The Big Idea

Concern continues around S&P insurer ratings

Steven Abrahams, Caroline Chen and Min Wang | March 18, 2022

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors.

S&P’s proposed changes to its analysis of insurance company capital continues to draw fire from insurers and others concerned that it penalizes investments without an S&P rating. The proposal would raise capital requirements for an estimated $120 billion of current insurer holdings in structured finance alone, with a sharply higher burden on $20 billion of those holdings that lack a rating from any the three largest agencies. These results come from analyzing $204 billion of structured finance holdings across 550 insurers. The potential impact varies significantly across assets and insurers. S&P continues to take input, but some issuers have pulled deals from agencies most penalized by the new approach and some investors will not buy deals only rated by those agencies. Industry groups plan to file comments, and some members of Congress have suggested hearings. The outcome of S&P’s proposal may not be clear until late this year.

A capital penalty for assets without an S&P rating

S&P last December proposed sweeping revisions to its analysis of insurance company capital (Request For Comment: Insurer Risk-Based Capital Adequacy—Methodology And Assumptions, December 6, 2021). The rating agency has always compared current capital to the amount needed in a series of stress scenarios. Capital feeds into a broad framework for rating the insurer that includes industry and competition, business risk and funding and so on. The rating reflects an insurer’s ability to meet its obligations, including paying claims to policyholders. While state insurance commissioners have their own rules for assessing insurer capital and set industry requirements, S&P ratings affect the insurer’s ability to price and market its insurance.

The rating agency currently uses 10 separate guides to assess capital worldwide across life, property and casualty, health, mortgage, trade credit, title and reinsurance. It applies those guides to 350 different insurers, according to Carmi Margalit, one of the authors of the S&P proposal. The proposed approach would replace the separate guides, Margalit emphasized the agency is aiming for a consistent, transparent and more usable approach.

While the proposal focuses on all aspects of an insurance company that influence capital—current capital, asset credit risk, interest rate and other market risks across assets and liabilities, risks of loss in different lines of business, the impact of diversification and so on—the provisions for setting capital on bonds and loans has drawn sharp fire. Any asset without an S&P rating, in the proposed approach, gets penalized. Specific adjustments apply to assets rated by Moody’s or Fitch:

- For corporate and government ratings, S&P lowers a Moody’s or Fitch investment grade rating by one notch and a speculative grade rating by two notches; for instruments rated by both, S&P uses the lowest notched rating

- For structured finance, S&P lowers the rating in general by three notches; if rated by both, S&P may lower the lowest rating by two notches

Some of the heaviest fire has targeted the S&P proposal for bonds and loans without a rating from S&P, Moody’s or Fitch. That would include assets rated by Kroll Bond Rating Agency, DBRS Morningstar, Egan-Jones or others. The S&P proposal keeps the door open to mapping S&P ratings to these other agencies, but S&P has not done the mapping so far. If S&P proves unable to map these providers, the asset is treated as ‘CCC.’

The impact of notched ratings or getting classified as ‘CCC’ becomes clear in the proposed capital charges for credit risk. S&P sets required capital based on product, rating, maturity and stress scenario. Products fall into four categories:

- Category 1: Sovereign, municipal, GSE, senior secured, infrastructure and project finance and covered bond debt

