Uncategorized

Marking-to-market the LIBOR to SOFR transition

admin | January 24, 2020

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors.

When the day finally comes for LIBOR to go the way of the dinosaur, at least if regulators have their way, investors worldwide will see their securities reset to float off of SOFR plus a spread. That new coupon may or may not match the one investors would have seen if LIBOR survived, and the change in coupon may mean a change in market value. The Alternative Reference Rate Committee, or ARRC, in the last week has unveiled a proposal to set that critical spread. If LIBOR were to die now, investors in securities indexed to 1-month LIBOR would experience a 3 bp drop in the first coupon set to 1-month SOFR plus the prescribed spread. This coupon difference will almost certainly evolve over time, and the prices of LIBOR-indexed securities may begin to reflect that evolution.

The ARRC proposal

ARRC’s recently published consultation proposes a spread adjustment approach designed to minimize the expected change in value of cash products when the LIBOR benchmark is replaced by SOFR plus a spread. The approach includes a few highlights:

- It uses a different spread adjustment for each tenor of LIBOR–1-month, 3-month, 6-month and 1-year—although the methodology used to calculate the adjustments will be the same.

- It fixes the spread once and for all at a specified time at or before LIBOR’s cessation to reflect the historical differences between LIBOR and SOFR and make the spread-adjusted SOFR rate comparable to LIBOR.

- The approach will mostly likely calculate the spread as the median historical difference between LIBOR and a SOFR rate of the same tenor over a 5-year lookback period. This is consistent with the spread adjustment method proposed and likely adopted by ISDA for derivatives contracts that reference LIBOR.

- The adjustments apply to LIBOR contracts that have incorporated ARRC’s recommended fallback language, or for legacy LIBOR contracts in which parties have and exercise the discretion to select the ARRC recommended spread-adjusted rate as a fallback.

The proposal allows investors and issuers of existing cash securities tied to LIBOR to begin to evaluate the potential market impact that the transition could have on their holdings.

Estimating the spread adjustments

Throughout the consultation, ARRC analyzes three possible constructions of SOFR rates that match LIBOR tenors, along with three spread methodologies for calculating the spreads (Exhibit 1). Despite the nine possible combinations that ARRC evaluates, the proposal clearly leans towards a 5-year median spread methodology, in part because it is consistent with the methodology chosen by ISDA.

Exhibit 1: Scenarios evaluated in spread adjustment for e.g. 1-month LIBOR

Source: ARRC

ARRC prefers to transition to forward-looking term rates, and places those first in the recommended waterfall in their recommended fallback language for loan and securities contracts. Utilizing those rates crucially depends on the development of a robust SOFR futures market prior to the transition, and ARRC notes repeatedly that it cannot guarantee the availability of forward-looking term SOFR rates.

ISDA has chosen to develop fallback SOFR rates of various tenors using compounded averages of overnight SOFR set in arrears, and the spread adjustment will use a historical median over a 5-year lookback period (Exhibit 1, cell highlighted in yellow), based on this ISDA consultation. For comparative purposes the spread adjustments are calculated using ISDA’s methodology and a workbook developed by the Brattle Group that ISDA has made available in their consultation (Exhibit 2).

Exhibit 2: Estimated spread adjustment applied to SOFR to make it comparable to LIBOR

Note: The spread adjustments are applied to SOFR compounded setting in arrears rates. The estimates are calculated using the Brattle Group workbook which uses a historical time period that ends on 6/28/2019. Actual compounded SOFR rates and spread adjustments will vary based on the when the transition occurs, whether a lockout period applies, and any technical issues related to the calculations that are addressed prior to implementation.

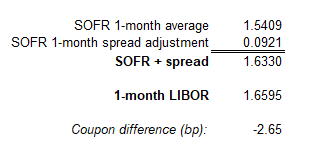

What if the transition occurred now?

As an example, assume the transition to LIBOR occurred on January 21, 2020, and the 1-month LIBOR coupon reset to SOFR + spread. The first SOFR-based coupon would be 2.65 bp below the 1-month LIBOR coupon (Exhibit 3).

Exhibit 3: Example 1m SOFR + spread coupon compared to 1m LIBOR

Note: See explanatory note in Exhibit 2. All computations as of 1/21/2020. Source: ISDA, Brattle Group, Bloomberg, Amherst Pierpont Securities.

