By the Numbers

In CLOs, it pays for now to play in secondary

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors.

The secondary market in CLOs now trades at wider spreads than the primary market for securities with similar risk, making the secondary a much better place for relative value. Liquid ‘AAA’ classes, for example, lately have offered spreads in secondary as much as 16 bp wider than similar securities at new issue. For investors that can aggregate positions over time, there is size and opportunity.

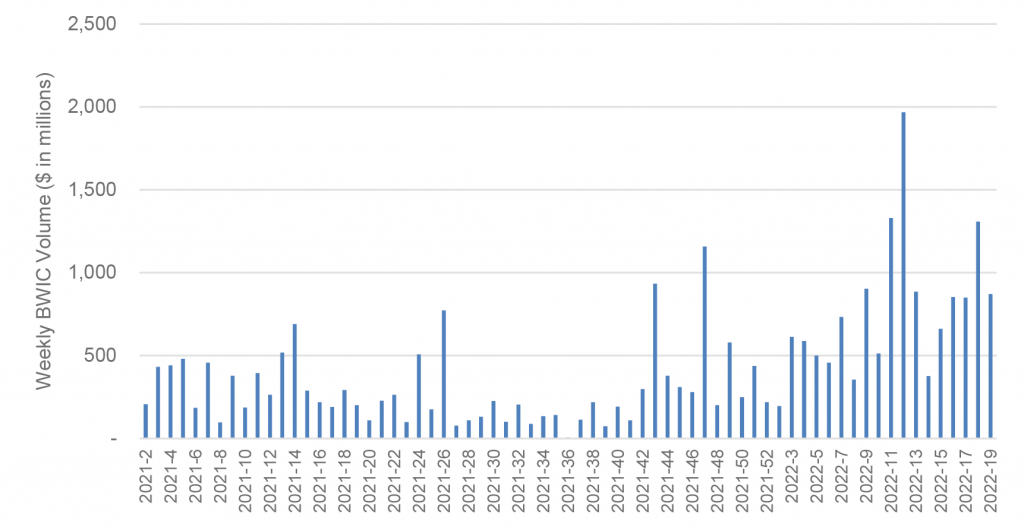

The secondary CLO market has seen heavy selling in recent weeks while the flow of new CLOs into the market has generally slowed. The median weekly volume of bid lists for ‘AAA’ CLOs, for example, ran at $219 million in 2021 but has jumped to $698 million this year (Exhibit 1). And ‘AAA’ bid list volume in the past four weeks has exceeded even this year’s elevated median volume.

Exhibit 1. US ‘AAA’ CLOs weekly bid list volume has jumped this year

Source: Amherst Pierpont Securities, Kopen Technologies

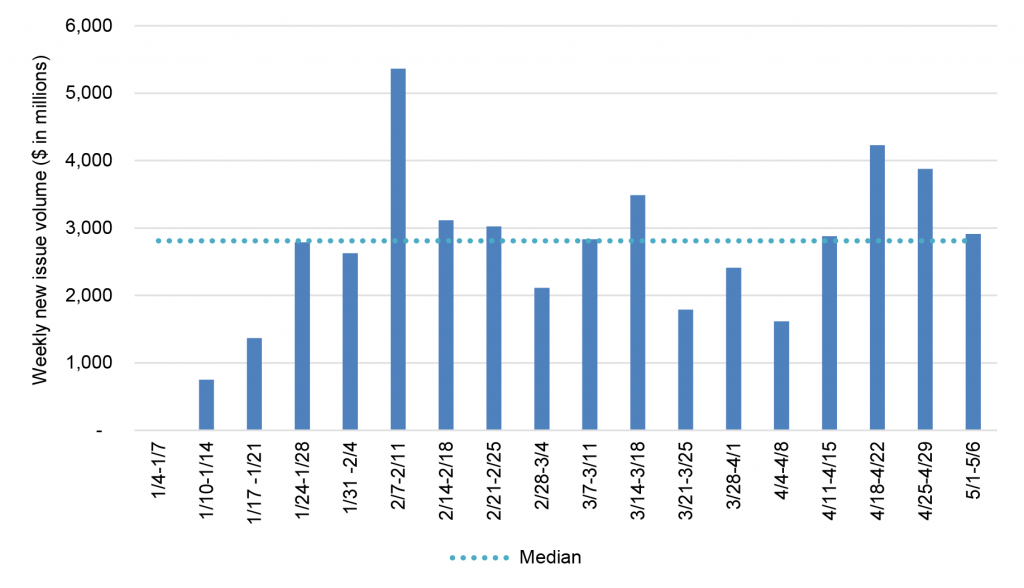

By contrast, the issuance of new CLOs had a slow start this year with uncertainties around the LIBOR-to-SOFR transition and steadily widening CLO debt spreads—often without similar widening in leveraged loans. The median weekly CLO new issuance volume year-to-date is $2.8 billion, and it takes CLO managers a longer time to get a deal closed in today’s market (Exhibit 2). It is also worth noting that a handful of deals closed recently used structures other than the traditional 5NC2, signaling the challenging economics of a traditional structure and the need for shorter structures and static structures to lower the cost of funds.

