The Big Idea

Inflation expectations follow the Fed

Stephen Stanley | June 4, 2021

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors.

Inflation has suddenly become the hot topic in financial markets, as the bulge in price hikes while the economy reopens threatens to fundamentally alter the economic landscape. TIPS breakevens offer a real-time window into how investors expect inflation to evolve. A detailed examination of the TIPS breakevens curve suggests that financial market participants are largely on board with the Fed’s narrative that inflation will accelerate for a short time and then return to the 2% target.

TIPS breakevens explained

For those not intimately familiar with the TIPS market, breakeven rates represent, as the name implies, how high inflation would need to be over the term of the inflation-indexed security for a buyer to earn the same return as another investor holding a nominal Treasury security with the same maturity. There are time-varying risk and liquidity premia imbedded in these calculations that present slight complications, but, as a first approximation, TIPS breakeven rates offer a reasonable rough estimate of the inflation rate that investors are anticipating over various time periods.

In terms of TIPS mechanics, the securities are indexed to the headline CPI, and the inflation payout to TIPS holders is slightly lagged. As an example, the TIPS inflation payout for May 2021 would be the CPI reading released in April, which would be the March CPI figure. Since the Fed focuses on the PCE deflator in its inflation targeting, we do have to make an adjustment to translate from the CPI. Over the last 20 years, the CPI has on average run almost three tenths higher than the PCE deflator, a gap that we will need to take account of.

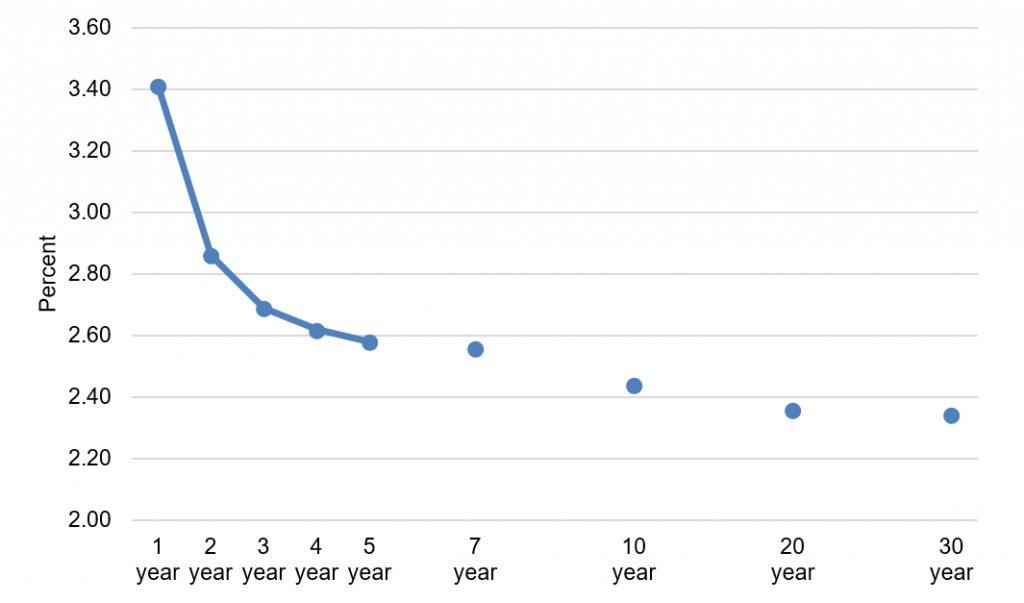

TIPS breakeven yield curve

Bloomberg reports TIPS breakeven rates across various maturities, allowing us to construct a yield curve of inflation expectations. At the moment, with inflation higher than usual, the curve is downward sloping (Exhibit 1). In fact, it slopes modestly downward all the way out to 30 years, a fully inverted curve, though once we move out beyond the first two or three years, the curve is pretty flat.

Exhibit 1: Yield Curve for Breakevens

Source: Bloomberg.

