Uncategorized

LIBOR issues arise in legacy RMBS

admin | October 16, 2020

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors.

The first of likely a litany of issues around the end of LIBOR popped up in the RMBS market recently as US Bank as trustee on certain legacy deals went to court for advice on the pending termination of the index. The request for judicial intervention is not surprising and suggests the transition away from LIBOR in RMBS will likely be bumpy and contested.

The US Bank notice

On October 9, US Bank notified bondholders across 43 legacy trusts of its intent to get judicial instruction on a possible transition from LIBOR. Issues raised by the trustee include whether fallback provisions should apply to a temporary or permanent cessation of the index, how those terms should apply if LIBOR ceased to exist, what would constitute an appropriate replacement index and methods for selecting that index. These issues appear to be fairly pervasive throughout legacy RMBS.These 43 trusts likely only represent a small swath of trusts where similar issues will arise, which in turn, should lead to more actions of this kind.

The request for instruction ring fences 43 unique trusts and over 250 outstanding bonds, representing over $4.5 billion in notional balance across a host of structures and types of collateral including prime, subprime and option ARM profiles as well as manufactured housing. All the deals require 100% consent amongst the certificate holders to amend the documents.

An example of the language at issue comes from one of the US Bank trusts, LXS 2006-16N. After describing how the trustee will get the LIBOR offered rate from a Telerate page on a particular date, it states:

If any such offered rate is not published for such LIBOR Determination Date, LIBOR for such date will be the most recently published offered rate on the Designated Telerate Page. In the event that the BBA no longer sets such

offered rate, the Trustee will designate an alternative index that has performed, or that the Trustee expects to perform, in a manner substantially similar to the BBA’s offered rate. The Trustee will select a particular index as the alternative index only if it receives an opinion of counsel (furnished at the Trust Fund’s expense) that the selection of such index will not cause any of the REMICs to lose their classification as REMICs for federal income tax purposes.

The end to LIBOR will almost certainly come when the UK’s Financial Conduct Authority declares LIBOR unsuitable. In any event, after 2021, the FCA will no longer require banks to submit LIBOR setting and few banks will likely continue. The documents for LXS 2006-16N would likely hand responsibility for selecting an alternative index to the trustee, explaining why US Bank would want to go to a court now to get guidance on the kind of index that “has performed, or that the Trustee expects to perform, in a manner substantially similar to the BBA’s offered rate.”

For investors, the US Bank notice should raise the curtain on the risks posed by transitioning from LIBOR to an alternative index. That could have a range of effects on risk and valuation depending on the basis between LIBOR and the alternatives.

The risk of going from floating- to fixed-rate coupons

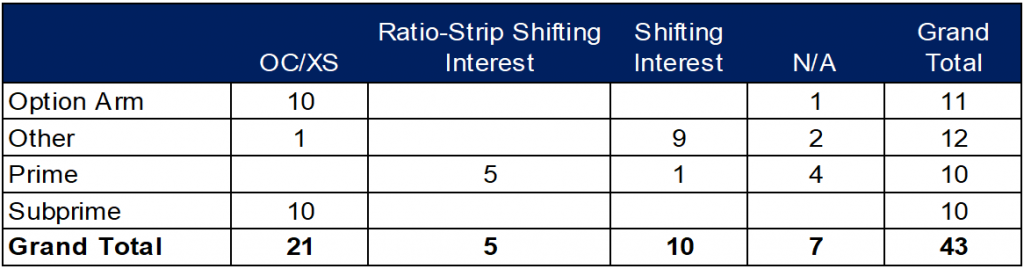

There are also trusts out there that do not turn to a trustee for an alternative index and instead leave it set at the last available reading on LIBOR. That would raise two issues that could be rife throughout the legacy market. First, investors in different parts of the capital structure will likely have conflicting interests, specifically around the issue of potentially permanently fixing the index to at the last observation of 1-month LIBOR. And secondly, investors’ potential desire or aversion to having LIBOR fixed may vary across excess spread structures as well as shifting interest ones across an array of different collateral profiles. (Exhibit 1)

Exhibit 1: LIBOR transition across varying legacy RMBS with USBank as trustee

Note: Structure and collateral in the USBank trusts.

Source: Amherst Insight Labs, APS

Ambiguous LIBOR fallback language could have meaningful impact on bond prices and durations across the capital structure. These issues could arise in any deal where floating-rate liabilities are issued even if the bonds are backed by fixed rate collateral. Fixing 1-month LIBOR at its last observed setting would cause floater durations to extend and their prices to fall as interest rates rise. Conversely inverse floaters or inverse IO issued opposite those floaters on backed by fixed rate collateral would benefit from their coupons being fixed at or near the bonds’ strike, assuming the level of 1-month LIBOR remains depressed at the final observation date.