- Category 2: Senior unsecured debt

- Category 3: Subordinated debt, and

- Category 4: Structured finance

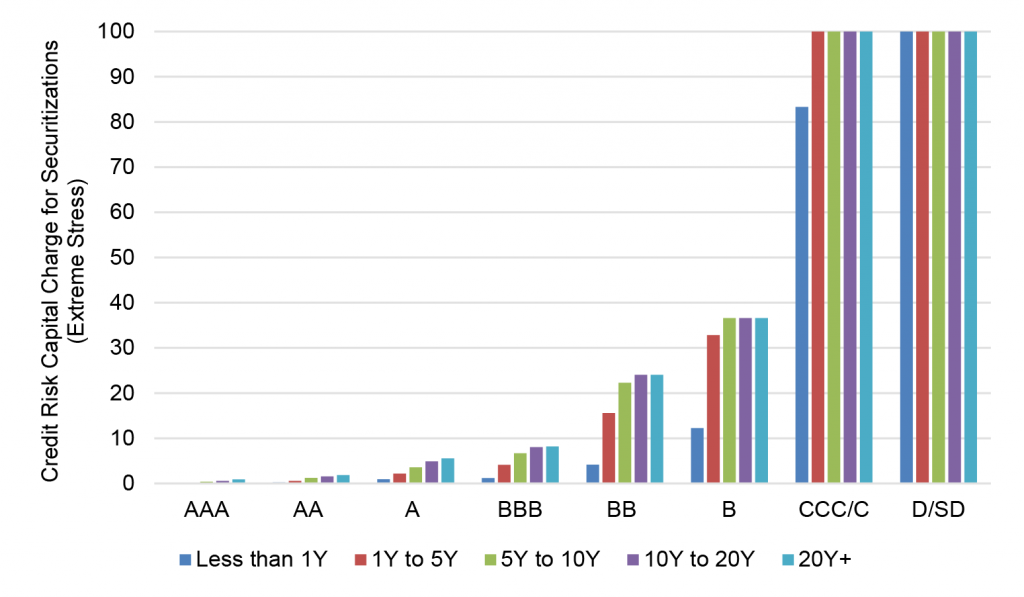

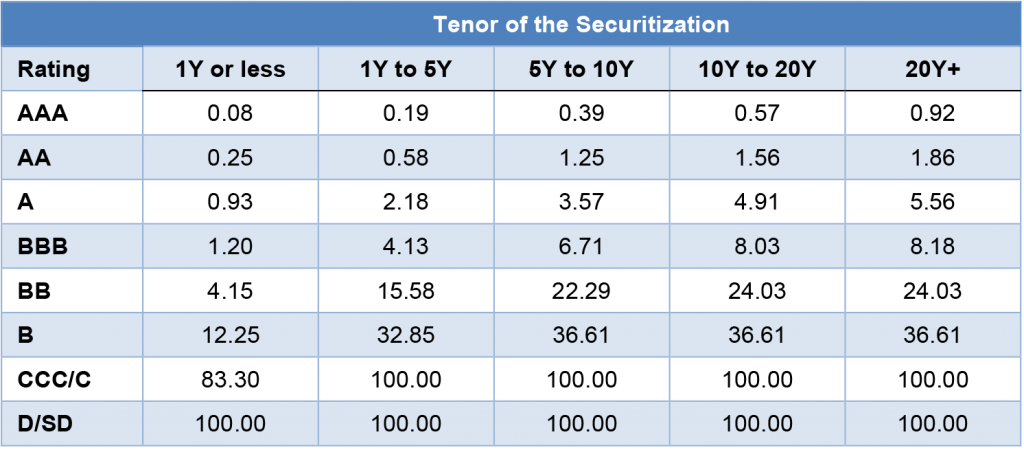

Structured finance has attracted the most attention because S&P has a smaller footprint in that category, raising the likelihood of an insurer holding instruments without an S&P rating. In S&P’s extreme stress scenario, which S&P sees as a 1-in-10,000 event and which sets capital consistent with the highest rating for an insurer, the S&P proposal has a meaningful effect on required capital. For example:

- Capital required for an S&P ‘AAA’ ranges from 0.08% of par for a 1-year or shorter instrument to 0.92% for a 20-year or longer (Exhibit 1)

- For a Moody’s or Fitch ‘AAA’ where the rating would drop by three notches to ‘AA-“, required capital goes up to 0.25% for a 1-year or shorter instrument, more than three times the S&P ‘AAA’, and to 1.86% for 20-year or longer, more than two times the S&P ‘AAA’

- For a Kroll, DBRS Morningstar, Egan-Jones or other ‘AAA’ where S&P does not have a rating map and where the rating would drop to ‘CCC’, required capital goes up to 83.30% for a 1-year or shorter instrument, more than 1,041 times the S&P ‘AAA’, and to 100% for a 20-year or longer, more than 1,250 times the S&P ‘AAA’.

For an insurer with a substantial share of its asset base in instruments without an S&P rating—and especially in instruments without S&P, Moody’s or Fitch—the added capital requirement could either threaten the company’s current rating or require restructuring the asset mix or other parts of the balance sheet to protect the rating. Or the holder may have to raise capital.

For individual assets or categories of assets effected by S&P’s proposed approach, the higher capital requirements could affect primary and secondary pricing. And if insurers choose to sell holdings without an S&P rating, it could have an impact on secondary prices in asset sectors where S&P has a light presence and where selling might be concentrated.

Exhibit 1: Proposed S&P extreme stress capital charges for structured finance (% of asset par balance)

Note: exhibit shows capital charge in the extreme stress scenario (99.99%).

