The Long and Short

M&A playbook for the financial sector

Dan Bruzzo, CFA | May 20, 2022

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors.

Corporate balance sheets remain strong despite recent hits to equity prices, and investment grade corporate debt funding remains readily accessible. It all adds up to a favorable environment for large-scale M&A. Over the past several months the financial sector has seen an uptick in notable deal announcements with issuers taking advantage of lower market caps and attractive financing options in the public debt markets. Some look like fair value. Some look like good relative value.

Bloomberg provides a full list of active and occasionally inactive deal proposals through its M&A Arbitrage screen, MARB, designed to help equity investors target opportunities where equity gains may be potentially unrealized. The list includes deal proposals in the financial sector with investment grade debt outstanding on at least one or both sides of the potential transactions. Some offer good relative value.

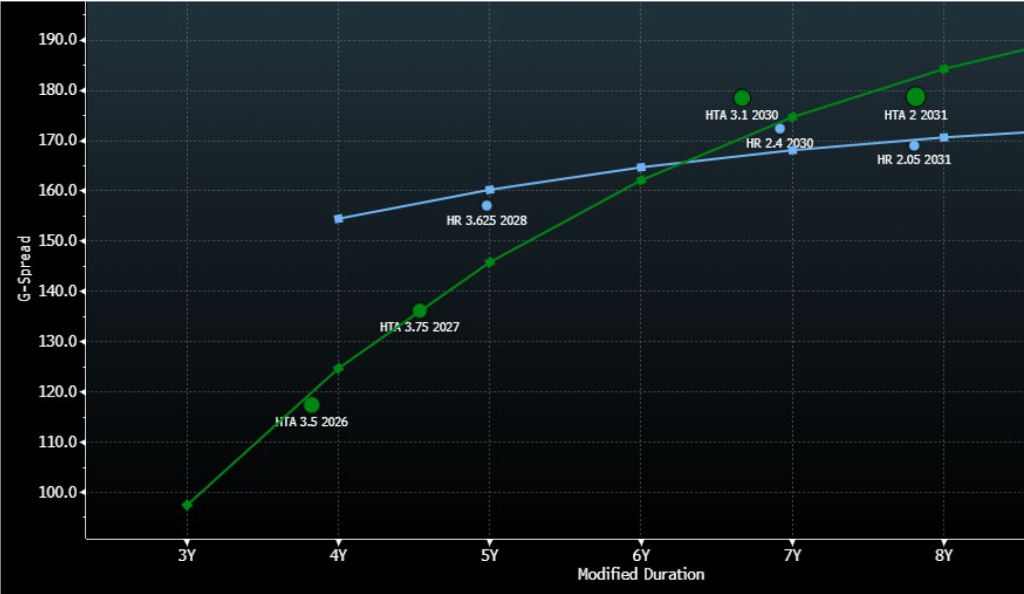

Acquirer: Healthcare Realty Trust Inc. (HR: Baa2/BBB/BBB+*-)

Target: Healthcare Trust of America Inc. (HTA: Baa2/BBB)

Announcement Date: 02/28/22

Projected Closing Date: 09/30/22

Market Value / Total Value: $6.7 billion / $10.0 billion

Deal Type: All Stock

Current Deal Status: Both parties have agreed to the combination and remain committed to the deal in the face of an unsolicited buyout offer from WELL (see below), the shareholder vote is expected to take place in July.

Debt Status: Although it was not explicitly stated in the press release or investor presentation, we would expect the likelihood of a legal assumption or explicit guarantee by HR of the HTA debt on closing.

APS Takeaway: Both parties appear satisfied with the terms and the deal appears likely to garner shareholder approval when it comes to a vote later in the year. Regulatory approval also appears likely given the unique positioning of each company’s property portfolios, and relatively moderate size the combination would present relative to the rest of the industry. The prospect of another hostile offer from WELL for HR seems to be the biggest uncertainty in this situation. As the two bond curves are trading closing in-line, bonds from both issuers reflect fair value of the high likelihood of the deal being completed as proposed.

