The Long and Short

The AerCap GECAS merger triggers a repricing of debt

Dan Bruzzo, CFA | March 12, 2021

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors.

This week, AerCap Holdings (AER: Baa3/BBB/BBB-*-) made official their plans to merge with General Electric’s (GE: Baa1/BBB+*-/BBB) aircraft leasing business, GE Capital Aviation Services (GECAS). The combination will create an industry juggernaut, while GE takes the next big step in its multi-year turnaround. The potential negative ratings consequences for AerCap have contributed to a widening of their debt spreads, while GE bonds have tightened on news of the merger.

AER will pay $24 billion in cash, plus an AER equity interest worth $5-6 billion, and $1 billion of AER notes for total consideration of around $30 billion. AER already has $24 billion in committed capital in place from Citigroup and Goldman Sachs to cover the cash portion, the majority of which will ultimately be termed out in a large-scale public debt launch likely to be completed between now and the scheduled closing by year-end 2021. It appears AER will be able to execute the debt launch with investment grade ratings intact.

The rating agencies have already weighed in on the proposed transaction. Both Moody’s and S&P affirmed AER at Baa3/BBB with a negative outlook, while Fitch was the only agency to threaten IG ratings by placing the BBB- rating on watch negative. Fitch stated that they could resolve the review if and when “AerCap makes sufficient progress toward securing term financing, provided that there is no material deterioration in the company’s unsecured funding mix or the surrounding operating environment.” As for GE, Moody’s affirmed the Baa1 rating with a negative outlook, while Fitch also affirmed its BBB rating with a stable outlook. In a somewhat surprising move, S&P placed the BBB+ rating on watch negative and stated its intention to lower the senior rating to BBB when the transaction closes, reflecting the expected near-term increase in debt leverage to about 6x, even with the expected use of proceeds for debt reduction.

For GE, the sale would represent one of the biggest and most anticipated transactions toward the company’s multi-year turnaround efforts to scale down the remaining elements of legacy GE Capital, and vastly deleverage the total company balance sheet. Adjusted leverage is currently viewed to be around 6x, with management’s target to achieve 2.5x long-term still intact with the announcement of the plans to jettison GECAS. A bigger element of the company’s goal to reach this leverage target now rests on the shoulders of the turnaround of its aviation business, which has seen considerable stress as a result of the global pandemic. In the most recent quarter, GE saw better than expected cash flow with improved performance in its power segment helping to offset decreased revenue in Aviation.

Meanwhile, AER will become the global leading aviation leasing company by a longshot with over 2,000 owned and managed aircraft in its portfolio, servicing roughly 200 customers worldwide. This would dwarf their closest current competition by nearly 4x. Average fleet age will be just under 7 years with an initial split of 59% narrowbody and 40% widebody, which the company expects to improve to 66%/33% within the first three years of operation, as a result of the two entities’ combined order book. The acquisition will also enable AER to write down the book value of about half of their fleet to help minimize future writedowns and unexpected charges over the near-term.

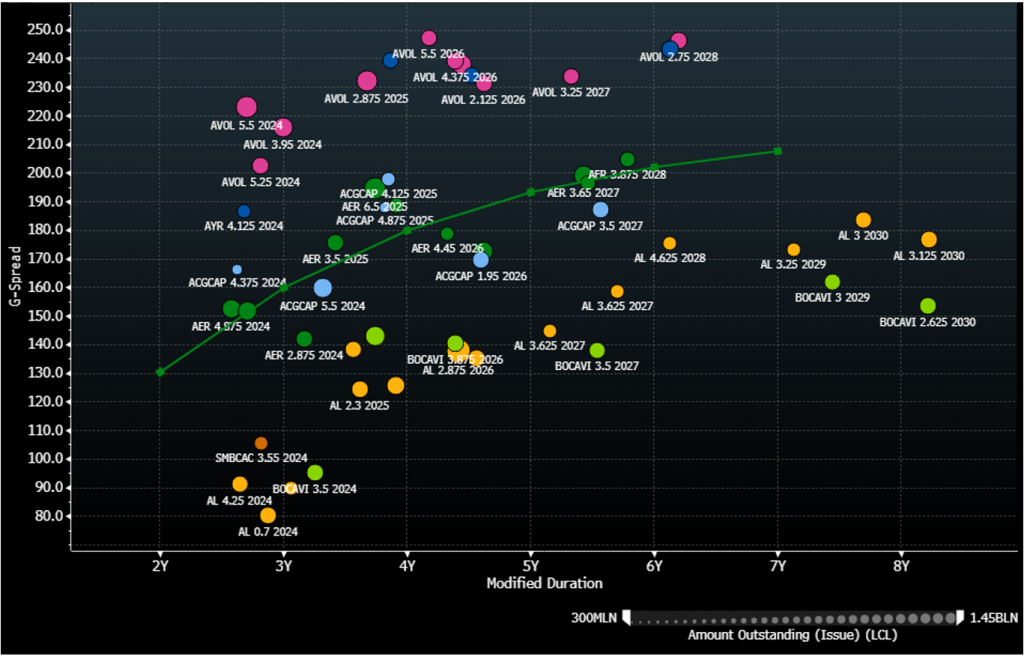

Exhibit 1: AER bonds vs Aircraft Leasing peers

Source: Amherst Pierpont Securities, Bloomberg/TRACE Indications

AER bond spreads have widened about 20 bp with the announcement of the transaction, with 5-year notes now trading about +170 bp to the curve (Exhibit 1). Obviously, the prospect for massive issuance on the horizon is weighing heavily on valuation, but bonds are now currently priced at fair value relative to peer credits.