Source: S&P Global, Request for Comment: Insurer Risk-Based Capital Adequacy—Methodology And Assumptions, Table 6, December 8, 2021, Amherst Pierpont Securities.

The potential impact of the S&P approach on assets and insurers

S&P estimates in its proposal that the full set of changes could lead to actions on up to 10% of insurance ratings with the majority changing by one notch and with more upgrades than downgrades. On S&P assessment of capital, however, it estimates changes for up to 35% of insurers. Changes in capital assessment, the agency says, could affect up to 20% of credit profiles before weighing possible benefits from diversification and other forms of support.

S&P has not disclosed estimates of impact on specific asset categories or on specific insurers, and S&P’s Margalit did not say he had seen any estimates at these levels either. That could make it difficult for anyone outside of S&P to independently gauge impact of the proposed changes.

Amherst Pierpont took regulatory filings for 550 insurers as of September 30, 2021 and focused on holdings in structured finance. The analysis calculated a few measures of exposure to S&P’s proposed approach:

- The percentage of holdings with an S&P rating

- The percentage with no S&P rating but at least one from Moody’s or Fitch

- The percentage with no rating from S&P, Moody’s or Fitch

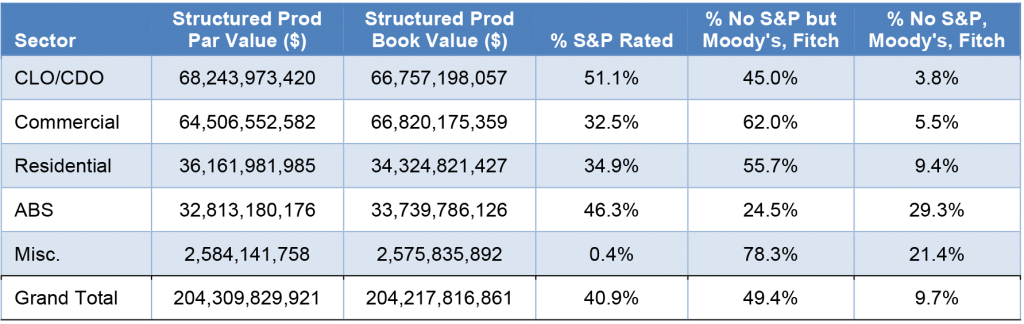

The analysis shows nearly 41% of insurer structured products with an S&P rating, meaning more than 59% would be subject to some form of capital penalty under the S&P approach (Exhibit 2). That would increase capital on more than $120 billion in assets. The S&P presence varies significantly across products. Less than 33% of commercial real estate exposures have an S&P rating, for example, while more than 51% of CLOs and CLOs have an S&P grade.

More than 49% of insurer structured products have no S&P rating but one from Moody’s or Fitch. This amounts to nearly $100 billion in assets. This also varies significantly across products. Less than 25% of ABS fall in this category while more than 62% of CMBS do. Ratings on these exposures would drop by three notches.

Less than 10% of insurer structured products lack a rating from S&P, Moody’s and Fitch. This amounts to $20 billion in assets. These is significant variation again across products. Less than 4% of CLOs and CDOs fall in this category, for instance, while more than 29% of ABS do. These exposures could get treated as ‘CCC’ and see required capital go up dramatically depending on current rating.

Exhibit 2: Insurer exposure by sector to proposed S&P approach to securitizations

Note: Data for insurer holdings of CLOs and CDOs, CMBS, RMBS, ABS and miscellaneous structured products as of 9/30/2021 based on regulatory filings. Analysis focuses only on entities categorized by IPREO as insurance companies. Some insurers that report at asset managers may not appear.

Source: IPREO, Intex, Bloomberg, Amherst Pierpont Securities.