Exhibit 1. HR and HTA senior debt obligations

Source: Amherst Pierpont, Bloomberg TRACE/BVAL

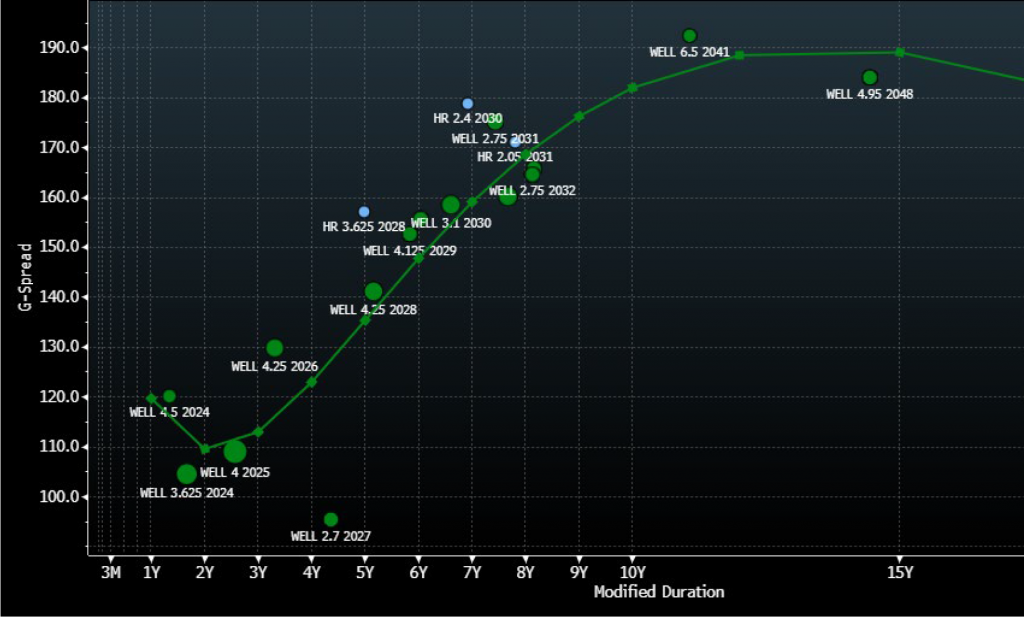

Acquirer: Welltower Inc. (WELL: Baa1/BBB+)

Target: Healthcare Realty Trust Inc. (HR: Baa2/BBB/BBB+*-)

Announcement Date: 03/28/22

Projected Closing Date: NA

Market Value / Total Value: $4.8 billion / $6.7 billion

Deal Type: All Cash

Current Deal Status: HR acknowledged that they received and subsequently rejected the alternative proposal from WELL in early May and stated that they remain committed to the HTA deal.

Debt Status: There is no deal in place but if negotiations were to pick back up, we would anticipate the legal assumption and/or guarantee of HR debt obligations would be likely if a deal between the two were to materialize.

APS Takeaway: WELL’s attempt to scuttle the HR/HTA deal may have been too little too late, but we would not rule out another attempt with more aggressive deal terms. Either way, it would appear that WELL is clearly in the market for assets, whether it be another pass at HR or another player in the industry. HR appears appropriately discounted to WELL on the likelihood of it remaining a standalone credit.

