Uncategorized

CLOs: Price coverage of CLO loans keeps improving

admin | April 12, 2019

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors.

CLO loan pricing and the transparency of performance and risk continue to improve. Between Intex and Markit, unpriced broadly syndicated loan principal in CLO portfolios today has dropped to less than 6 bp. Unpriced loans show wider average spread, lower ratings and more defaults. They also come more frequently from industries with commodity exposure or from computer or electronics businesses. While not all prices are equal, the broad coverage creates a valuable check for CLO investors.

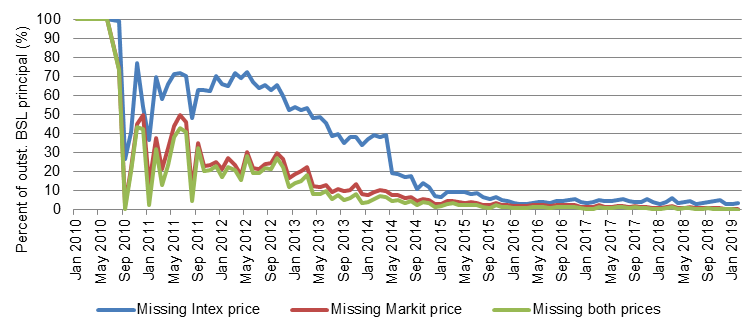

Pricing coverage for broadly syndicated loans has improved dramatically in the last decade (Exhibit 1). As recently as 2012, Intex had missing prices for 70% of loan principal in deals issued since 2010, and Markit had missing prices for 30%. By the middle of 2014, Intex had missing prices for less than 20% and Markit for less than 10%. As of February, Intex had missing pricing for 3.3% and Markit for 0.3%. Combining Intex and Markit left missing prices for less than 6 bp of principal.

Exhibit 1: Price coverage of broadly syndicated loans has improved dramatically

Source: Intex, Markit, Amherst Pierpont Securities calculations

Missing prices do signal slightly higher-than-average loan risk (Exhibit 2). Among loans without either an Intex or Markit price, 6.0% of principal is in default while loans with a price show only 0.2%. Unpriced loans show an average margin of 482 bp while priced loans show 345 bp. Unpriced loans also show a shorter original maturity than priced loans.

Exhibit 2: Unpriced loans show higher-than-average risk

| Statistics |

Has Intex or Markit |

Missing Intex and Markit |

| Balance ($ mm) |

496,373 |

275 |

| % Defaulted |

0.2 |

6.0 |

| Margin (bp) |

345 |

482 |

| WAM |

62 |

33 |

| WALA |

17 |

23 |

| Orig Term |

80 |

57 |

Source: Intex, Markit, Amherst Pierpont Securities

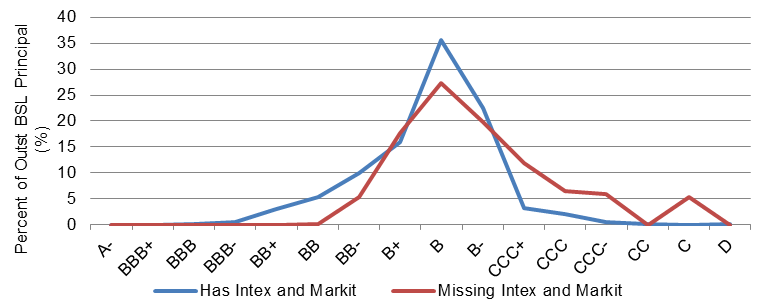

Loans without prices also show a rating distribution skewed to lower categories with a larger share of ‘CCC’ (Exhibit 3). Loans with prices consequently show a relatively higher share of ‘B’ and higher ratings.

Exhibit 3: Loans without prices show a larger incidence of ‘CCC’

Source: Intex, Markit, Amherst Pierpont Securities

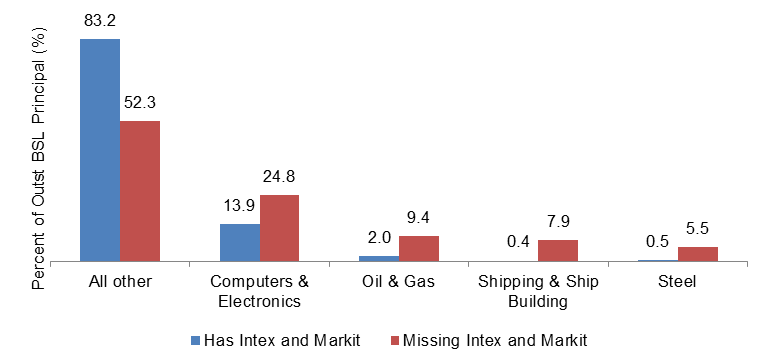

Loans without prices also tend to come disproportionately from computer or electronics businesses or industries with energy or commodity exposure (Exhibit 4).

Exhibit 4: Unpriced loans come from technology, energy or commodity sectors

Source: Intex, Markit, Amherst Pierpont Securities

Higher risk in unpriced loans likely argues for lower value than the average of all priced loans. The discount, of course, will depend on each loan’s margin, rating, industry and other factors.

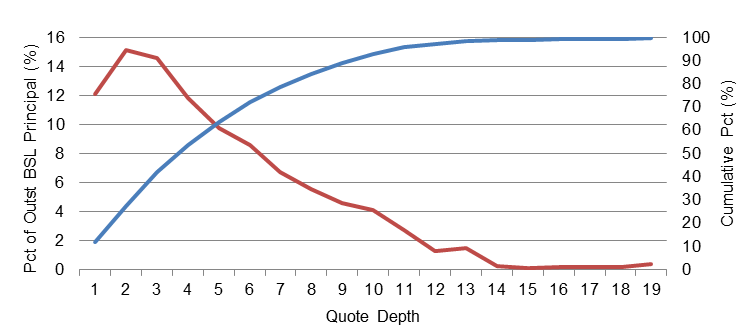

Even of the more than 99.94% of loans with prices, not all prices are equal. Nearly 42% of all priced loans have three or fewer market-makers. Of course, 58% have four or more (Exhibit 5). Fewer market-makers made price less reliable as a measure of tradeable value.

Exhibit 5: Nearly 42% of priced loans have three or more market-makers

Source: Intex, Markit, Amherst Pierpont Securities

Despite its limitations, the broad pricing of CLO loans offers valuable information about CLO loan portfolio performance and risk. The return on each loan and its volatility and correlation with other loans’ offers an alternative to rating agency or analyst views of risk and diversification. Investors in CLOs that use this information well arguably have one of the best and most timely views of collateral quality among investors in securitized products, where most collateral has no visible market price at all.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2024 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.