By the Numbers

Expect heavy net supply from strong home sales

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors.

The net supply of agency MBS moved higher in the fall, buoyed by a pickup in existing home sales. Falling new home sales prevented an even larger increase. Net supply could average $60 billion a month in 2022 if home sales remain at the current pace. This will quickly become a challenge for markets to absorb as the Fed plans to stop growing its MBS portfolio by mid-March. And private investors may have to deal with even greater supply later in the year if the Fed stops reinvesting some of its MBS paydowns. Mortgage spreads are likely to keep widening unless home sales slow markedly or weakness in corporate earnings pushes money managers to reallocate into MBS.

The pace of home sales is a large driver of new supply in agency MBS. Existing and new home sales jumped during the pandemic, reaching the highest levels since early 2007. Both indices peaked in early 2021 but fell sharply in the spring and summer. Existing home sales rebounded close to the peak levels in the fall, but new home sales remain lower and was even revised lower in July and August. A shortage of new homes is the likely reason that new home sales did not keep pace with existing home sales

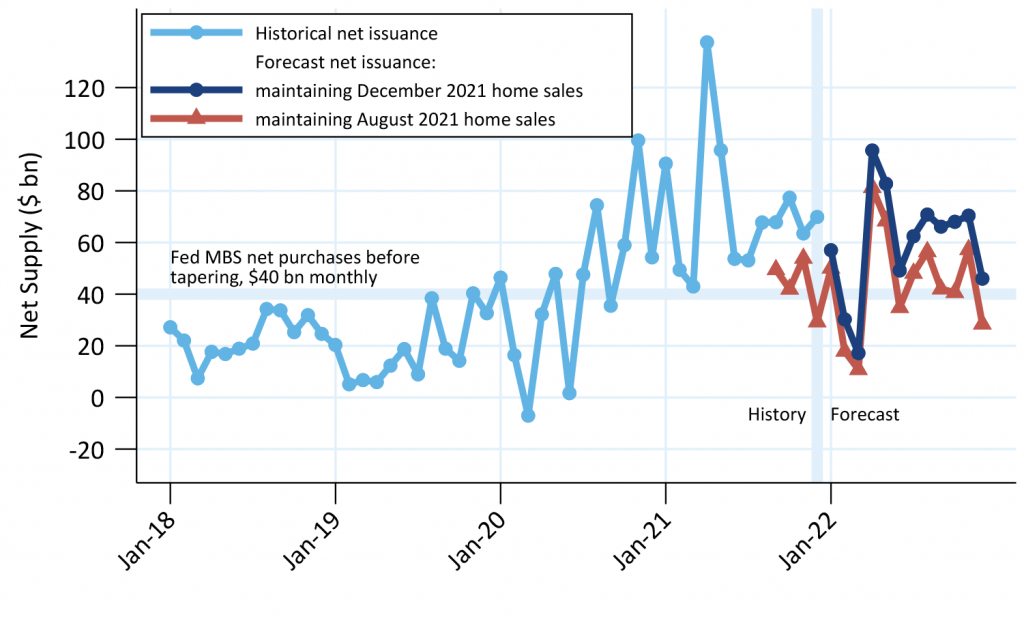

Amherst Pierpont’s net supply model predicts that net supply will average roughly $60 billion a month in 2022 (Exhibit 1). This is higher than the prior forecast of $45 billion a month, which used August home sales data. The increase is driven by the pickup in existing home sales, which caused the model to underpredict supply over the last few months. New home sales haven’t bounced back to the levels from early 2021, but the November reading is close to the level used for the August forecast.

Exhibit 1. MBS supply could average roughly $60 billion each month

The December forecast assumes 6.18 million existing home sales and 744,000 new home sales. The latter is slightly below Amherst Pierpont’s estimate of 750,000 and the median estimate of 770,000. The August forecast assumes 5.88 million existing home sales and 740,000 new home sales.

Source: Bloomberg, Amherst Pierpont Securities

Home sales are not the only factor that could affect MBS supply in 2022. The higher conforming loan limit should divert into agency pools more origination that previously would have been held in bank portfolios or sold into private-label securitizations. But Fannie Mae and Freddie Mac are raising fees on certain loans, which could push some production back to portfolios or private securitizations. And higher mortgage rates make housing less affordable, which might slow home sales.

The Fed plans to stop growing its MBS portfolio by mid-March, which means that all this net supply will end up with private investors. This should pressure mortgage spreads to continue to widen. And it appears the Fed is considering allowing the MBS portfolio to runoff starting later in the year, which would further boost the supply of MBS flowing to private investors and another negative for the basis. Coupled with the heavy supply from strong home sales makes spread widening likely. However, any weakness in corporate credit could boost demand from money managers and help limit the widening.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2024 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.