Exhibit 2. HR senior debt obligations vs the WELL curve

Source: Amherst Pierpont, Bloomberg TRACE/BVAL

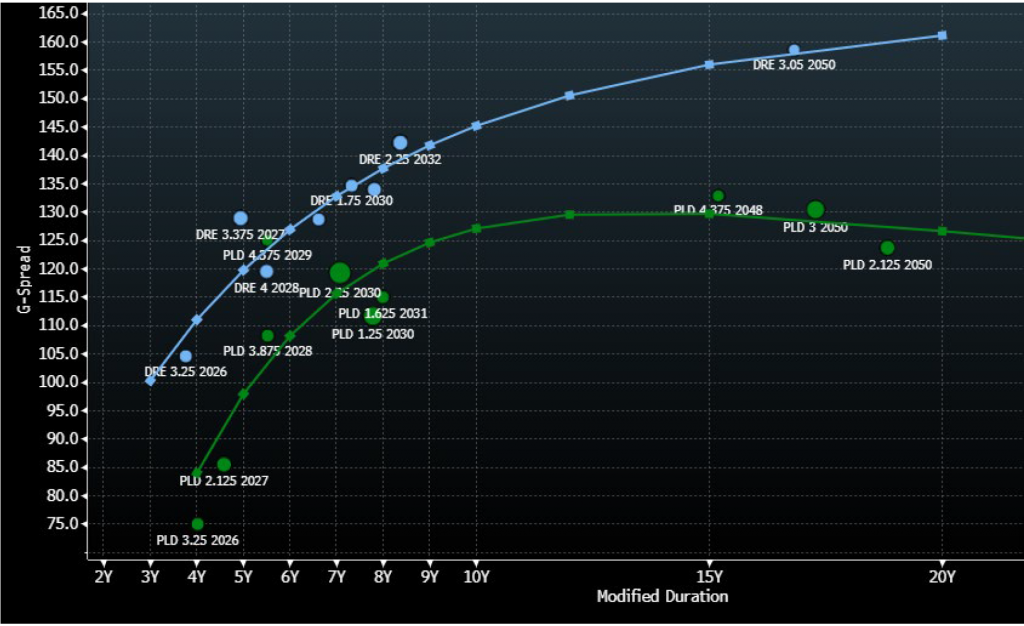

Acquirer: Prologis Inc. (PLD: A3/A-)

Target: Duke Realty Corp. (DRE: Baa1/BBB+)

Announcement Date: 05/10/22

Projected Closing Date: NA

Market Value / Total Value: $28.8 billion / $32.4 billion

Deal Type: All Stock

Current Deal Status: On May 11, 2022, DRE management stated that the acquisition proposal was “insufficient” but did not provide a hard and fast no on potential bids with more competitive terms.

Debt Status: There is no deal in place but if negotiations were to pick back up, we would anticipate the legal assumption and/or guarantee of DRE debt obligations by PLD would be likely if a deal were to materialize.

APS Takeaway: This is not the first attempt by Prologis to seek a merger with their biggest competitor in the industry, but they have been repeatedly rebuffed by DRE management. The steep sell-off in stocks has created another window of valuation for PLD to pursue a deal but it would likely require a more attractive premium to shareholders to generate any real momentum. Although it is difficult to rule out another offer on the near-term horizon, the current offer seems dead on arrival. DRE debt appears attractively discounted to PLD given its strong standalone credit profile and the prospect of a sweetened offer materializing.

