The Long and Short

Updating the M&A landscape for US regional banks

Dan Bruzzo, CFA | September 24, 2021

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors.

It has been a very active year for bank consolidation in the US, with the most recent deal announced by US Bancorp (USB) to purchase the bulk of US banking operations from MUFG (the old Union Bank branch network). A re-cap of noteworthy merger and acquisition activity shows that several of the bank candidates identified in last year’s study have already been linked in deals announced throughout 2021. An update to our universe of US bank merger candidates with public debt outstanding is available for event driven corporate investors.

In late 2020, two major regional bank mergers were announced prompting our study – PNC Financial’s purchase of BBVA USA Bancshares for $11.6 billion, which is very similar to the recent USB/MUFG deal, and Huntington Bancshares purchase of TCF Financial for just over $5 billion. A further wave of consolidation had long been percolating in the sector. Low rates and weak loan demand make operating efficiency one of the best ways for banks to defend profits. Bank balance sheets have expanded over the past few years as deposits have ballooned. Meanwhile, the prospect for loan growth has remained muted with tempered demand that even preceded the pandemic. These factors, along with easy access to capital, had helped create an ideal environment for further bank deals to be announced. Bank regulators have also been increasingly receptive to mergers of relevant size among regional banks.

USB’s merger announcement with MUFG on 9/21/21 was just the most recent of several noteworthy deals in 2021. The deal will add $105 billion in US bank assets and $90 billion in deposits. USB agreed to pay $8 billion, with $5.5 billion coming in cash/debt and the remainder in stock. The bank currently has a massive cash stockpile on the balance sheet but could still choose to bring a portion of the cash funding in debt given how cheap it would be for USB to issue debt. Moody’s and S&P both affirmed USB’s A2/A+ ratings, but revised their outlooks to Negative from Stable, mostly reflecting the execution risks of the deal. Fitch affirmed USB’s rating at AA- and left the outlook unchanged at AA-.

Other notable bank acquisitions in 2021 include Citizens Financial Group’s (CFG) agreement to purchase of Investors Bancorp (ISBC) for $3.6 billion announced on 07/28/21. ISBC had no public debt outstanding so it was not a part of our study in late 2020, but the size of $27 billion in total assets was within the parameters of our search. Also announced year-to-date was New York Community Bancorp’s (NYCB) purchase of Flagstar Bancorp (FBC) for $2.6 billion on 04/26/21. Both NYCB and FBC were included in our list of merger candidates last year, and the deal will add $29 billion in assets to NYCB’s $38 billion in total assets as of 2Q21. Several days prior on 04/19/21, Webster Financial (WBS) announced a deal for Sterling Bancorp (STL) for $5.9 billion, which is expected to close by year-end. Again, both banks with current assets of $34 billion and $29 billion, respectively, were listed among our merger candidates in late 2020. Lastly, M&T Bank Corp (MTB) announced a deal with People’s United Financial (PBCT) for roughly $5.3 billion on 02/22/21, in a deal that will add approximately $63 billion in assets to MTB $151 billion as of 2Q21. That deal is also expected to close by year-end 2021.

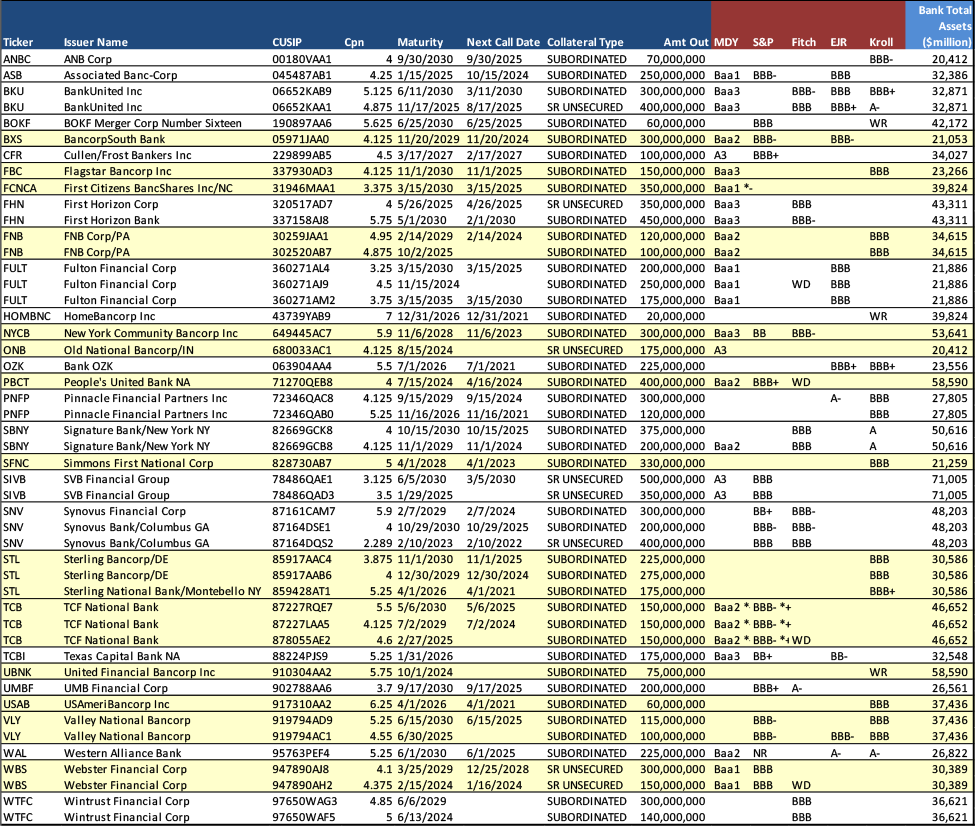

Exhibit 1. Last year’s 2020 Bank Merger Candidates – Highlighted banks have announced mergers as either a buyer or target since the publication of our last study