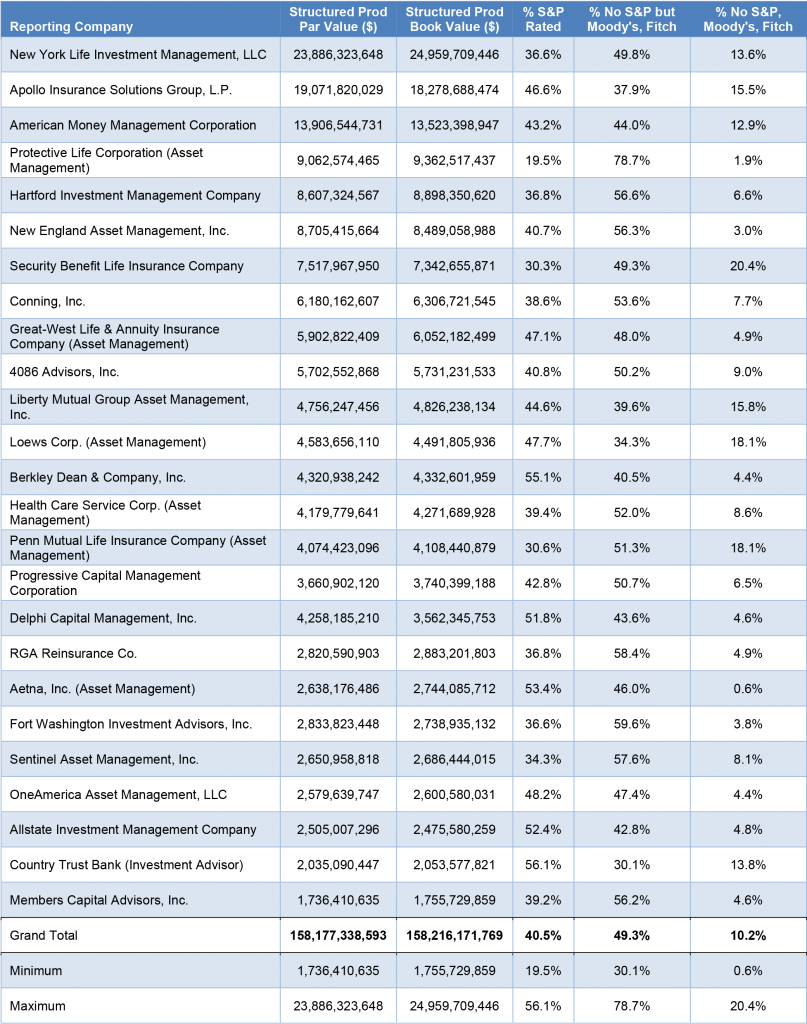

Insurers also showed significantly different exposures to the S&P approach. Readers can filter, sort and select from a complete list of 550 insurers here. Among insurer portfolios with the 25 largest holdings in structured products, the average has almost 41% with an S&P rating, but that ranges from nearly 20% to more than 56% (Exhibit 3). Insurers with these large exposures also have an average of more than 49% without S&P but with either Moody’s or Fitch, although that exposure ranges from more than 30% to more than 79%. These insurers also have an average of more than 10% of structure finance exposures with no rating from either S&P, Moody’s or Fitch and subject to classification as ‘CCC’, and that ranges from less than 1% to more than 20%.

Exhibit 3: Insurer exposure by company to proposed S&P approach to securitizations

Note: Data for insurer holdings of CLOs and CDOs, CMBS, RMBS, ABS and miscellaneous structured products as of 9/30/2021 based on regulatory filings. Analysis focuses only on entities categorized by IPREO as insurance companies. Some insurers that report at asset managers may not appear.

Source: IPREO, Intex, Bloomberg, Amherst Pierpont Securities.

These exposures are only one part of each insurer’s balance sheet, of course, so the impact on capital and company ratings is hard to pinpoint. However, with S&P poised to view around 10% of this exposure as ‘CCC’, it is hard to imagine it will not raise capital requirements significantly on this part of the balance sheet.

No mapping so far beyond Moody’s and Fitch

Given the dramatic capital impact of treating an asset as ‘CCC’, the lack of mapping beyond Moody’s and Fitch has also drawn attention. S&P first mapped just to Moody’s and later mapped to Fitch, according to Margalit. “We’d like to map to other rating agencies.”

Caitlin Colvin, Managing Director at Kroll, said S&P had not contacted Kroll for any information needed for mapping. Charles Lucas, a vice president at DBRS Morningstar, also said S&P, to his knowledge, had not been in touch. Margalit, who said a group at S&P outside of insurance company ratings did all mappings, did not know if S&P had approached other rating agencies.