Exhibit 3. DRE senior curve vs the PLD curve

Source: Amherst Pierpont, Bloomberg TRACE/BVAL

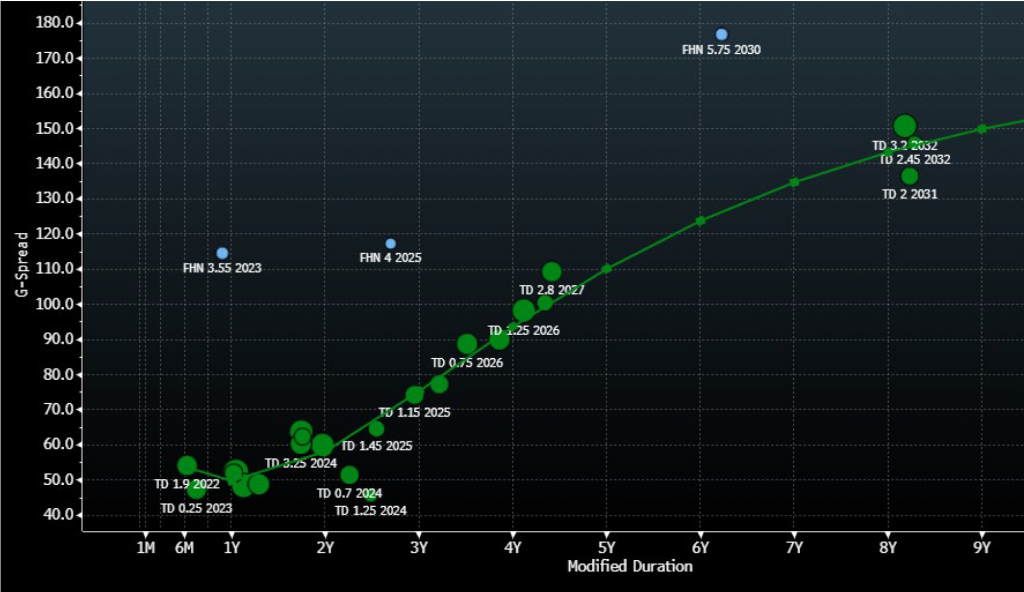

Acquirer: Toronto-Dominion Bank (TD: A1/A)

Target: First Horizon Corp. (FHN: Baa3*+/BBB-*+/BBB*+)

Announcement Date: 02/28/22

Projected Closing Date: 03/31/23

Market Value / Total Value: $13.4 billion / $13.4 billion

Deal Type: All Cash

Current Deal Status: Both parties have agreed to the terms of the proposal, the deal now awaits shareholder and regulatory approval.

Debt Status: We would expect that the debt of FHN is legally assumed but would most likely not be explicitly guaranteed by TD.

APS Takeaway: Regulatory approval is never an easy thing to predict, particularly when it involves an acquiring bank from across the US border. That said, US regulators have been much more receptive to deals involving US regional banks (particularly those with <$250 billion in assets) over the past few years, as the reluctance and scrutiny of bank deals that followed the financial crisis has gradually dissipated. We would expect that the deal has a reasonably high likelihood of gaining approval from both shareholders and regulators, but the absence of progress up to this point is at least worth noting. While regulatory approvals remain tricky to predict, FHN debt presents an opportunity for significant spread compression, subject to liquidity as the bonds do not trade with high frequency.

Exhibit 4. FHN senior holdco and sub bank notes vs TD senior curve

Source: Amherst Pierpont, Bloomberg TRACE/BVAL

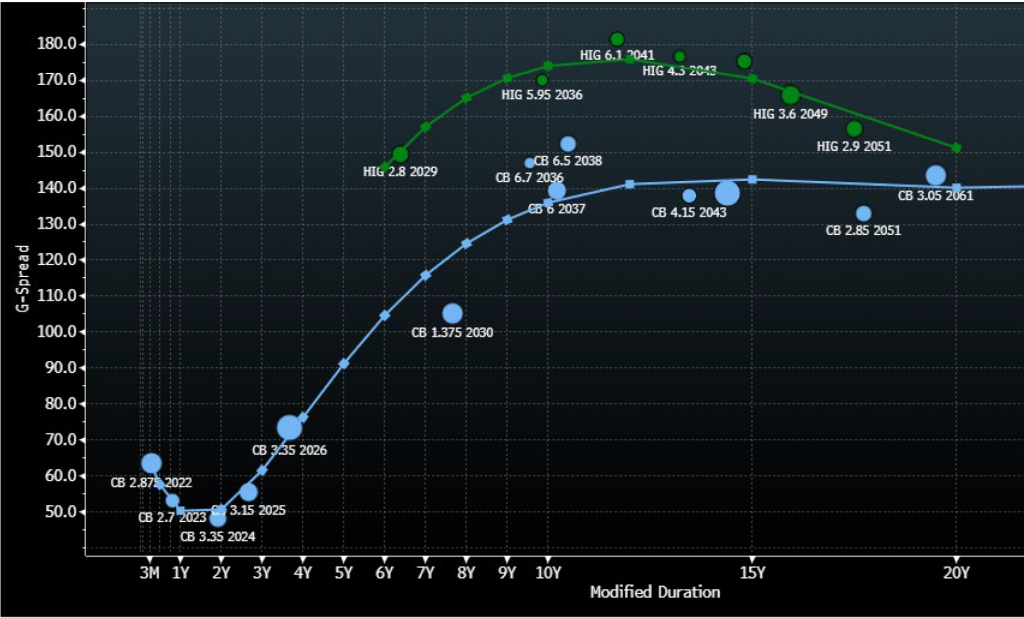

Acquirer: Chubb Ltd. (CB: A3/A/A)

