The Long and Short

Sell First Horizon to buy BankUnited

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors. This material does not constitute research.

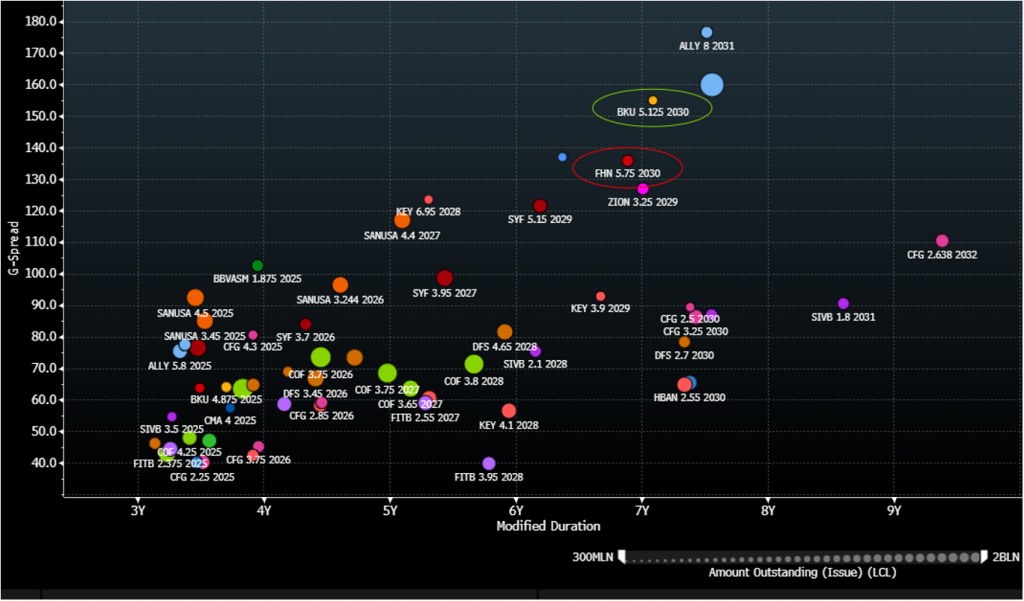

Investors can find a good relative value swap in selling selected subordinated First Horizon debt to go into similar BankUnited issues. While First Horizon is a significantly larger entity, the banks are otherwise highly comparable in terms of overall credit quality. The structural difference of trading from a subordinated bank issue into a subordinated holding company issue is mitigated by lack of complexity in BankUnited’s overall operations and capital structures. The trade: sell FHN 5.75% 05/30 to buy BKU 5.125% 06/30.

The particulars:

- SELL: FHN 5.75% 05/30 @ +125/20YR; G+136; 52%; $124.54

- BUY: BKU 5.125% 06/30 @ +145/20YR; G+155; 72%; $118.33

Investors can pick up around 20 bp of total yield by swapping from FHN 5.75% ‘30s to similar maturity BKU 5.125% ‘30s while maintaining comparable ratings and staying in index-eligible deal size. The trade also offers the opportunity to take out roughly $6 points of cash to move to a moderately lower coupon and lengthen by just one month of total maturity.

Both issuers trade at the wide end of the range for regional banks (Exhibit 1). They have very similar duration, which invites a potential swap. Other key considerations:

Exhibit 1: BBB regional banks

Source: Amherst Pierpont, Bloomberg/TRACE Indications

- BKU operates almost exclusively in its home state of Florida, where 68 of its 69 branches are currently located. The bank has just over $35 billion in total assets as of March 2021, with $28 billion in total deposits and $23 billion in total loans. Comparatively, FHN has nearly $88 billion in total assets with $73 billion in total deposits and $59 billion in total loans. The bank’s roughly 455 branches are spread out across its southeast footprint in its home state of Tennesee, as well as Arkansas, Alabama, Florida, Louisiana, Georgia, Virginia, North Carolina and South Carolina. FHN recently expanded its footprint meaningfully through the $2.3 billion purchase of IBERIABANK, which closed mid-2020. BKU has not made a substantial bank acquisition since 2012.

- BKU and FHN have similarly well-diversified loan books by loan category. BKU has 28% of loans in residential, 27% in commercial real estate (CRE), 19% in commercial & industrial loans (C&I), with about 15% categorized as non-real estate loans. FHN’s loan mix is classified as 28% C&I, 24% CRE (plus an additional 4% in construction and development), 20% residential, and approximately 17% in non-real estate lending.

- BKU currently maintains significantly higher capital ratios than FHN. The bank’s Tier 1 Common (CET) ratio was 13.18% as of 1Q21 versus 9.97% at FHN. BKU’s total risk-based capital ratio was 15.19% as of 1Q21 versus 12.84% for FHN.

- The two banks have comparable funding profiles, with both organizations primarily utilizing traditional deposit funding and neither overly reliant on higher-risk wholesale funding. BKU’s total loan/deposit ratio was 84% as of 1Q21, while FHN’s was 81%, as both banks maintain deposits well in excess of their total loan books. BKU’s total reliance on wholesale funding as of 1Q21 was 23%, which we view as highly appropriate, while FHN was just under 10%. Both banks have negligible levels of short-term wholesale funding as of 1Q21. BKU’s percentage of brokered deposits was a very manageable 12.5% as of 1Q21, while FHN’s was just under 5%.

Both banks have very low delinquencies in their loan books, reflecting relatively conservative lending practices. BKU’s non-performing assets (NPAs) were just 0.82% of total assets as of 1Q21. FHN’s NPA/Asset ratio was a very similar 0.67%. The banks’ adjusted Texas Ratios (which measure total NPA and 90-day past due loans as a percentage of tangible equity and loan loss reserves) were 12.15% and 8.46%, respectively as of 1Q21. We typically consider any score below 20% as appropriate for mid-sized regional banks like BKU and FHN.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2024 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.