By the Numbers

The market beats most managers through December

Steven Abrahams and Jinzhao Wang | January 8, 2021

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors.

The average CLO leveraged loan portfolio gained 3.10% between October and December but after adjusting for broad market exposure still trailed the market by 0.19%. More than 30% of larger CLO managers nevertheless managed to post wins. Prospects for fiscal stimulus and news of effective Covid-19 vaccines triggered a broad credit rally after US elections in November, and managers holding loan portfolios at the end of October with weaker credits and lower liquidity led the pack to close the year.

A strong 2020 finish for leveraged loans

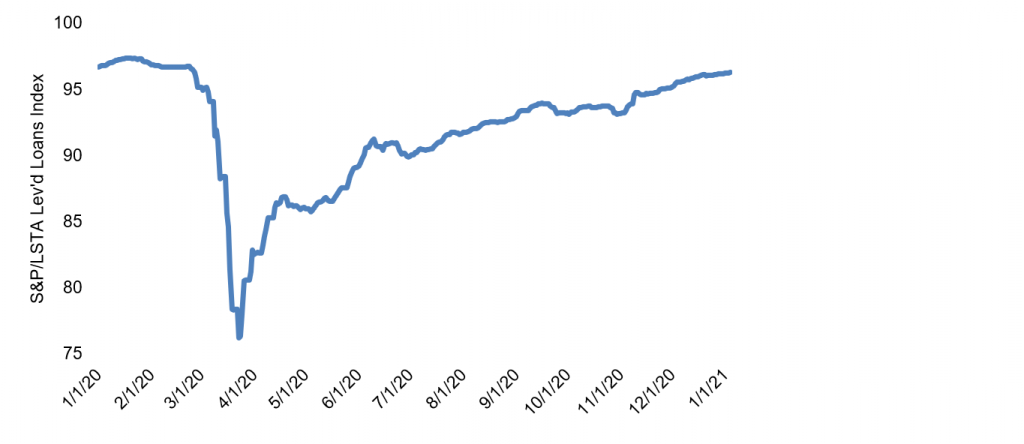

Loan prices rose steadily between October and December (Exhibit 1). The S&P/LSTA Leveraged Loan Index has now reached near its pre-coronavirus level. After accounting for the various reporting dates of managers, the index gained 3.17% between October and December. Managers held portfolios with an average broad market exposure, or beta, of 1.03, which meant the average manager should have gained 3.29%. With the actual average performance at 3.10%, the average manager underperformed the index by 0.19%.

Exhibit 1: Loan prices continued to rise through the end of 2020

Source: Bloomberg, Amherst Pierpont Securities

Portfolios of weaker credits outperformed

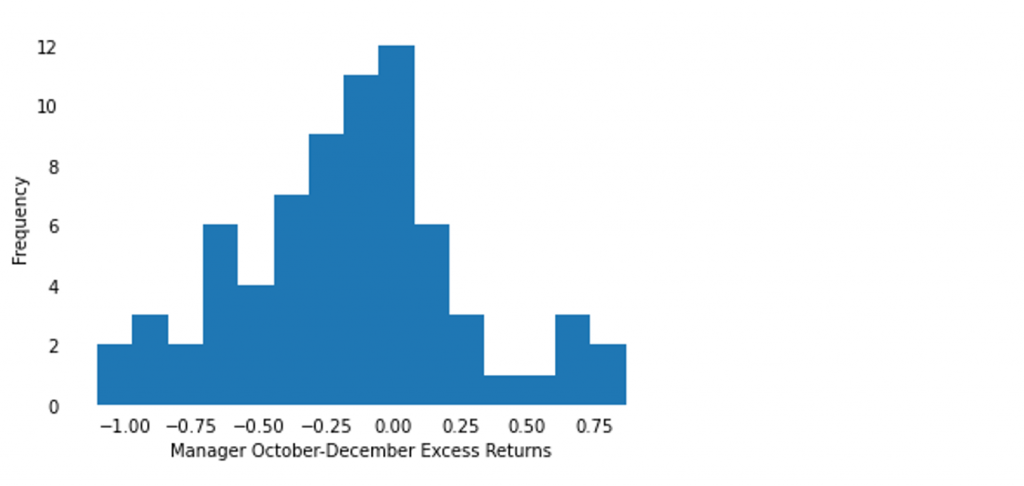

About 30% of managers with five or more active deals led the index, a downtick from the figures reported by Amherst Pierpont last month (Exhibit 2). Out of the 70 managers tracked for October through December, six delivered excess return or alpha greater than 50 bp, while 16 trailed the index by at least 50 bp.

