By the Numbers

A tactical short in the basis

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors.

This note was originally distributed on August 3, 2022.

Nominal and option-adjusted spreads on MBS have tightened significantly through June and July, raising the possibility of picking up total return by tactically shorting MBS against Treasury debt. The best spot for doing that looks like FNCL 2.0%s where an estimated only 7 bp of spread widening put the trade in the money.

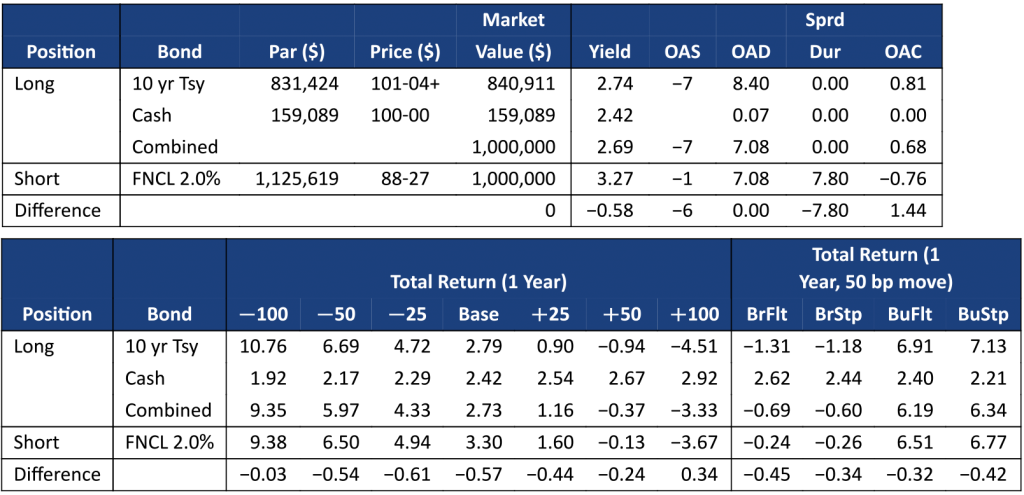

A portfolio can match market value and duration in FNCL 2%s with a combination of 10-year Treasury debt and cash (Exhibit 1). The MBS position has a natural yield advantage to compensate for negative convexity. The MBS carry advantage shows up in most of the total return scenarios where getting long Treasury debt against MBS underperforms. The MBS advantage diminishes over larger rate moves as the convexity of the Treasury position kicks in. The Treasury position importantly avoids the 7.80 spread duration of the MBS.

Exhibit 1. Replacing FNCL 2%s with the 10-year Treasury bond

Note: All market levels as of 8/2/2022 close. Returns assume a linear shift over the holding period, reinvestment in 1-month T-bills and repricing at constant OAS.

Source: Yield Book, Amherst Pierpont Securities

Spreads only must widen 7.3 bp to break-even in the base case 1-year total return. The break-even spread widening is estimated by dividing the MBS’s performance advantage by the spread duration [7.3 bp=100.0*(0.57/7.80)]. It would take 7.8 bp widening to break even in the lowest scenario, a 25 bp rally.

The nominal mortgage basis—the spread of the par coupon to the interpolated 7.5-year Treasury curve—is currently 128 bp but was roughly 140 bp to 145 bp for much of June and July. It peaked at 151 bp on July 14. The basis widened 14 bp yesterday, undoing a lot of the tightening that followed the FOMC meeting last week, so mortgage spreads are volatile. It is plausible that the basis could widen another 12 bp or more to get back to the typical level in June and July.

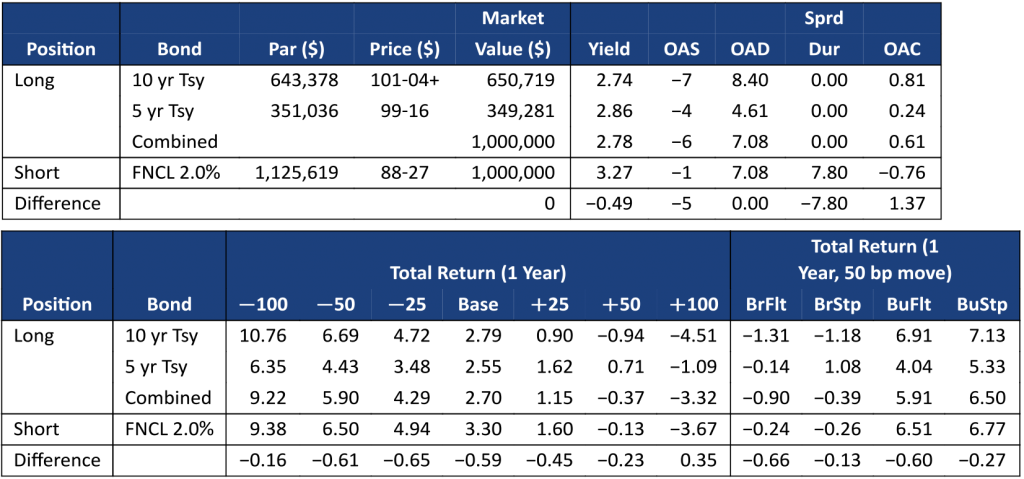

An investor with a curve view could replace the MBS with a combination of 5-year and 10-year treasuries instead of cash and 10-year treasuries (Exhibit 2). The 10-year+5-year combination is better than the 10-year+cash combination when the curve steepens but worse when it flattens. Otherwise, the yield, convexity, and parallel-shift total returns are comparable to the 10-year+cash combination.

Exhibit 2. Replacing FNCL 2%s with 5-year and 10-year Treasury bonds

Note: All market levels as of 8/2/2022 close. Returns assume a linear shift over the holding period, reinvestment in 1-month T-bills and repricing at constant OAS.

Source: Yield Book, Amherst Pierpont Securities

This trade can also be done in higher coupons, but more spread widening is needed to break even on the trade. The total returns are lower because higher coupon MBS carry better than lower coupon MBS, and spread durations are shorter. For example, the 1-year total return in the base case drops 0.91% when replacing FNCL 3%s with Treasuries, and the spread duration falls to 7.02. That trade needs 13 bp of widening to break even.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2024 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.