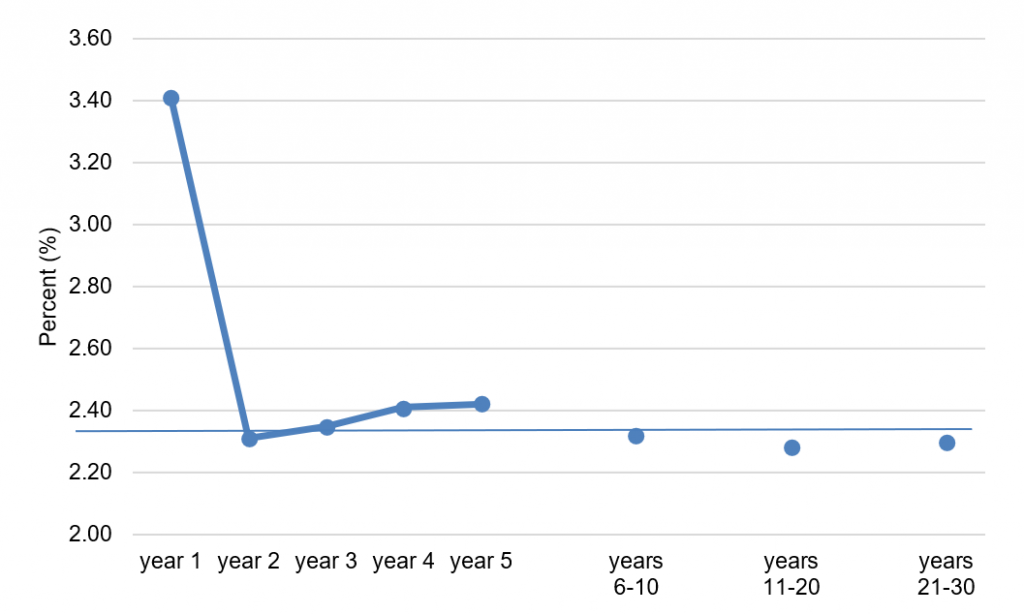

We can use these breakeven rates to tease out inflation expectations for specific years. For example, the 1-year breakeven rate is 3.41% and the 2-year breakeven rate is 2.86%. The arithmetic would then dictate that investors must expect inflation of 2.31% in Year 2. We can do these calculations to isolate expectations for given years (Exhibit 2).

Exhibit 2: Implied Inflation Expectations from Breakeven Rates

Source: Bloomberg.

Parsing the data in this way, it is evident that investors expect a sharp acceleration in inflation over the next year, followed by a return to roughly 2% inflation forever after. Inflation in Year 1 is expected to be 3.4%. However, in Year 2, the expectation slides to 2.3%, which, when adjusted for the CPI-PCE gap, implies that inflation would be exactly consistent with the Fed’s 2% target. In fact, the implied expectations are within a tenth or so of the magic 2.3% level over the entire 30-year period.

The data point for Year 6 through Year 10 is also known as the 5-year 5-year forward TIPS breakeven rate and is one of the favorite long-term inflation expectations proxies for many Fed officials. It is currently sitting at 2.32%, almost exactly consistently with the Fed’s target.

Assessing the market’s expectations

Based on the lag in the TIPS inflation payout, the breakeven rate for the next 12 months represents a projection of CPI inflation from April 2021 through March 2022. Of course, we already know that the CPI surged by 0.8% in April. Moreover, the consensus expects a 0.4% rise in May, while my forecast calls for a 0.5% advance. Using the consensus projection for May, that’s 1.2 percentage points over two months, which means that the 1-year TIPS breakeven rate implies an advance in the CPI over the 10 months from June through March 2022 of 2.2%, or 0.22% per month, which translates to a roughly 2.3% annualized pace for the PCE deflator over that timeframe.

In essence, the TIPS breakeven curve suggests that investors expect inflation to run slightly above a 2% pace for the next few months and then to settle at roughly a 2% pace (for the core PCE deflator) for the next 30 years.

My own expectation for the next 10 months is not radically different than the TIPS market implies. I expect the year-over-year CPI reading for March 2022 to be about 3.6%, just 15 bp above the breakeven rate. However, I am less optimistic further into the future, as I look for easy fiscal and monetary policy and a robust economy to generate inflation that is well above the Fed’s 2% target in 2022 and beyond, perhaps in the range of 2½% or so for the PCE deflator in 2022 and 2023.

Fed officials as of the March FOMC projections are closer to the TIPS market camp, as the median projection of policymakers called for roughly 2% PCE inflation in both 2022 and 2023.

I would imagine that most FOMC participants would be largely happy with what they see in the TIPS breakeven data. After running below the 2% mark for several years before the pandemic, the Fed has managed to successfully boost inflation expectations to exactly where they should want them. The run-up in TIPS breakeven rates so far is not in any way problematic for the central bank. It will be interesting, however, to see how policymakers react if breakeven rates imply a further acceleration of inflation going forward, especially well out the yield curve. In that case, it would potentially be time for the FOMC to push back. For now, however, it is easy to see why the committee is quite satisfied with what they see.