Exhibit 2: Less than a third of the managers outperformed the index between October and December

Note: data shows excess return only for active deals.

Source: Amherst Pierpont Securities.

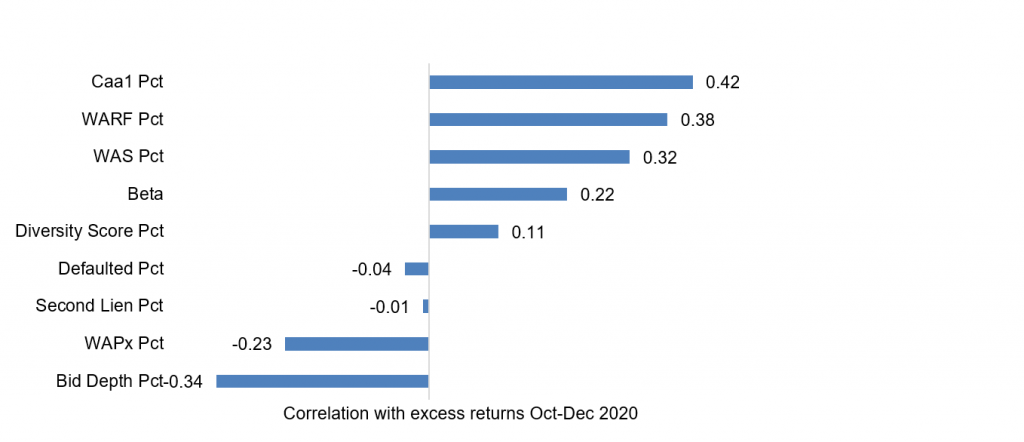

The weighted average rating factor and ‘Caa1’ exposure of the portfolio correlated most strongly with recent excess returns (Exhibit 3). Managers who held portfolios with a higher weighted average rating factor or more exposure to loans rated ‘Caa1’ or below delivered higher returns. Additionally, portfolios with a lower bid depth or lower weighted average price also correlated with more recent excess returns. These relationships indicate that managers holding riskier loans continued to outperform between October and December.

Exhibit 3: Correlation of portfolio or manager features with recent excess return

Note: data shows the correlation of manager or loan portfolio attribute with managers’ excess return or alpha from October through December only on active deals. Portfolio attributes measured as percentiles.

Source: Amherst Pierpont Securities.

Meanwhile, the exposure to defaulted and second-lien loans correlated weakly and negatively with recent excess returns. While riskier collateral mostly led to better performance for managers, as the loan market rallied between October and December, some collateral may still carry fundamental risks that continued to put a drag on performance.

The alpha leaders

The following managers delivered positive alpha in the market between October and December (Exhibit 5). Angelo Gordon, Jefferies and Denali top the chart this time. The other alpha leaders in the Top 10 include Marathon, ZAIS, KKR, Symphony, DFG, Apollo and ArrowMark.

Exhibit 4: Alpha leaders in CLO portfolio performance October-December 2020

Note: Performance for managers with five or more deals tracked by APS. Performance attribution starts with calculated total return on the leveraged loan portfolio held in each CLO for the 3-month reporting period ending on the indicated date. CLOs, even with a single manager platform, may vary in reporting period. The analysis matches performance in each period to performance over the identical period in the S&P/LSTA Leveraged Loan Index. Where a deal has at least 18 months of performance history since pricing and no apparent errors in cash flow data, the analysis calculates a deal beta. The deal beta is multiplied by the index return to predict deal return attributable to broad market performance. Where no beta can be calculated, the analysis uses the average beta across each manager’s active deals weighted by the average deal principal balance over time. Any difference between performance attributable to beta and actual performance is attributed to manager alpha.

Source: Amherst Pierpont Securities.