Target: Hartford Financial Services Group Inc. (HIG: Baa1/BBB+)

Announcement Date: 03/18/21

Projected Closing Date: NA

Market Value / Total Value: $25.0 billion / $25.0 billion

Deal Type: All Cash

Current Deal Status: CB reportedly made three offers in total, twice sweetening the terms—including a final offer of $70 per share (60/40 cash/stock) on 4/14/21.

Debt Status: There is no deal in place, but were negotiations to pick back up, the legal assumption of HIG debt obligations would be likely if a deal were to materialize, but not necessarily an explicit guarantee.

APS Takeaway: It has been over a year since the deal was last proposed by CB and subsequently rejected by HIG. With the ongoing washout in equity prices, it is entirely possible that CB could take another pass at HIG or pursue another similarly positioned P&C company within the industry. It does not appear at this point that HIG debt should trade with any real premium on takeover prospects unless talks resurface. HIG debt appears appropriately discounted to CB given that deal prospects between the two entities have been extremely quiet since first being proposed in 2021.

Exhibit 5. HIG senior curve vs CB senior curve

Source: Amherst Pierpont, Bloomberg TRACE/BVAL

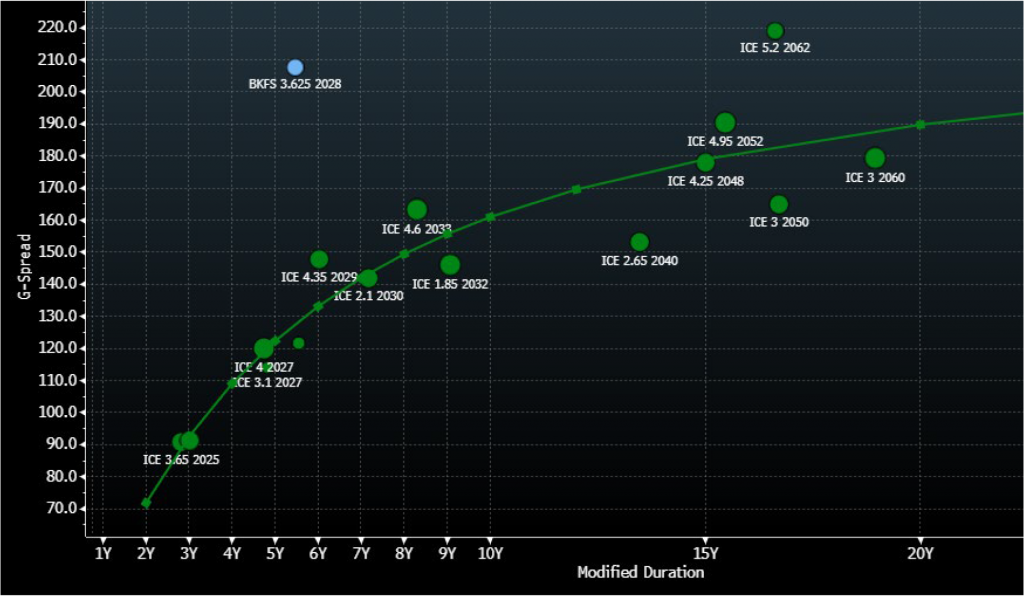

Acquirer: Intercontinental Exchange Inc. (ICE: A3/A-)

Target: Black Knight Inc. (BKI: Ba2*+/BB*+)

Announcement Date: 05/04/22

Projected Closing Date: 06/30/23

Market Value / Total Value: $13.3 billion / $15.6 billion

Deal Type: Cash/Stock 80%/20%

Current Deal Status: Both sides have agreed to the terms of the proposal. ICE wasted very little time in pre-funding the bulk of the cash financing (~$10.5) for the transaction with a public USD debt launch for $8 billion, which contains $101 Special Mandatory Redemption (SMR) language through May 4, 2023 (ICE/BKI debt launch).

