Uncategorized

The swift prepayment speeds in Freddie Mac K-Series floating-rate loans

admin | April 9, 2021

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors.

The rising issuance of Freddie Mac floating-rate CMBS backed by floating-rate loans has revived interest in prepayment speeds. In short, they are much faster than speeds in fixed-rate loans and likely leave the average life of the floating-rate CMBS much shorter. This should be welcome news for banks on the hunt for assets with low duration and steady cash flow liquidity.

The basics of prepayment speeds in floating-rate K-Series loans are straightforward:

- After a 1-year lockout period, the floating rate loans are prepayable with a 1% penalty. The prepayment penalty goes to Freddie, not to the investors

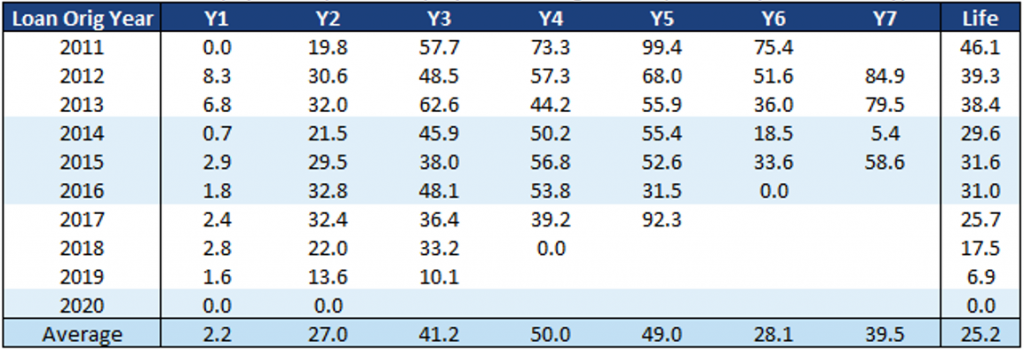

- Prepayment speeds begin to rise immediately after expiration of the lockout, hitting 27 CPR on average two years after origination and rising to 40 CPR and then 50 CPR in years three and four (Exhibit 1)

- Involuntary prepayments do happen but have been relatively rare in Freddie K floaters since a cluster of defaults from the 2012 vintage (which occurred in 2019)

Exhibit 1: FHMS K-F Floater: Prepayment speed ramp by loan vintage – CPR (voluntary and involuntary)

Source: Intex, Amherst Pierpont Securities

- The average life of a new floater at 0 CPY is 9.4 years. This can be seen by running the SOFR floater, the FHMS K-104 AS, issued in March 2021 in Bloomberg’s SYT screen. However, running it at a steady 25 CPR, which is the lifetime average prepayment speed for K-Series floaters shown in the table, the average life drops to 3.9 years. Running the historical prepay vector of speeds shown in the last row of the table above reduces the projected average life to 3.6 years. Even at 50% of the historical speed vector, the average life drops to 5.3 years.

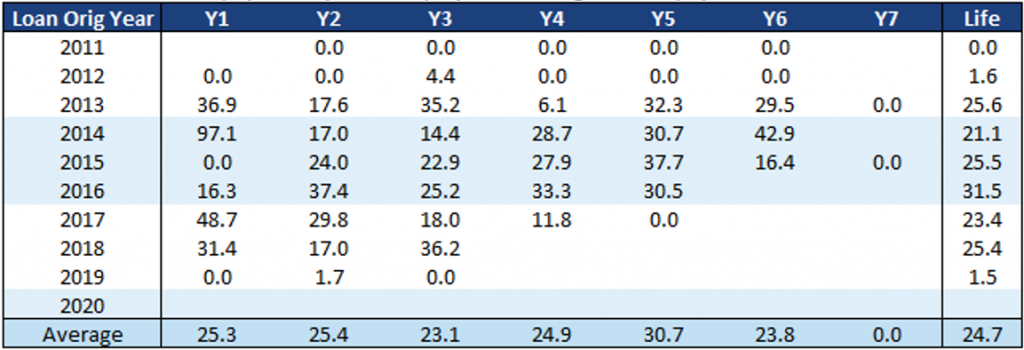

- The 1% prepayment penalty can be waived if the borrower refinances into a Freddie Mac fixed-rate loan. On average 25% of floating rate K loans that prepay over time have their prepayment premium waived (Exhibit 2).

Exhibit 2: FHMS K-F Floater: Prepayment speed ramp by loan vintage – % prepayment premiums waived

Source: Intex, Amherst Pierpont Securities

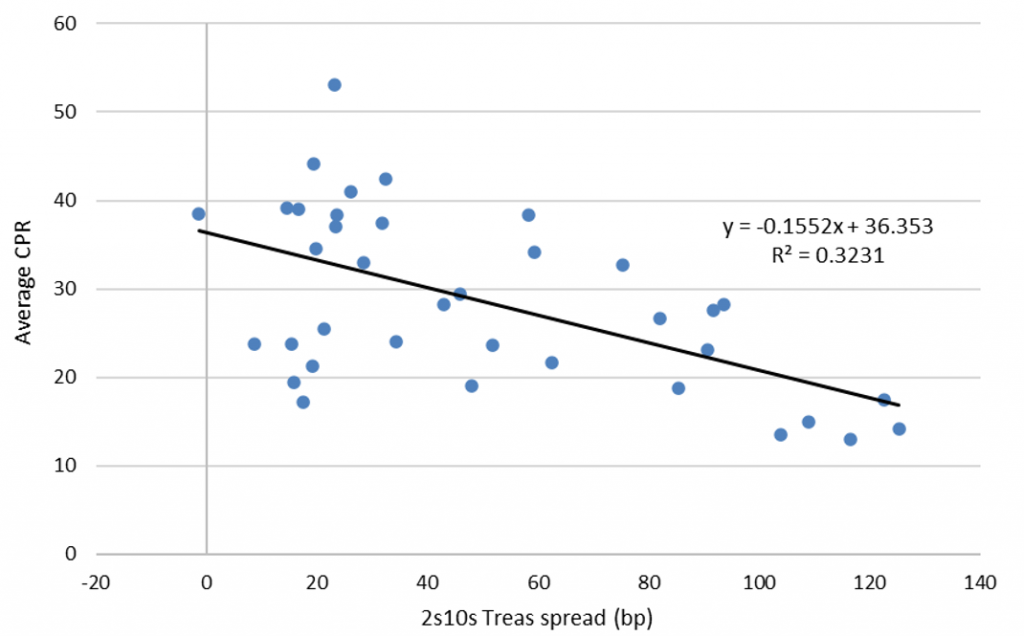

- Generally speaking, prepayment in floating-rate loans tend to slow down when the curve steepens and accelerate as the curve flattens. The chart below is a scatterplot of monthly average CPR of Freddie’s floating rate loans against the 2s10s Treasury slope at the beginning of the month (Exhibit 3). It does not account for burnout of many loans or the time it takes to refinance, which is longer than a couple of weeks, but it does illustrate the point that refis of floating-rate loans are sensitive to curve shape – as fixed rates approach the floating rate, borrowers tend to refinance more quickly. A steep curve slows down prepayment rates of floaters.

Exhibit 3

Source: Amherst Pierpont Securities

The average life of the K-Series floating rate debt is a key part of current relative value. Comparing a K-Series AS class to a K-Series fixed-rate A2 class with a 10-year weighted average life requires weighing a current AS coupon of 26.1 bp to an A2 swapped to floating of 29 bp. The AS has a floor on the coupon and less operational and accounting complexity. The shorter average life adds to the appeal of the AS, making the relative value case for the K-Series SOFR floaters stronger.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2024 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.