplement, edited for brevity (page 3 of 13):

Involuntary Prepayment of the Mortgage Loan

If casualty insurance proceeds or funds received in connection with a condemnation action affecting the mortgaged property are used to reduce the unpaid principal balance of the mortgage loan, the resulting reduction in the unpaid principal balance may result in certificateholders receiving an early prepayment of principal of the certificates. The borrower would not be required to pay a prepayment premium in this case.

The multifamily prospectus for each agency securitization and the offering circulars for a particular deal incorporate the risks of to the deal and the collateral as a whole. Freddie Mac’s offering circular also indicates that prepayment in the event of condemnation may not require a prepayment premium. That would certainly be specifically covered in the underlying documents for each mortgage loan, but those are not made available to investors.

Unfortunately without additional disclosure its unclear whether there was a bespoke clause in the Riverstone mortgage loan documents that required defeasance in the event of a condemnation action – which seems exceedingly unlikely – or whether the owner voluntarily defeased the loans from the condemnation proceeds. Please see the Appendix for further information on the standard condemnation clause in a Freddie Mac multifamily loan, though given the variations of state and local jurisdiction it’s not possible to draw conclusions.

California law does not cover prepayment penalties

The San Francisco metropolitan area currently boasts, or suffers from, the highest housing costs in the nation. Google recently pledged $1 billion over the next 10 years to help ease the housing crisis in Silicon Valley. At this time the commitment from Google does not designate funds for local housing authorities to purchase existing multifamily properties akin to the effort in King County. However, it’s certainly possible that Google or other companies could follow Microsoft’s lead, or California housing authorities could pursue a similar initiative on their own. Notably the California Code of Civil Procedure § 1265.240 states that:

“Where the property acquired for public use is encumbered by a lien, the amount payable to the lienholder shall not include any penalty for prepayment”.

Again, it’s unclear whether bespoke mortgage loan contracts for properties in the state could require the mortgagor to pay prepayment penalties in the event of a taking, but the state will not explicitly include the fees as part of their payment.

Appendix: That’s the law

The taking of private property through eminent domain

Eminent domain refers to the right of the federal or state government to expropriate private property for public use. The Fifth Amendment to the Constitution places an important limitation on the federal government’s power, stating in part: “…nor shall private property be taken for public use, without just compensation.” This part of the Fifth Amendment is known as the “takings” clause. The Supreme Court ruled that the takings clause also applies to state governments through the Fourteenth Amendment to the Constitution.

The just compensation part of the takings clause has been interpreted to mean that any government that does take property for public use must fully compensate the owner of the property for the taking. Generally speaking this means that in a complete taking the property owner is compensated at fair market value.

The best tutorial on the subject appears in the article, What’s In Your Condemnation Clause? by George Kroculick and Michael McCalley, lawyers at Duane Morris. Importantly state and local law can determine whether a mortgagee (lender) is named or has any rights in a condemnation proceeding.

From Kroculick and McCalley (page 1-2 of 4):

II. Notice of the Taking and Rights of Mortgagees to Participate in Condemnation Case

Whether a mortgagee is named a party in a condemnation case will likely depend on state law and how the term “condemnee” or “owner” is defined in a jurisdiction’s relevant statute. In some jurisdictions, the relevant statute requires that owners and any persons having an interest in the property being condemned shall be joined as parties. In others, absent an express statutory requirement, mortgagees with a mere security interest in the property condemned need not be made a party to the action. …

Due to the varied treatment of mortgages and the rights they convey, the method of participation by a mortgagee will vary from state to state. Some jurisdictions allow the mortgagee to participate fully in an action against the condemnor. Others allow the mortgagee to participate only to the extent necessary to claim its portion or allocation of the condemnation proceeds. Yet, a few jurisdictions only provide that the mortgagee maintains a remedy against the mortgagor. Consequently, mortgagees should seek to reserve the fullest protections and rights of participation as granted under the controlling law when drafting a condemnation clause.

III. Rights of Parties to the Proceeds/Impact Where Rights Are Assigned to Mortgagee

Most standard condemnation clauses address the mortgagee’s right to the condemnation proceeds, and may go so far as to establish the distribution as between mortgagor and mortgagee. Typically, the clause includes a provision whereby the proceeds of any award or claim for damages in connection with any condemnation or conveyance in lieu of condemnation is assigned to the mortgagee. Such a clause is intended to give the mortgagee the unfettered right to the condemnation proceeds. While this language protects the mortgagee’s interest and gives the mortgagee a right to as much of the condemnation proceeds needed to satisfy the outstanding mortgage obligation, it may have unintended consequences.

An example condemnation clause in Freddie Mac’s loan template

There is a boilerplate multifamily loan and security agreement available on Freddie Mac’s website that does contain a condemnation clause. That clause states in part (page 46, section 6.11):

Condemnation

Rights Generally. Borrower will promptly notify Lender in writing of any action or proceeding or notice relating to any proposed or actual condemnation or other taking, or conveyance in lieu thereof, of all or any part of the Mortgaged Property, whether direct or indirect (“Condemnation”). Borrower will appear in and prosecute or defend any action or proceeding relating to any Condemnation unless otherwise directed by Lender in writing. Borrower authorizes and appoints Lender as attorney in fact for Borrower to commence, appear in and prosecute, in Lender’s or Borrower’s name, any action or proceeding relating to any Condemnation and to settle or compromise any claim in connection with any Condemnation, after consultation with Borrower and consistent with commercially reasonable standards of a prudent lender. This power of attorney is coupled with an interest and therefore is irrevocable. However, nothing contained in this Section 6.11(a) will require Lender to incur any expense or take any action. Borrower transfers and assigns to Lender all right, title and interest of Borrower in and to any award or payment with respect to (i) any Condemnation, or any conveyance in lieu of Condemnation, and (ii) any damage to the Mortgaged Property caused by governmental action that does not result in a Condemnation.

Application of Award. Lender may hold such awards or proceeds and apply such awards or proceeds, after the deduction of Lender’s expenses incurred in the collection of such amounts (including Attorneys’ Fees and Costs) at Lender’s option, to the Restoration or repair of the Mortgaged Property or to the payment of the Indebtedness, with the balance, if any, to Borrower. Unless Lender otherwise agrees in writing, any application of any awards or proceeds to the Indebtedness will not extend or postpone the due date of any monthly installments referred to in the Note or Article IV of this Loan Agreement, or change the amount of such installments. Borrower agrees to execute such further evidence of assignment of any Condemnation awards or proceeds as Lender may require.

Fannie Mae’s approach and language regarding condemnation is substantially similar, though it is enumerated across different sections of their loan documents. Fundamentally both agencies appear not to require that prepayment penalties and/or defeasance occur in situations of involuntary prepayment.