Uncategorized

High DTI homeowners get some refi help from Fannie Mae, Freddie Mac

admin | April 30, 2021

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors.

Lower income homeowners with debt-to-income ratios above 50% should have an easier time refinancing their mortgages with introduction of new refi programs by Fannie Mae, Freddie Mac and their regulator. Although only 2.7% of 30-year GSE loans since 2014 have had an original DTI of 50% or greater, the pandemic may have raised that share. Parts of the specified pool market and loans coming out of forbearance could see some impact.

Many of these borrowers would have qualified for the GSEs’ existing lower income refinance programs except for their DTI ratios. The new RefiNow program announced April 28 by Fannie Mae and Refi Possible announced by Freddie Mac will accept borrowers with DTI ratios up to 65%. The existing programs—Fannie Mae’s HomeReady and Freddie Mac’s Home Possible—generally cap borrower DTI at 45% and the GSEs’ standard refinance programs do not exceed 50% DTI. Borrowers with DTI at or below 45% will probably prefer a HomeReady or Home Possible refinance, which generally will have lower upfront fees.

The greatest risk to MBS investors from faster prepayment speeds may come from the FHFA’s intention to aggressively market the new programs, which could trigger refinances from borrowers eligible for existing refinance programs. Loans that went into Covid-19 forbearance may also be able to take advantage, assuming forbearance followed enough loss of homeowner income to raise DTI above existing program limits. It is not yet clear, however, whether borrowers coming out of forbearance would need to meet the pay history requirements of the new programs. Fannie Mae and Freddie Mac have yet to release detailed guidelines.

The RefiNow and Refi Possible programs can be compared to the existing HomeReady and Home Possible programs since both are only available to borrowers making at most 80% of the area median income. Borrowers eligible for both programs are likely to prefer HomeReady and Home Possible. One benefit of the new programs—waiving the 50 bp adverse market refinance fee for loans less than or equal to $300,000—is already offered to all HomeReady and Home Possible mortgages regardless of balance. The new programs offer $500 credits towards appraisal fees, but that only benefits borrowers that do not receive appraisal waivers. And many upfront fees that are capped or waived under HomeReady and Home Possible will be charged to borrowers using the new programs

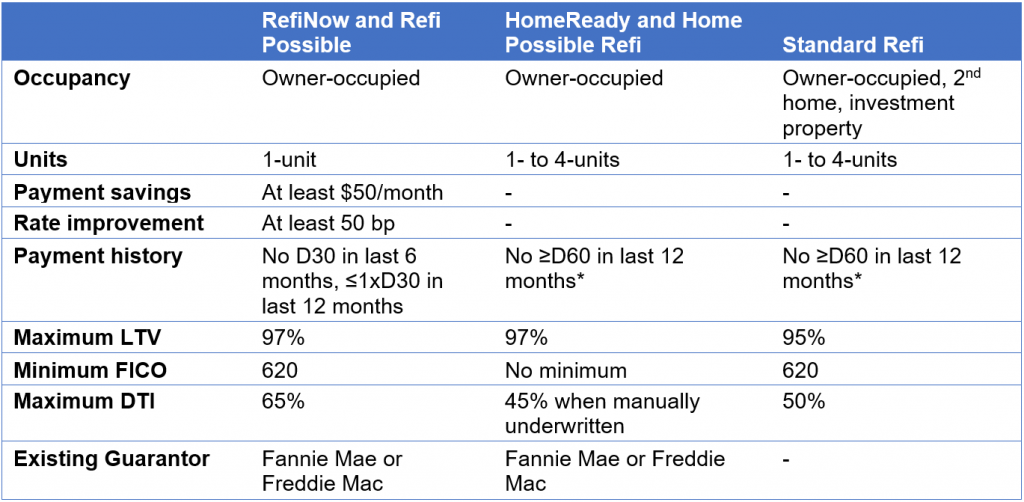

Other than the increased debt-to-income limit, eligibility for RefiNow and Refi Possible are more restrictive than HomeReady/Home Possible and standard refinances. The below table gives a brief overview of the eligibility differences between the refinance programs:

Note: * Loans are able to refinance after making 3 consecutive payments following Covid forbearance.

Source: Amherst Pierpont Securities.

The primary benefit of today’s announcement is to expand refinance eligibility to borrowers that have suffered income loss and could not refinance using existing programs. It also makes refinancing a little cheaper for 45 to 50 DTI borrowers that would have been able to use a standard refinance, but the modest benefits and restriction to lower income borrowers make it unclear whether the program triggers a big increase in prepayment speeds.

The bigger risk to MBS investors may come from efforts to market the program to eligible borrowers. Outreach efforts are likely to reach borrowers that do not need these new programs to refinance since the GSEs and lenders may have limited information on borrower’s current incomes. These borrowers may have lower DTIs and/or higher incomes and not be eligible for the new programs, but find out they can save money refinancing through an existing program.

The program is expected to be made available this summer. Fannie Mae and Freddie Mac plan to release more information about the programs soon, which could alter the view of these programs.

The relevant announcements are here:

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2024 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.