S&P describes its approaching to mapping other ratings scales in a 2014 piece (Mapping A Third Party’s Internal Credit Scoring System to S&P Global Ratings’ Global Rating Scale, May 8, 2014). S&P looks for instances where S&P and the other rating agency have both rated an issuer or a security. For every instance where the other agency has rated an instrument ‘AAA’, for example, S&P will look at its own rating and calculate a difference. If S&P rated the instrument ‘AA+’, the difference might be ‘-1’. Over multiple pairings, S&P will end up with a distribution of differences, and the distribution will have an average and a standard deviation. S&P translates this distribution into expected 5-year default rates. Instead of mapping to the average or the expected default rate for the other rating agency, S&P adjusts the mapped default rate higher:

In this equation, S&P chooses t so that in a hypothetical repetition of the analysis an infinite number of times, the average default rate would fall below the adjusted default rate 95% of the time. That value is 1.645. The bigger the standard deviation of differences or the smaller the number of pairs, then the higher the adjustment. S&P could plausibly argue that deals bypassing the agency and going to another provider could have a systematic bias toward higher risk and need an extra margin of safely. This is likely the reason S&P chooses to notch ratings by Moody’s and Fitch.

It is unclear why S&P could not apply this same approach to Kroll, DBRS Morningstar, Egan-Jones or other rating agencies. The S&P approach notes that it needs a representative sample of pairings to map well but also notes “In general, we would expect a minimum of at least 10 observations.”

“There’s no hard line in terms of minimum number of observations,” Margalit noted, suggesting S&P may have adjusted its mapping approach since 2014. He also said the agency could not disclose the number of observations used to map Moody’s or Fitch.

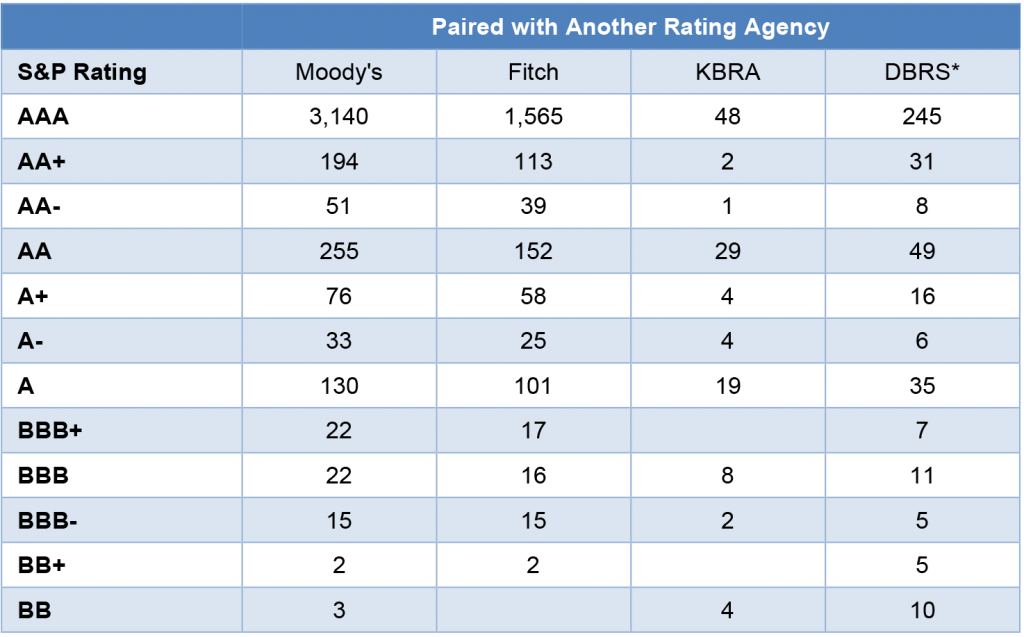

Focusing only on the residential structured finance exposures disclosed by insurers through September 30 last year, it is clear that Moody’s and Fitch overlap with S&P much more than Kroll or DBRS (Exhibit 4). But the overlap with Kroll and DBRS also seems to exceed at least the minimum mentioned in S&P’s 2014 methodology. For example, insurers reported 3,140 unique residential securities rated by S&P as ‘AAA’ that also had a rating by Moody’s. Insurers also reported 1,565 securities rated by S&P as ‘AAA’ that also had a rating by Fitch. But insurers only reported 48 securities rated by S&P as ‘AAA’ that also had a Kroll rating and 245 that also had a DBRS rating. The number of pairs would almost undoubtedly grow in an analysis that looked at a longer history of insurer holdings.

Exhibit 4: Number of pairings of S&P rating with other agencies’ in residential securities reported by insurance companies as of September 30, 2021

Note: data shows counts of unique non-government residential securities disclosed by insurers on September 30, 2021, where the security had an S&P rating and a rating by Moody’s, Fitch, KBRA or DBRS. DBRS data are before its merger with Morningstar. Analysis based on original ratings. Analysis focuses only on entities categorized by IPREO as insurance companies. Some insurers that report at asset managers may not appear.