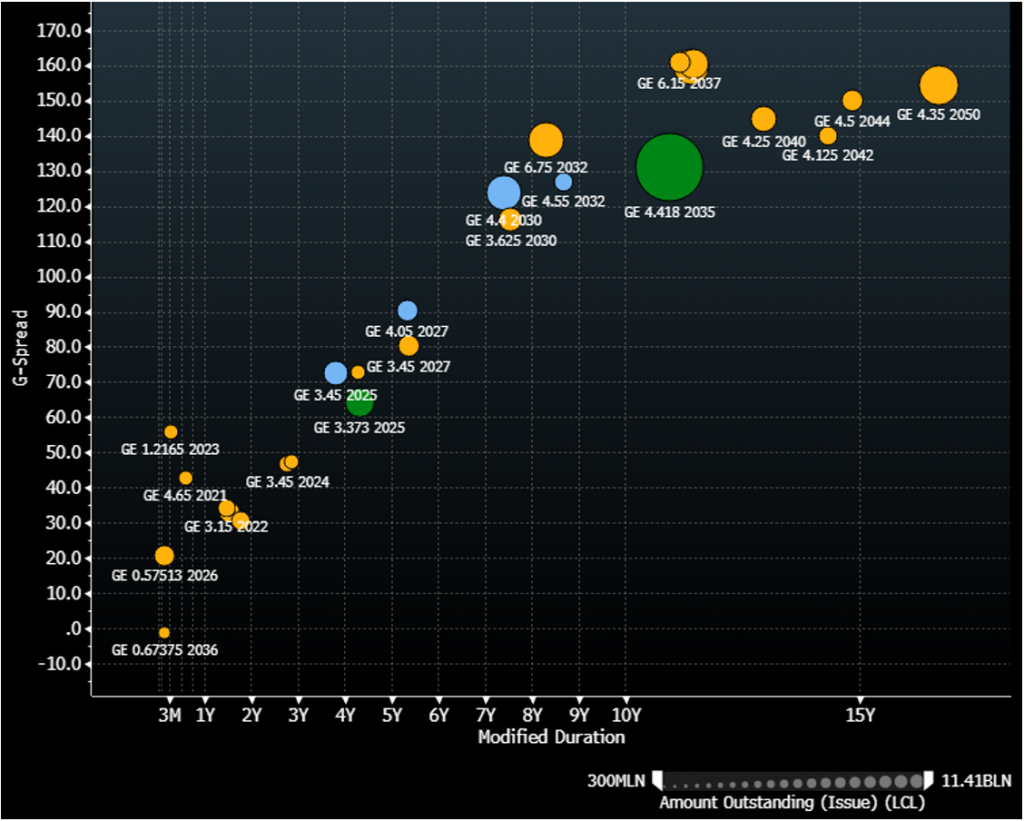

Concurrently, GE bonds have tightened roughly 10-15 bp with the news of the merger becoming official (Exhibit 2). These bonds are attractively valued; in particular, given the limited prospect for issuance creating scarcity value over the near-to-intermediate term and the ability for investors to position bonds that could be targeted in subsequent debt reduction efforts via tender offer. GE only has about $11.5 billion in maturities rolling off in the next three years, which would imply that much more debt will need to be redeemed via active tender offer or make-whole to reach management’s debt reduction targets with the proceeds of the sale.

Exhibit 2: GE bond curve (GE Co – yellow, GEICF – green, GECF – blue)

Source: Amherst Pierpont Securities, Bloomberg/TRACE Indications

Worth noting is that when GE recapitalized back in 2015, all bonds issued under the then new banner of GE Capital International Funding (GECIF) were fully and unconditionally guaranteed by General Electric Co. and the legacy General Electric Capital Corp (GECC); the latter of which was subsequently dissolved into the parent company, converting all legacy GECC debt obligations into GE Co. debt. More recently, GE issued debt under a new entity GE Capital Funding LLC (GECF), which was also fully and unconditionally guaranteed by GE Co. This was done presumably so that the Fed would consider GECF a domestic entity under its bond buying programs, and perhaps also to make the launch more marketable since a portion of proceeds were being used to retire GECIF debt, which falls under the Finance Company classification in the IG index. What this all adds up to is that instead of the once notable split between GE and GECC debt, all remaining outstanding US dollar senior GE debt is either at General Electric Co. or GECIF or GECF, which are both pari passu via a fully and unconditional guarantees from GE Co.