By the Numbers

KBRA pushes back on S&P’s proposal for insurer ratings

Caroline Chen | April 22, 2022

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors.

KBRA has started to push back against an S&P proposal that would likely hurt smaller rating agencies and affect the ability of insurance companies to invest in certain fixed income products. S&P’s proposed approach to insurer financial strength would penalize securities without an S&P rating by raising the amount of capital needed to hold the investment. KBRA argues that its ratings deserve much more favorable capital treatment than the one proposed by S&P, although it is unclear whether S&P will be swayed.

KBRA on April 18 issued a public response to a proposal originally floated by S&P on December 6. The proposal focuses on a broad set of influences on financial strength—current capital, asset credit risk, interest rate and other market risks across assets and liabilities, risks of loss in different lines of business, the impact of diversification and so on—but provisions for setting capital on bonds and loans has drawn sharp fire. Any asset without an S&P rating, in the proposed approach, gets penalized. In particular:

- For corporate and government ratings, S&P lowers a Moody’s or Fitch investment grade rating by one notch and a speculative grade rating by two notches; for instruments rated by both, S&P uses the lowest notched rating

- For structured finance, S&P lowers the rating in general by three notches; if rated by both, S&P may lower the lowest rating by two notches

- For assets without an S&P, Moody’s or Fitch rating, the proposal would treat these assets as ‘CCC’

Treatment of assets without a rating from a major agency has drawn especially sharp fire. An asset rated ‘AAA’ by KBRA, DBRS Morningstar, Egan-Jones or other agencies would drop to ‘CCC’, potentially raising capital required under the S&P approach by more than 1,000 times.

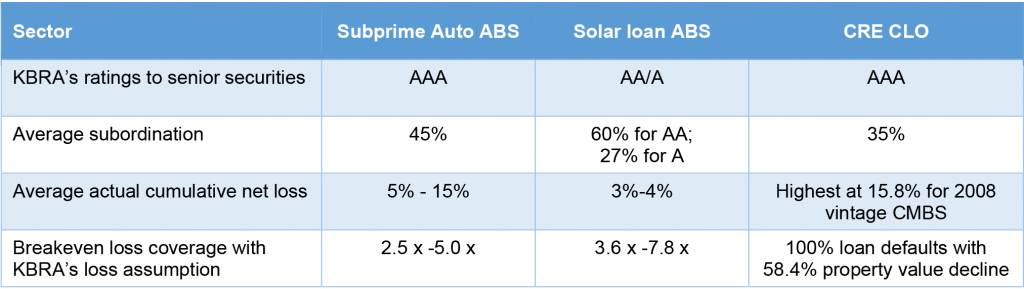

The KBRA response argues that S&P’s approach does not fairly assess the risk of KBRA-rated assets. The response focuses on subprime auto loan ABS, where both KBRA and S&P play, solar loan ABS, where KBRA dominates and S&P has just started to play, and CRE CLOs, where S&P has no market presence. In all examples, KBRA argues that structural protections should allow those securities to withstand losses in most draconian scenarios, a much stronger profile than ‘CCC’ (Exhibit 1).

Exhibit 1. KBRA’s breakeven loss coverage

Note: Breakeven loss coverage indicates the rated class could take a multiple of historic cumulative collateral losses before incurring loss of class principal. Protection comes from subordination, excess spread and other sources.

Source: KBRA

KBRA already has seen an impact from the S&P proposal. At least seven deals moving through the KBRA rating process have been put on hold since the S&P announcement by issuers concerned about going to market with a major rating agency, according to Caitlin Colvin, a managing director at KBRA. Some bankers have reported issuers taking deals to S&P that might have used only KBRA in the past.

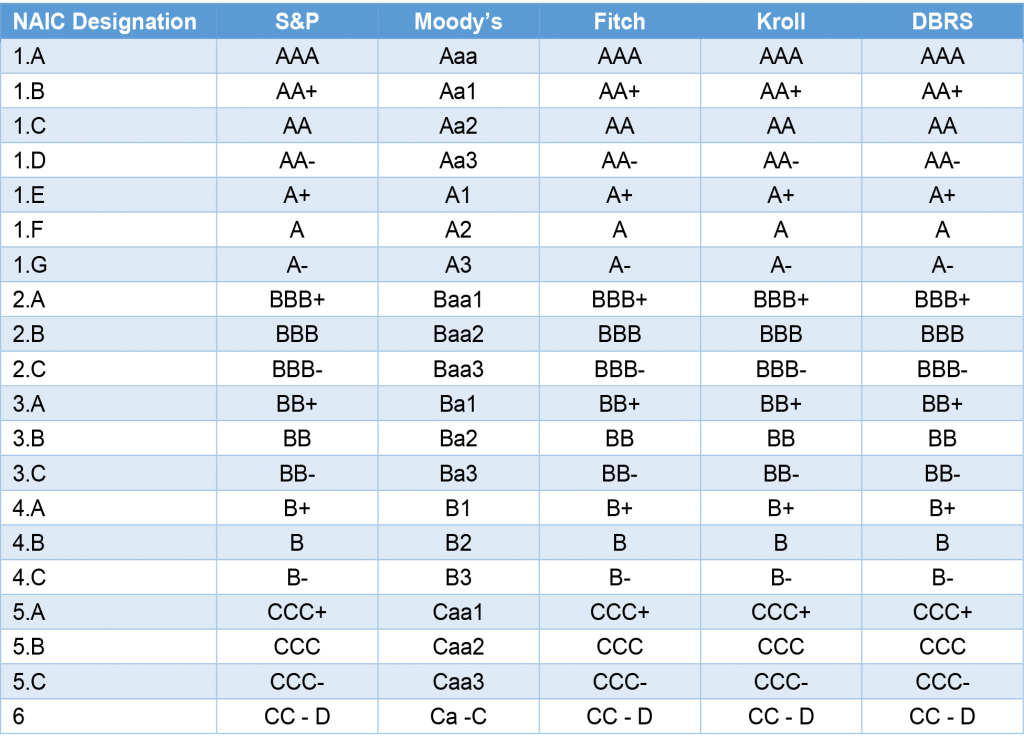

KBRA gets much better treatment under S&P’s current approach to insurer financial strength ratings, at least for US insurers. Where S&P does not have a rating on a security, the agency uses the current designation from the National Association of Insurance Commissioners to map to other rating agencies. That mapping puts KBRA and DBRS on even ground with S&P, Moody’s and Fitch (Exhibit 3). S&P is dropping this approach, however, in favor of one that would apply both inside and outside the US.

Exhibit 2. NAIC generic rating symbol mapping

Source: NAIC, available here.

S&P is taking comments on its approach through April 29, but market participants already started to react. Some insurance investors have reportedly stopped buying assets that might be affected by the proposed S&P approach and Structured Finance Association and the American Council of Life insurers plan to file comments on the proposal as well. And the Wall Street Journal reports that 26 congressional Democrats and Republicans sent a letter to SEC Chairman Gary Gensler on April 14 asking for a closer look into S&P’s move. “Many impacted stakeholders have expressed concern that this treatment of investments is potentially anticompetitive,” the letter said, “and we share this concern.”

For more background, see Concern continues around S&P insurer ratings.