Exhibit 2. US CLO weekly new issuance volume recently has slumped

Source: Amherst Pierpont Securities, Bloomberg

Some recent flows highlight the gap between secondary and primary markets. CIFC Funding 2022-1A Class A appeared on a May 3 bid list offered at a discount margin of SOFR + 162 bp. CIFC is a relatively liquid platform with $25 billion in AUM, and it is a programmatic issuer with four deals closed year-to-date with an aggregate new issue volume of $1.9 billion. Amherst Pierpont analysis of past CIFC new issues indicates its debt usually trades 0.26 standard deviations tighter than its peers. Another CIFC LIBOR-indexed bond, CIFC Funding 2021-6A Class A, traded in secondary on May 6 with price talk of $98.5 to $98.8, implying a SOFR-based discount margin around 160 bp. But on May 9, Invesco 2022-2 Class A1 priced at a discount margin of SOFR + 144 bp. Invesco also is a relatively liquid platform with $6.2 billion in AUM, and this is the second deal priced with year-to-date new issue volume of $1 billion. Amherst Pierpont analysis of past Invesco new issues shows its debt prices on average 0.24 standard deviations tighter than peers—very close to CIFC. A high-level loan attributes comparison across the CIFC and Invesco deals along with APS CLO manager model outputs show comparable risk (Exhibit 3).

Exhibit 3. Comparable risk across CIFC and Invesco ‘AAA’

Source: Amherst Pierpont Securities, INTEX, KopenTechnologies

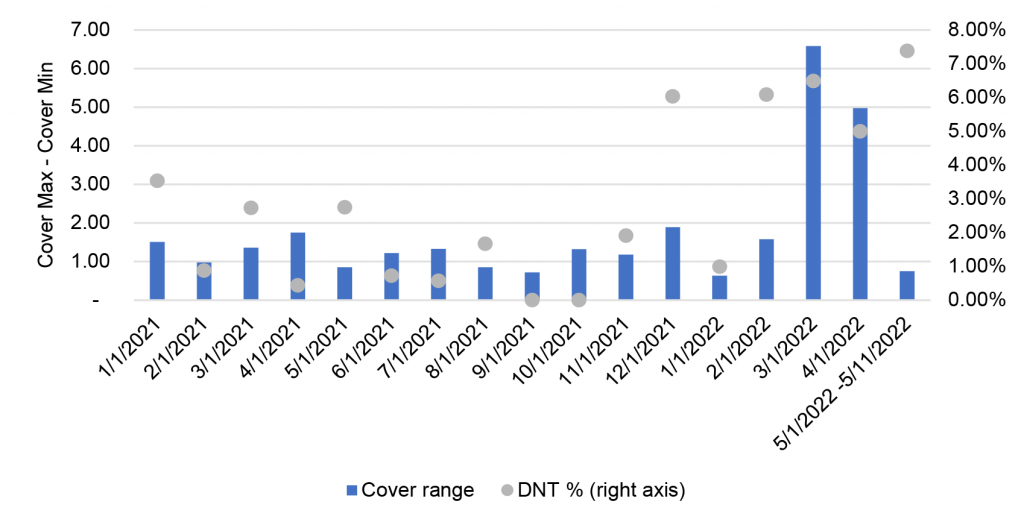

The heavy bid list volume in recent weeks has come with an increase in the share of bonds that do not trade and widening price talk in the secondary market. For example, the difference between the highest and the lowest cover for ‘AAA’ CLOs traded in a month was range-bound at 0.5 to 1.5 points last year, but the difference has increased to 5 to 6 points in the last two months (Exhibit 4). The wide secondary market is presenting opportunity for investors to find some good value. APS’s latest review of CLO managers performance can be found in the newly launched APS CLOutlook.

Exhibit 4. Price gaps and DNTs have jumped for ‘AAA’ CLOs in secondary

Note: DNT ratio is computed as the number of DNT bonds over number of posted securities in a month.

Source: Amherst Pierpont Securities, Kopen Technologies

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2024 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.