Source: IPREO, Intex, Bloomberg, Amherst Pierpont Securities.

S&P notes in its mapping analysis that it may consider other factors, such as the time window for observing rating pairs, to ensure the mapping relationship is stable. The shorter histories for Kroll, DBRS and other agencies may work against them in the S&P approach.

If S&P is unable to map to Kroll, DBRS or others, Margalit did emphasize that the proposal would allow the rating committee to take an asset categorized as ‘CCC’ and adjust it up or down by one category if the insurer could justify it. That would take ‘CCC’ exposures up to ‘B’. That would lower the capital requirement but still leave it well above levels for investment grade assets.

It is worth noting that S&P’s current analysis of insurer capital uses the asset’s rating from the National Association of Insurance Commissioners whenever the asset lacks an S&P rating. “It is close enough to proxy the S&P rating,” Margalit notes. But the NAIC only scores US insurers, and S&P is proposing to drop the NAIC proxy for an approach that would work worldwide.

The NAIC has declined to comment on the S&P proposal. “Rating agencies are independent commercial enterprises responsible for their own methodologies,” said Charles Therriault, director of the NAIC’s securities valuation office, in an email to Amherst Pierpont. “The NAIC staff does not comment on their methodologies.”

Already having an impact on the ratings industry

The S&P proposal has already had an impact on the ratings industry. Kroll’s has had at least seven ratings processes put on hold since the S&P announcement by issuers concerned about going to market without a major agency rating, according to Kroll’s Colvin. At DBRS Morningstar, no issuers have explicitly pulled the plug on ratings, according to Lucas. Some bankers report that issuers are now going to S&P that might have used only Kroll in the past.

Both Kroll and DBRS Morningstar have had inquiries from insurers interested in comparing their ratings to those of S&P, Moody’s and Fitch. Colvin says she has been on more than 40 calls on the issue.

Some investors also have reportedly stopped buying assets that might be affected by the proposed S&P approach. Colvin says dealers have told her of at least nine insurers that will not buy outstanding securities with a rating only by Kroll. Amherst Pierpont also is aware of insurers that have stopped buying assets that might go to ‘CCC’ under the S&P guidelines.

Morningstar provided information to the Structured Finance Association and the American Council of Life Insurers, who reportedly plan to file comments on the proposal with S&P.

Rep. Brad Sherman (D-CA), who chairs a subcommittee on investors and capital markets under the House Financial Services Committee, recently told POLITICO he planned to hold hearings on S&P’s “power grab.

“Capitalism doesn’t work when you have this kind of an unrivaled power,” Sherman said. “This by itself will get half or more of the insurance companies to blackball those bond issuers not rated by the Big Three.”

An email from Amherst Pierpont to Sherman’s office trying to confirm if hearing will take place is still unanswered at press time. And Jeff Sexton, head of communications for S&P in the Americas, says the agency is not aware of any hearings being scheduled to discuss the S&P proposal.

Next steps for S&P

S&P originally planned to close its comment period on February 18. It then extended the period to March 18 and recently extended it again to April 29. After the comment period ends, according to S&P’s Margalit, the agency will review comments, make any changes to its approach if warranted and then publish a final document along with all comments submitted to the agency. The agency will also publish a list of insurers whose ratings might change in light of the final methods. The agency will then review ratings on an expected 350 companies worldwide, which Margalit expects could take up to six months after the agency publishes final rules.

“This is not an established method,” Margalit emphasizes. “It is a proposal, and we are eliciting feedback.” Margalit said S&P cannot disclose whether it has received feedback until it publishes its final approach. “There have been no decisions yet, and there will be none until discussions are final.”

Reactions from insurers

“The S&P approach would clearly be a negative for the market,” said one insurance company portfolio manager. “We are hoping there is enough momentum during the comment period to change the proposal.”

Outright selling of securities by insurers could be easier said than done, another insurance portfolio manager suggested. Taxes and the loss of book yield could be clear obstacles to sales. Another manager expects “a slowdown in new acquisitions of non-major rated bonds.”

“It’s unclear where we’ll end up,” another manager said. “No one seems to be in favor. But the same manager noted that the overall set of changes to analyzing capital could leave many insurers in better shape. Changes in the handling of asset and liability duration and other offsets could be more balance sheet friendly.