By the Numbers

JPMorgan makes a big move in risk transfer

Chris Helwig | October 18, 2019

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors.

JP Morgan looks like it’s making a run at a big change in the mortgage credit markets. The bank has launched a novel deal that would transfer credit risk on roughly $750 million of loans from its own portfolio into the capital markets. Instead of using securitization, the deal takes a page from the Fannie Mae and Freddie Mac programs for synthetic risk transfer. With regulators reportedly set to bless the deal for both risk-based and economic capital relief, it could pave the way for a new flow of credit out of bank loan portfolios and into other private hands.

Borrowing a page from Fannie Mae and Freddie Mac credit risk transfers

The deal, CHASE 2019-CL1, bears striking similarities to Fannie Mae and Freddie Mac credit risk transfer but with some key differences. Like the GSE transfers, the deal uses a reference pool of loans and credit-linked notes to transfer risk. Investors buy the credit-linked notes, and the sponsor can use the proceeds to cover future losses on the reference pool. As losses occur, the principal balance of the notes falls. In return, the deal pays a stream of income to compensate investors.

The CHASE structure differs from a traditional cash securitization in that principal and interest on the notes are unsecured general obligations of JPMorgan Chase Bank. That makes the deal a hybrid of both mortgage and unsecured corporate credit risk. The structure roughly parallels the approach used by both Fannie Mae and Freddie Mac in their credit risk transfer programs. The GSE deals put note proceeds into a trust that reinvests in highly rated commercial paper and other short-term instruments. Investors only have counterparty credit exposure through the stream of fees paid by the GSEs to the trust. Based on available pre-sale information, it is unclear whether the Chase deal uses the same fully funded trust structure or passes on note proceeds to the sponsor. Both the Chase deal and GSE CRT bonds pay uncapped 1-month LIBOR.

There are other differences between the JPMorgan and GSE approaches. First, JPMorgan is selling risk all the way through the ‘AA’ portion of the capital structure while the GSEs by and large only sell through ‘BBB.’ The JPMorgan deal uses a pro-rata structure on the five mezzanine classes with a locked-out first loss Class B, which provides a floor to the credit enhancement on the deal. Assuming the reference collateral is passing certain performance triggers, the five mezzanine classes will receive both scheduled and unscheduled principal. The pro-rata structure potentially makes deeper mezzanine bonds more negatively convex than the 4-tranche sequential structure commonly used by the GSEs. Since Chase is selling through ‘AA’ bonds, they are selling a thicker corridor of risk than the GSEs. Chase is transferring the credit risk on the first 8.00% of losses, roughly double the GSE transfer.

The JPMorgan transaction will not explicitly compete with GSE credit as the average loan size is nearly $775,000, well outside GSE loan limits. And while all the loans were underwritten to JPM’s guidelines; they were not tested for Qualified Mortgage or QM status in the diligence process and as a result were assumed to be non-QM in Fitch Ratings analysis of the pool. The collateral in the Chase reference pool is very similar to the high quality loans being securitized in their non-QM ‘ATR’ program, marked by high FICOs and low LTVs. The loans are also different from standard GSE CRT pools in that they have roughly four years of seasoning. Fitch’s base case expected pool loss is 20 bp.

Other key differences between the two programs include the maturity and call features of the transactions. The legal final maturity on the Chase transaction is consistent with that of the underlying reference obligations. The Chase deal employs a 10% collateral clean-up call as well as somewhat of a unique optional redemption. According to the Fitch presale documents, in a default or a regulatory event before October 2020 that would preclude Chase from getting the desired capital treatment from the transaction, the bank has the option to collapse the deal. In that case, the deal will pay off performing reference obligations at par and will pay off delinquent loans based on factors including LTV, unpaid interest, unpaid servicer advances and any forbearance associated with the loan. In contrast, Fannie Mae uses a 20-year non-call 7-year structure while Freddie Mac uses a 30-year non-call 10-year structure.

The motivation for JPMorgan

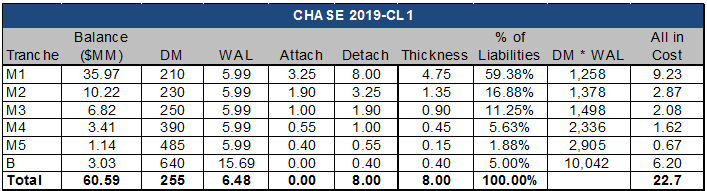

While pricing information on the transaction remains elusive, a few assumptions point to potential savings on regulatory and economic capital. Pricing on the tranches should parallel similarly rated new issue prime jumbo securitizations, and an additional 40 bp of spread for each tranche reflects the premium for 5-year CDS protection on JP Morgan Chase. The cost of insurance is then weighted by the portion of the reference pool that each tranche represents at its projected WAL. Based on this first step, the cost of risk transfer comes in at just less than 23 bp (Exhibit 1). And while it’s unclear what portion, if any, of the loans would be GSE eligible, the estimated cost of insurance is significantly less than current guarantee fees charged by the GSEs.