Debt Status: ICE has not yet provided a firm indication on the treatment of BKI debt once the deal has closed, but we would expect a high likelihood of a legal assumption and/or explicit guarantee of the debt upon closing.

APS Takeaway: This deal seems unlikely to encounter any significant shareholder or regulatory resistance at this early phase, but it is a reasonably long road to closing. BKI’s only public USD debt outstanding has already reacted sharply to the prospect of the takeover, but still trades at a deep discount to the IG-rated ICE notes. To the extent that investors have appetite for high yield credit, the Black Knight 2028s could benefit from extraordinary spread compression from this early stage in the process.

Exhibit 6. BKFS vs ICE senior curve

Source: Amherst Pierpont, Bloomberg TRACE/BVAL

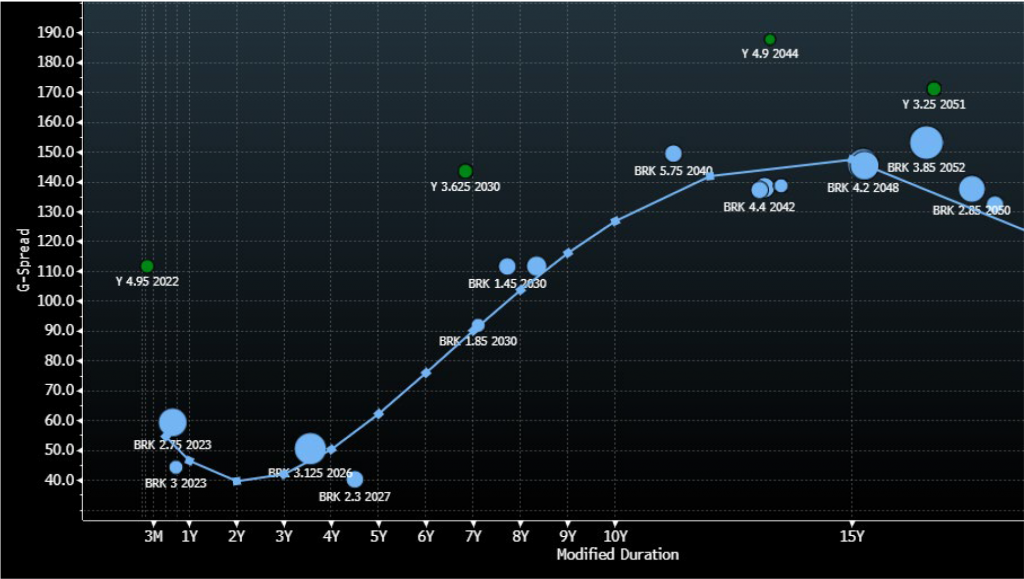

Acquirer: Berkshire Hathaway Inc. (BRK: Aa2/AA/A+)

Target: Alleghany Corp. (Y: Baa1*+/BBB+*+)

Announcement Date: 03/21/22

Projected Closing Date: 12/31/22

Market Value / Total Value: $11.5 billion / $13.7 billion

Deal Type: All Cash

Current Deal Status: Both sides have agreed to the terms of the proposal. A brief “go shop” period has recently expired with no competing offers materializing for Y. There are some shareholder suits alleging a lack of disclosures, but BRK has so far avoided either serious pushback or a bidding war despite efforts to solicit competing offers.

Debt Status: BRK has not yet provided a firm indication on the treatment of Y debt once the deal has closed. It would appear likely that BRK would legally assume the debt of the subsidiary upon closing based on historical treatment of insurance operating subsidiaries, but we do not think BRK would provide an explicit guarantee of the debt obligations of the new operating subsidiary.

