Uncategorized

Lessons from the Fed’s agency CMBS operations

admin | April 17, 2020

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors.

The Fed’s decision to buy agency CMBS has quickly stabilized the market and tightened spreads for Fannie Mae DUS, for the guaranteed classes of Freddie Mac K-series and for Ginnie Mae project loans. This has occurred evenly across products despite decidedly uneven investor participation, reflecting differences in financing and liquidity. Fed support has not passed through to the unwrapped classes, where spreads remain so wide that Freddie Mac declined to issue B and C class securities in a recent deal in favor of expanding the AM class, absorbing the credit risk because it was uneconomical to sell into the market at current levels.

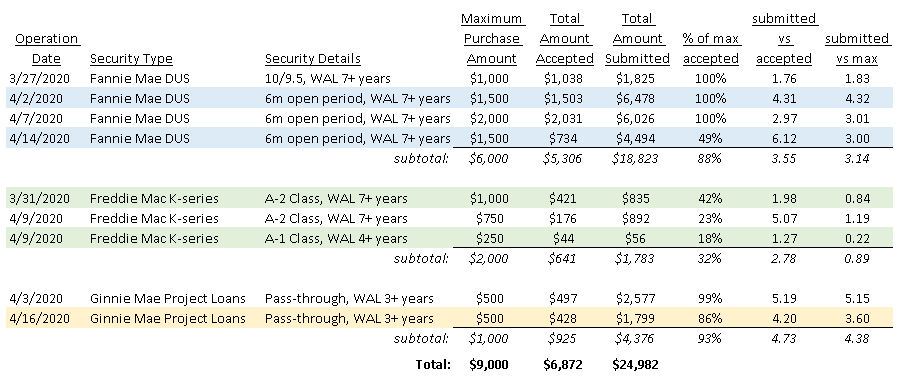

There are a few noteworthy takeaways from the results of the first few operations in agency CMBS (Exhibit 1). The size of the Fannie Mae DUS operations have been considerably larger than those for Freddie K-series, and the uptake has been stronger in both DUS and Ginnie Mae project loans than in Freddie Ks. So far, the Fed has conducted four DUS operations with a maximum total purchase size of $6 billion and an actual accepted amount of $5.3 billion (88%). The two operations in Ginnie Mae project loans have been 4.4x oversubscribed, and the Fed has taken 93% of the $1 billion maximum to date. As for Freddie K-series, the Fed has so far has conducted three operations with a maximum total purchase size of $2 billion but total purchases of only $641 million (32%).

Part of the imbalance has no doubt been driven by the greater investor participation in DUS operations. On average the DUS operations have been more than 3x oversubscribed, while Freddie K-series operations have been undersubscribed. In two of the three Freddie K-series operations so far, the face amount of bonds offered by primary dealers and investors was slightly (0.8) to significantly (0.2) below the maximum purchase amounts.

Exhibit 1: Summary of Fed agency CMBS operations ($ in millions)

Source: New York Federal Reserve, Amherst Pierpont Securities

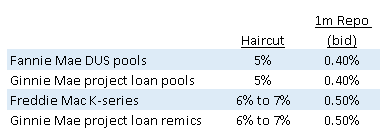

The greater participation by investors and primary dealer in the Fannie versus Freddie CMBS operations is due to a difference in the investor base between the two, which is driven by a difference in financing. Leveraged investors, particularly mortgage REITs, are more likely to be overweight Fannie Mae DUS relative to Freddie K-series because the DUS pools have a financing advantage that makes them cheaper and more liquid to own. DUS pools fit into FICC’s GCF (general collateral financing) bucket, whereas structured securities like REMICs do not. DUS funding is therefore cheaper with lower haircuts (Exhibit 2), making them a more attractive asset for leveraged accounts.

Exhibit 2: Financing comparison for agency CMBS

Note: Indicative levels only. Source: Amherst Pierpont Securities

When the COVID-19 crisis escalated in mid-March many mortgage REITs failed and other accounts were forced to rapidly delever. This put more pressure on spreads and left an overhang of Fannie Mae DUS pools that needed to be absorbed, some of which likely ended up on primary dealer balance sheets.

The higher levels of participation in Ginnie Mae project loan operations compared to those for Freddie K-series are not due to a financing difference. The Fed operations are not focusing on project loan pools, which enjoy the same advantage as DUS pools, but instead on the project loans that are structured as pass-throughs and front sequentials, which are REMICs and finance similarly to K-series. These Ginnie Mae project loans tend to be less liquid overall because the market is smaller and there can be significant uncertainty regarding prepay speeds. Investors with high premium project loan securities in particular tended to offer bonds into the Fed’s open market operations in order to raise cash or get out of positions at acceptable levels.

Freddie Mac skips issuing B and C classes in recent K-deal

Freddie K-deals often include B and C classes which are not wrapped with the agency guarantee, and offer investors the opportunity to earn more yield in exchange for accepting some credit risk on the deal. In a typical deal the equity tranche absorbs the first 7.5% of credit risk, the C class covers 7.5% to 10% of losses, and the B class takes any losses that account for between 10% to 14% of the underlying principal balance.

Prior to the crisis, spreads on the B and C classes at issuance were in the range of 150 bp and 200 bp over swaps, respectively. Those spreads are currently in the range of 375 bp and 525 bp, down from higher altitudes they touched a few weeks ago.

Freddie Mac’s multifamily guarantee fees can vary according to the type of collateral, the loan characteristics, the purpose of the loans and other factors. The guarantee fee in the FHMS 2020-K106 deal which was marketing in late February and priced on 3/17/2020, contained both FREMF B and C classes, and the guarantee fee was 20 bp according to the offering circular supplement.

The FHMS 2020-K107 deal priced 4/15/2020 and contained no B or C classes. The principal balance usually allocated to those classes was rolled into the AM class, meaning all by the 7.5% of the deal allocated to the equity tranche was wrapped with Freddie’s guarantee. The guarantee fee on the K107 deal was 30 bp. The incremental cost of increasing the guarantee fee to wrap the 7.5% to 14% of the deal was likely much cheaper than issuing B and C classes with yields in the neighborhood of 5.00% to 6.50%. As more deals come to market it will be interesting to see if spreads tighten enough to make the economics more attractive or if Freddie continues to be the agency guarantor of last resort.