Exhibit 1: Calculating the cost of risk transfer

Source: Fitch Ratings, Bloomberg LP, Amherst Pierpont Securities

The transaction may reduce the regulatory risk-based capital on the loans, and a recent Asset-Backed Alert report suggests regulators would recognize that. Risk-based capital could fall from the current 4% required for 1- to 4-family mortgage to anywhere from 0% to 1.6%.. At a 4% capital ratio, assuming Chase’s current return on equity of 14.2%, the annual dividend cost of risk-based capital held against the loans is 57 bp. Reducing the regulatory and economic capital held against the position to 1.6% would drop the cost of capital to just 23 bp. And if the bank is able to get a 0% risk-based capital charge, it would completely eliminate any cost of for regulatory risk-based capital.

For JPMorgan Chase, as a G-SIB, requirements to hold minimum core equity capital of as much as 6% would prevent the bank from leveraging to the level implied by risk-based capital. However, the transaction would nevertheless give the bank more flexibility to manage risk-based and economic capital. The bank could possibly lower the equity capital held against the reference loans as long as it could find more capital-intensive assets that get it back on average to its minimum equity requirements.

Investment implications

Given the unique nature of the deal, the bonds should trade wide to comparable risk profiles in GSE CRT. The most obvious additional compensation that investors need is for counterparty credit risk. And while that can be measured in the corporate CDS market, there is likely some degree of correlation between the reference pool and corporate credit. Specifically, deterioration in the credit performance in the pool may come concurrent with economic downturns in high-cost areas where the bank has other concentrated risk. Investors also need compensation for the illiquidity associated with a transaction that may amount to little more than a thought experiment if not blessed by regulators.

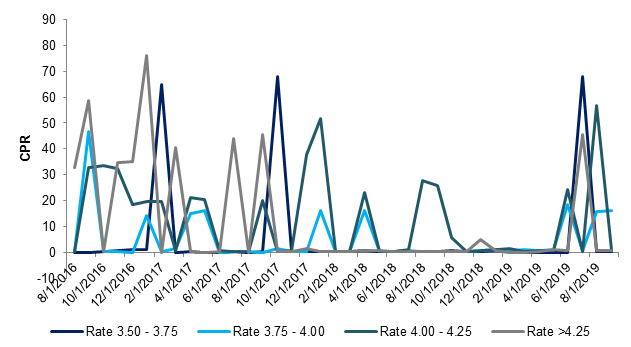

There may some attributes of the deal that makes it attractive relative to GSE CRT, however. Given the seasoning and low WAC, the pool should offer better convexity than newly issued GSE CRT bonds. Chase serviced loans with comparable WACs, seasoning and loan sizes have had choppy but by and large very slow prepayments. The level of prepay volatility is a function of a small sample of loans to observe (Exhibit 2).

Trying to bookend the compensation investors should receive for the additional credit and liquidity risk somewhat offset by the credit and convexity positives, the bonds would look attractive at 40-60 bp wider than comparable CRT risk with incremental spread compensation potentially being less at the top of the capital structure.

Exhibit 2: Prepay performance on lookalike loans

Source: Amherst Insight Labs, Amherst Pierpont Securities

A call on regulation

While regulators seem inclined to give capital relief, the transaction has a unique call feature that reduces transaction risk. The addition of the issuer call is in direct response to Chase’s ill-fated 2016 portfolio risk transfer deals, CHASE 2016-1 and 2016-2. In these deals, Chase deposited the loans to a trust, sold off a 0%-to-10% subordinate slice and retained the ‘AAA’ portion of the capital structure. They were the only deals backed by RMBS collateral to be issued under the FDIC Safe Harbor rule, which affords third-party investors similar protections as bankruptcy remoteness on secured financings where there is no true sale.

The stated goal of the ill-fated deals was to reduce the risk weighting on the retained interests from 50% to 20%, which is the risk weighting floor for structured products. In 2017, the OCC disallowed the regulatory capital treatment based on the fact that Chase controlled the loans as servicer and maintained significant economic interests in the transaction. The OCC’s conclusion may remind some of Hotel.com’s slogan, “Well thanks Captain Obvious” as the impetus for the Safe Harbor transaction was for Chase to retain the servicing and ‘AAA’ liabilities.

According to a recent Mayer Brown blog post, synthetic securitizations may provide a clearer path to risk-based capital relief. There are likely other tailwinds to a better outcome for Chase this time around. The recent Treasury plan for GSE reform made explicit mention of the use of portfolio risk transfer to level the playing field between banks and the GSEs. Additionally, changes at the top of the house at the OCC may look more favorably on the new deal as Joseph Otting, a Trump appointee has replaced Obama era comptroller Thomas Curry. Additionally, since the structure is fundamentally similar to those used by the GSEs and CRT has been widely held as a key to the overall de-risking of the GSEs, it would seem that a private institution engaging in a similar form or risk transfer should get the same credit.

And while the current deal is small, the 0%-to-8% slice on the reference pool representing just over a $60 million investment, it may prove to be the next little big thing. If the deal is blessed by bank regulators it likely paves the way for other institutions to be second and third movers, opening a new flow of residential mortgage credit for a broader audience of investors.