Implications for excess spread structures may be even more pronounced in the instance where bond coupons are fixed at a final LIBOR observation. Under what appears to be a widely held assumption that servicers should have significant latitude to replace LIBOR in loans struck to the index, asset coupons could continue to rise while liability coupons remain fixed, generating more excess spread for these transactions. Bonds with leverage to excess spread would include both outstanding and potentially written-off mezzanine, subordinate and residual tranches of legacy RMBS as well as any derivatives with coupons determined by the amount of excess spread available to the trust.

Sizing up the impact

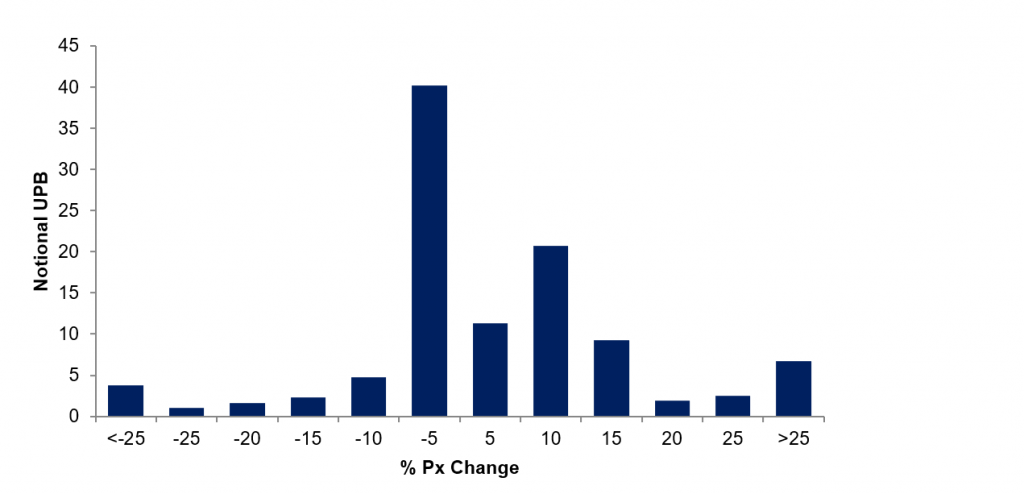

While fixing LIBOR at the last observed rate may be both contrary to the spirit of the deal documents and a low probability event, its impact, if it were to happen, could be material. And the probability of bonds being struck to a last LIBOR setting will likely not be the same given the incongruity around fallback language across the documents of given trusts. Using an admittedly crude assumption that all trusts are on relatively equal footing on this issue, an attempt can be made to approximate the impact to prices if bonds’ whose coupons are tied to 1-month LIBOR effectively converted from floating-rate to fixed-rate securities.

Using a fixed yield-to-price methodology, just over $40 billion in notional balance of legacy securities would see a market value decline between 5% and 10% relative to prices assuming that same yield as a result of simply holding forward 1-month LIBOR at a constant low, fixed rate going forward, the overwhelming majority of these being 1-month LIBOR floaters whose prices could decline even further assuming an increase in interest rates as these bonds effectively are converted to fixed rate securities. Conversely, it’s estimated that roughly $40 billion in notional legacy bonds could see prices rise by 10%. There is some asymmetry present in that assets with more upside to fixing the index are lower priced subordinate and derivative classes while bonds with downside are by and large higher priced, senior principal and interest bonds.

Exhibit 2: Estimating the price impact of fixing 1m LIBOR on the legacy universe

Source: Amherst Insight Labs, Amherst Pierpont Assumes all securities indexed to 1-month LIBOR’s coupons are fixed at spread over the index. Loans backing the trust with floating rate coupons increase along the forward curve in accordance with the index loans are tied to, including but not limited to CMT, COFI and 1-year LIBOR. Assumes ALIAS Pay Model Fair Value base case scenario and a 4% yield to price

Other considerations

An additional factor that will likely lead to other trustees following suit is the fact that, as can be seen in the prospectus language for the LXS 2006-16N deal, the trust bears any costs borne by the trustee associated with replacing the floating-rate index. Since potential costs arising as a result of petitions for judicial instruction will be borne by the bondholders, trustees can assumedly reduce their potential exposure at no cost to them, likely paving the way for other trustees to follow suit.

Finally, comparing the fallback language of the LXS covered trust to a comparable deal not named in the petition, LXS 2006-18N, shows that the relevant language is identical. As a result we can say with a reasonable degree of certainty that these 43 trusts are likely only a small representative sample of a far larger issue and one that may remain contested into next year and beyond.