Uncategorized

Markets: A trade war of attrition

admin | May 24, 2019

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors.

Both the US and China at this point seem intent on wearing each other down in their trade war to the point where one side finds the prospective costs too high to bear. Each side probably has a fair idea of the costs the other might impose, but neither knows when the costs become unbearable. That’s invitation to steady, small tests of the other side’s willingness to continue. That’s trench warfare, and, for fixed income markets, steady volatility.

The headline costs for each side seem relatively clear. The imports, exports, companies, people and places involved are largely transparent. Data on international trade are plentiful. The gross costs are just a matter of which flows get hit with tariffs, by what amount and when. Both political leaders and their advisors should have a clear picture of the prospective stakes.

The net costs to each side may be a little fuzzier. The impact of tariffs depends on whether the exporter, the importer or the eventual buyers bears the cost. It depends on whether importers or buyers find substitute products. But economists have estimates of these nuances, so still the range of prospective stakes is presumably sketched out.

Both sides so far still seem more willing to escalate the trade conflict rather than deescalate. Each side must be assuming the other will eventually fold. The wildcard is pinpointing when costs on each side become unbearable.

Both sides likely have areas—economic and political—where the impact of trade war does become unbearable. Damaged economies, angry constituencies, volatile financial markets are on the list for both the US and China. These things are arguably more visible in the US than in China, but political analysts argue that they exist in China nevertheless. But their very visibility in the US may give China an advantage in knowing the trade war’s impact. Still, it’s likely to be a hazy picture that takes time to clear.

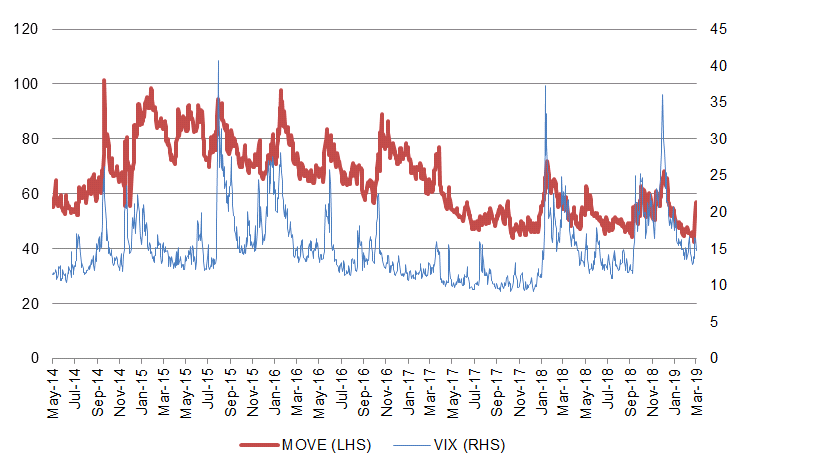

Both equity and fixed income implied volatility lately have spiked as the markets have started to anticipate a steady, grinding confrontation. It’s plausible that the conflict could play well into next year and get either amplified or resolved depending on which endgame works best for the 2020 elections. Either side might run too high a political risk by folding before then.

Exhibit 1: Both equity and rate implied volatility lately have spiked

Source: Bloomberg

For fixed income investors, getting long volatility, or alternatively, buying convexity should be a valuable hedge.

* * *

The view in rates

Trade friction has already appeared on the Fed’s list of reasons to watch and wait, and it seems increasingly likely to tilt the Fed toward an ease. The market has already put a nearly 80% probably on a Fed cut this year. Threats to growth stand to compound concerns about low inflation as reflected in recent remarks by Fed Governor Lael Brainard. Explanations for low inflation vary, but the Fed seems to be appropriately focused on inflation expectations and ways to keep them anchored around 2%. Breakeven 10-year inflation continues to drop, recently hitting 177 bp. The likely fundamentals of long-run growth should keep long rates biased toward 3.00%, but, unless a new trade agreement is brokered, expect those yields to stay out of reach.

The view in spreads

Spreads in investment grade debt continue to widen as trade frictions pick up It’s an appropriate repricing as prospective global growth comes under pressure. Over the longer term, a relatively flat yield curve, low volatility and heavy net supply of Treasury debt should re-tighten spread markets, but the timing will depend on trade as well. The longer the Fed remains patient, the longer the spread advantage in assets other than Treasury debt compound to the advantage of portfolio return. Leverage and loosening of underwriting remain a concern in investment grade corporate debt and leveraged loans, but concerns about recession, which would trigger those vulnerabilities, have diminished. Agency MBS could see a softening of bank demand, but it should still outperform credit.

The view in credit

Companies have started to divert cash flow toward paying down debt, have started to sell non-core assets and have curtailed stock buybacks. Management has heard the concerns of debt investors. Households continue to look strong with low unemployment, rising home prices, and generally good performance in investment portfolios.