APS Takeaway: This would be BRK’s first big foray into insurance in a long time, and the company’s largest acquisition in six years. A competing offer would have likely been among the bigger risks to this deal not getting executed, as BRK is not in the habit of getting drawn into a bidding process once it has identified value in a particular market. There are definitely some law firms seeking to solicit shareholders ahead of approval, with some claiming lack of proper disclosures. It is fairly early in the process, and therefore still plenty that could go wrong. Nevertheless, given BRK’s track record of executing once it commits to a target and no reasonable concerns regarding regulatory approval, this deal does seem like it has a good chance for success. Alleghany debt trades with an attractive discount to BRK given solid prospects for deal execution.

Exhibit 7. Y senior debt obligations vs the BRK curve

Source: Amherst Pierpont, Bloomberg TRACE/BVAL

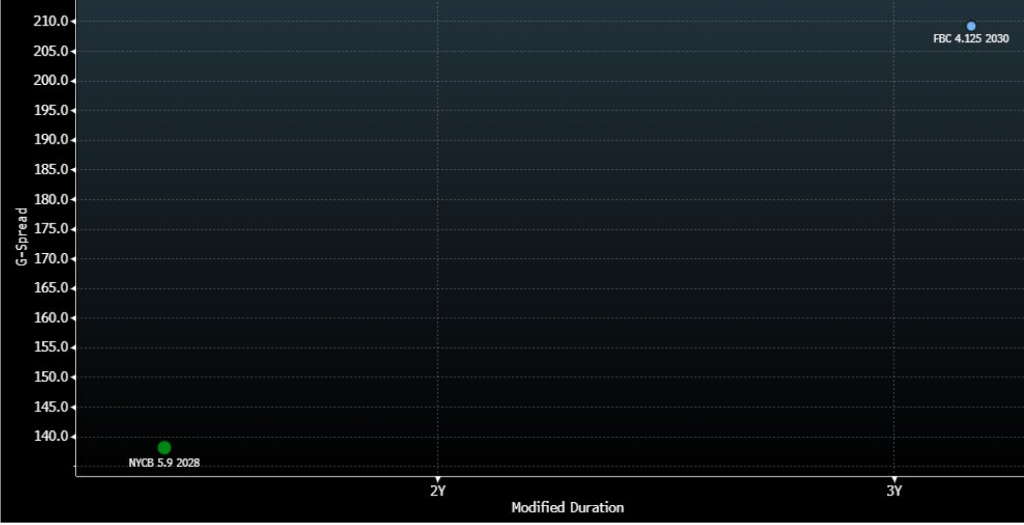

Acquirer: New York Community Bancorp (NYCB: Baa3/BB+/BBB)

Target: Flagstar Bancorp Inc. (FBC: Baa3/A(EJR)/BBB+(KBRA))

Announcement Date: 04/26/21

Projected Closing Date: 12/31/22

Market Value / Total Value: $1.9 billion / $2.6 billion

Deal Type: All Stock

Current Deal Status: Both sides have agreed to the terms of the proposal, and recently mutually agreed to extend the merger agreement through October 31, 2022. The deal received some initial protests from legal firms on the behalf of shareholders. The deal awaits regulatory approval from the Federal Reserve Board and the OCC.

Debt Status: We would expect that the debt of FBC is legally assumed but not explicitly guaranteed by NYCB.

APS Takeaway: Fresh concerns seem to have emerged with the extended merger agreement and plans to seek a national banking charter. Still, the deal seems small enough to fly under the radar of the deepest levels of regulatory scrutiny in the banking industry. The deal still appears to have a good prospect of closing as presented but we could not rule out the possibility that further delays shake investor confidence. There is a huge gap in valuation between the only (non-hybrid) debt outstanding – the NYCB 5.9s ’28 versus the FBC 4.125 ’30, which are both subordinated issues with front-end calls. While FBC debt could see credit uplift with a completion of the deal, it may be too difficult to exploit this opportunity given a lack of liquidity in the FBC bonds.

Exhibit 8. FBC vs NYCB – 10NC5 subordinated debt issues

Source: Amherst Pierpont, Bloomberg TRACE/BVAL