The Long and Short

ICE pilots Black Knight through a turbulent market

Dan Bruzzo, CFA | May 13, 2022

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors.

Although there was no rain, nor snow, nor heat nor gloom of night, Intercontinental Exchange launched a debt deal through turbulent markets in the last week to fund a recently announced acquisition of application software company Black Knight. ICE management clearly sees the current environment as preferable to the unknown of waiting. It is telling that ICE would issue within days after announcing the acquisition and so far from potential completion. Management likely sees the prospect for either higher rates or more market turbulence, or both.

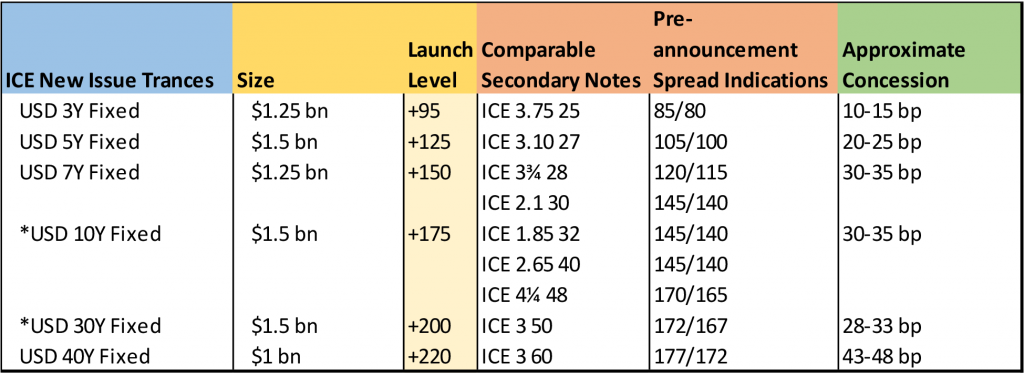

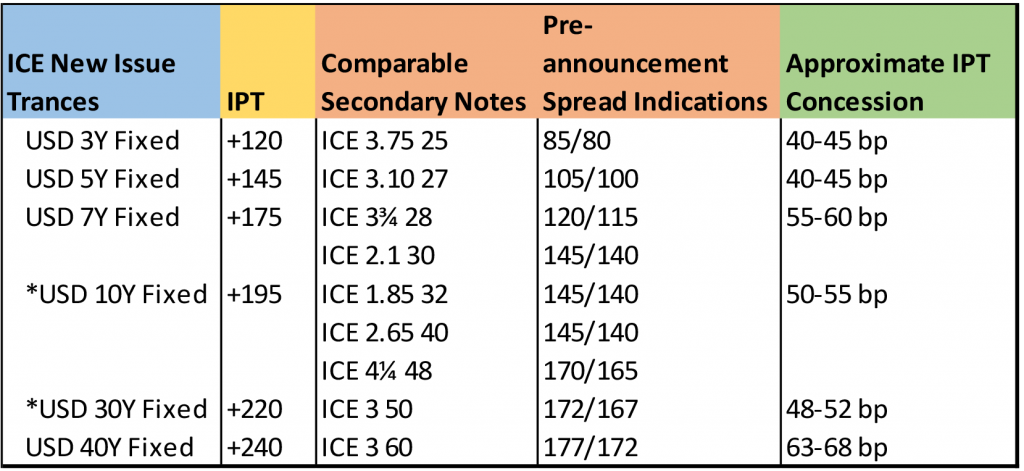

Wasting little time after announcing the $15.6 billion acquisition of Black Knight (BKI: Ba2*+), ICE (ICE: A3/A-) on May 12 announced a 6-part $8 billion debt launch to fund the deal. The targeted completion date on the deal is not until June 30, 2023, which could likely serve as the expiration date on the $101 Special Mandatory Redemption (SMR) language on the debt tranches that include it. The initial price talk on the debt tranches included some extremely generous spread discounts to the existing ICE debt curve just prior to announcement. Though the eventual launch levels came significantly tighter, they still appeared generous and serve as an indicator of just how much the primary calendar can impact secondaries on the days it is actually functional. However, while the concessions on the new debt are substantial, it is important to consider that many of the secondary ICE bonds are trading at deep dollar discounts to par, lending support to their current valuations versus the new deals. The debt launch was roughly 3.5x oversubscribed.

Exhibit 1. New Debt IPT vs Existing ICE Secondary Curve

Source: Amherst Pierpont, Bloomberg TRACE/BVAL, Company Press Release

* Issue does not contain SMR language

ICE agreed to buy Black Knight on May 4, 2022, for $85 per share in a cash and stock transaction (80%/20%) that valued the market cap of BKI at $13.1 billion. Total cash consideration is expected to be $10.5 billion, which at the time of announcement ICE management stated would be paid with newly issued debt and cash on hand. The remaining $2.6 billion will be paid in stock. BKI offers software, data and analytics solutions and will prospectively give ICE a stronger foothold in the mortgage industry. The deal appears to be a solid strategic addition that lies close to ICE’s core competency. Only two years ago, ICE was rumored to be considering a bid for eBay – a deal that would have been well outside the company’s comfort zone and might have suggested that ICE management no longer prioritized its high-quality credit profile and single-A ratings.

According to Moody’s, the additional debt burden of the BKI deal will push ICE’s total debt balance to $24 billion and result in pro forma adjusted debt leverage of approximately 4.4x. ICE has temporarily halted debt repurchases and has indicated that it will not resume until it gets leverage under 3.25x. Moody’s affirmed the A3 rating with a Stable outlook and is affording management two years of flexibility to pay down debt and get to its target leverage into the 2.75-3.00x range.

S&P also affirmed the A- long-term rating and left the outlook at Stable. The rating agency projects that leverage will increase from its current level of 3.0x to 3.4-3.6x, when factoring in projected total synergies of $325 million starting in 2023. Likewise, S&P will be expecting ICE to reach its targeted leverage range of 2.75-3.00x.

Exhibit 2. $8 billion New Debt Launch Levels vs Existing ICE Secondary Curve

Source: Amherst Pierpont, Bloomberg TRACE/BVAL, Company Press Release

* Issue does not contain SMR language

As has become the standard among corporate issuers, most of the new tranches of debt will contain $101 Special Mandatory Redemption language, in the event that the proposed acquisition does not close on time. The 2025, 2027, 2029 and 2062 notes will all contain the SMR feature. Meanwhile, the 2033 and 2052 notes will not contain SMR language and would therefore not be redeemed in the event that the BKI deal does not close. The use of proceeds on the non-SMR bonds is the redemption of upcoming debt maturities, including the $500mm notes due in September of 2022, the $400 million notes due in September of 2023, the $1 billion notes due in June 2023 and the $800 million notes due in October of 2023. Which again speaks to management’s likely concerns regarding higher rates and/or additional market trepidation on the near-term horizon.

Bonds with $101 SMR language have recently come into focus with the extreme move in interest rates year-to-date, which has many of those issues trading at deep discounts to their prospective redemption prices. This was highlighted recently when Rogers Communications’ (RCICN: Baa1*-/BBB+*-/BBB+*+) proposed $20 billion acquisition of Shaw Communications was challenged by regulators, putting the deal in jeopardy. Though RCI management is seeking to appease regulators with potential asset sales, the deal remains in question, thus putting upward pressure on the dollar price of the SMR bonds that were issued to fund the deal. Management has until year-end 2022 to consummate the deal or risk triggering the SMR feature.