The estimated spread adjustments and SOFR-based coupons will vary over time. It’s reasonable to assume that sometimes the SOFR-based coupons might be above their comparable LIBOR coupons, and at other times they will be below. The question is how the market will react to the shift, and whether there will be a repricing of LIBOR-based securities ahead of the transition if it seems likely that the SOFR-based coupons will often or persistently be a few basis points below those tied to LIBOR.

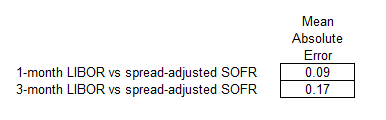

ARRC synthetically created bonds indexed to SOFR-based fallback rates and compared them to LIBOR-based bonds to evaluate differences in total return over historical periods. The historical errors between returns of a hypothetical 1-month or 3-month LIBOR loan or security and the return of a SOFR-based one (Exhibit 4) shows that, on average, there is a market value transfer between the two securities of 9 bp and 17 bp, respectively.

Exhibit 4: Historical errors between returns on a LIBOR loan and spread-adjusted SOFR

Note: Loans with 5-years remaining maturity, sample period Jan 1999 – May 2019, SOFR adjustments and rates use 5-year median look-back period and compound averages in arrears. Mean absolute error is based on annualized differences in returns (in percentage points). Complete results across all methodologies and other tenors are available in ARRC’s consultation. Source: ARRC, FRBNY, Federal Reserve Board, Refinitiv, and Federal Reserve Board staff calculations.

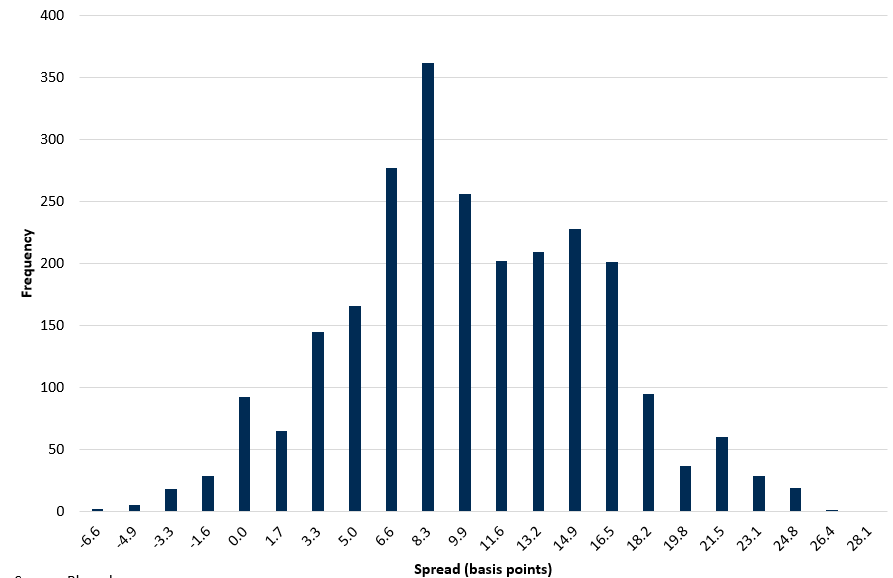

Although the mean absolute errors don’t indicate that the value transfer is typically in favor of the LIBOR securities, it’s almost certainly the case given the propensity for unsecured, bank credit sensitive, forward-looking LIBOR rates to rise during periods of financial stress or tightening regimes relative to secured, nearly risk-free, compounded overnight SOFR. The distribution of the difference between the two rates is not normal, but tends to be fat-tailed with occasional large, positive differences when LIBOR exceeds SOFR (Exhibit 5).

Exhibit 5: Frequency of historical spreads between 1m LIBOR and 1m SOFR

Note: SOFR is 30-day compounded average in arrears. Source: Brattle Group, Bloomberg.

It is unclear how much historical analysis and spreads will matter to market participants when LIBOR is being decommissioned. Given that the spread adjustment as contemplated does not make the transition market value neutral, if SOFR-adjusted coupons remain below those of LIBOR coupons its possible that LIBOR-based securities that mature after the transition will cheapen over time.

The latest ARRC proposal highlights one of the most specific and important risks in the LIBOR-to-SOFR transition. It affects all outstanding LIBOR-indexed securities, and the market has just started to understand and price the risk.