Source: Amherst Pierpont, Bloomberg LP

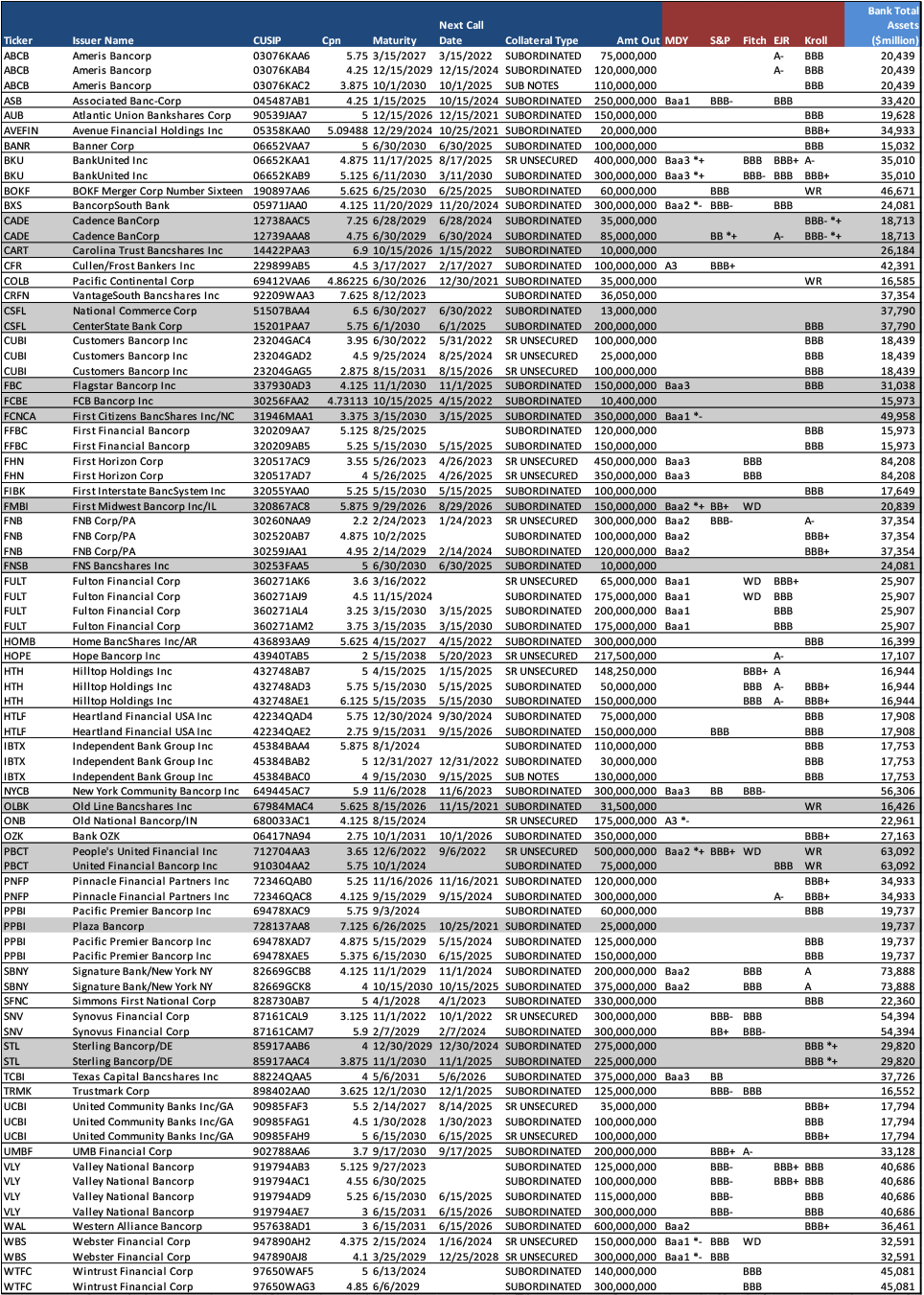

To update our pool of potential merger candidates for investors to target in the corporate bond market we are once again running a screen to identify large community and smaller regional banks. This time we are expanding the search to banks with total assets of between $20 billion to $100 billion from the $75 billion max in last year’s study, given that the BBVA USA and MUFG Union bank deals each had assets of just over $100 billion. We then limit our search to banks with public debt deals with at least $20 million outstanding, which would make them more available to target in the secondary bond market.

Exhibit 2. 2021 Bank Merger Candidates – Shaded banks have already been announced as targets in ongoing/recently closed mergers

Source: Amherst Pierpont, Bloomberg LP